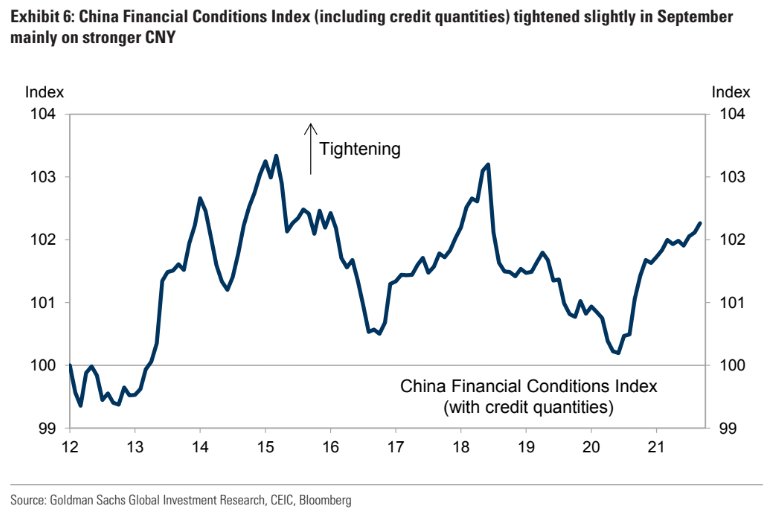

Good and bad news today for the Chinese property crash today. It has been a few better days for developer spreads and equity as the PBoC gets busy with its jawbone. Wider financial conditions remain tight:

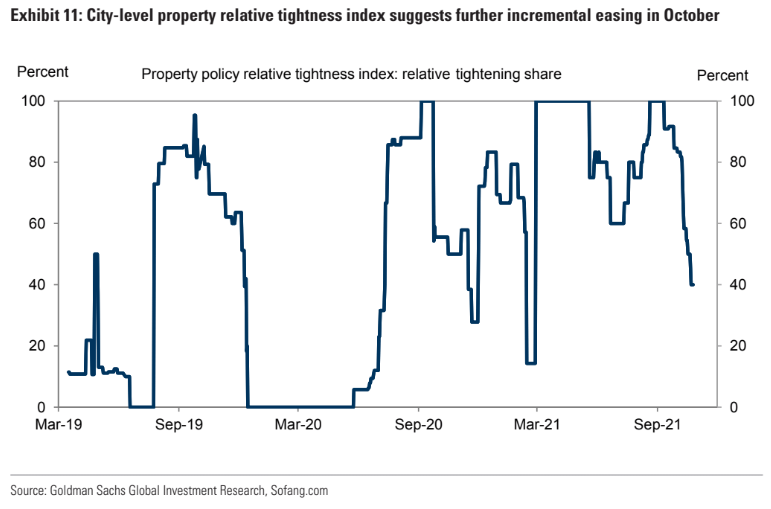

But the demand side of property is seeing easing:

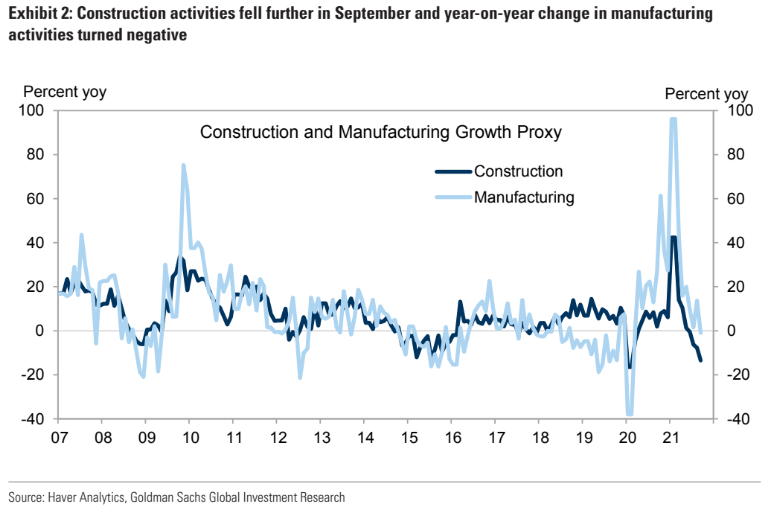

As the construction market outright crashes:

Advertisement