By Gareth Aird, head of Australian economics at CBA

Key Points:

- We expect the headline CPI to increase by 0.8% in Q3 21 (+3.0/yr).

- The trimmed mean CPI on our forecasts will print at +0.5% (1.8%/yr).

- The lift in consumer inflation in Australia will lag a number of other advanced economies, but we believe it’s coming and forecast underlying inflation to accelerate to 2½% by mid-2023.

- We expect the RBA to commence normalising the cash rate in May 2023; markets should be reminded that the RBA will be deliberately late to start its tightening cycle.

Overview:

The upcoming Q3 21 CPI is a big one for domestic financial market participants. A lift in actual inflation and inflation expectations in a number of advanced economies has markets on edge. But those looking for an upside inflation surprise on Wednesday 27 October, like we have seen in other jurisdictions, are

likely to be disappointed.

Regular readers will know that we have been making the case all year that higher inflation was in the pipeline. Indeed our expectation for inflation to lift has been founded on the idea that “this time is different”. Our views appeared quite hawkish earlier this

year. But the recent inflation data overseas has supported our narrative.

That said, a meaningful lift in core inflation is yet to appear in the official data in Australia. That is in large part because a number of government subsidies and rebates have put downward pressure on measured consumer inflation over the pandemic. And wages pressures have also been slow to emerge which has

kept a lid on services inflation.

That will change as we move through 2022. But we are not at that point just yet. In addition the emergence of the delta variant locally pushed our timetable back a little for higher wages and inflation.

What happened in Q3 21

The pandemic hit the Australian economy hard over Q3 21 and that will have implications for inflation over the period. Sydney and Melbourne were essentially in lockdown for the entire quarter and that will weigh on some parts of the CPI basket. Notwithstanding, we think the Q3 21 CPI will show a modest

acceleration in underlying inflation on a six month annualised basis. It will set the scene for a firmer inflationary pulse next year.

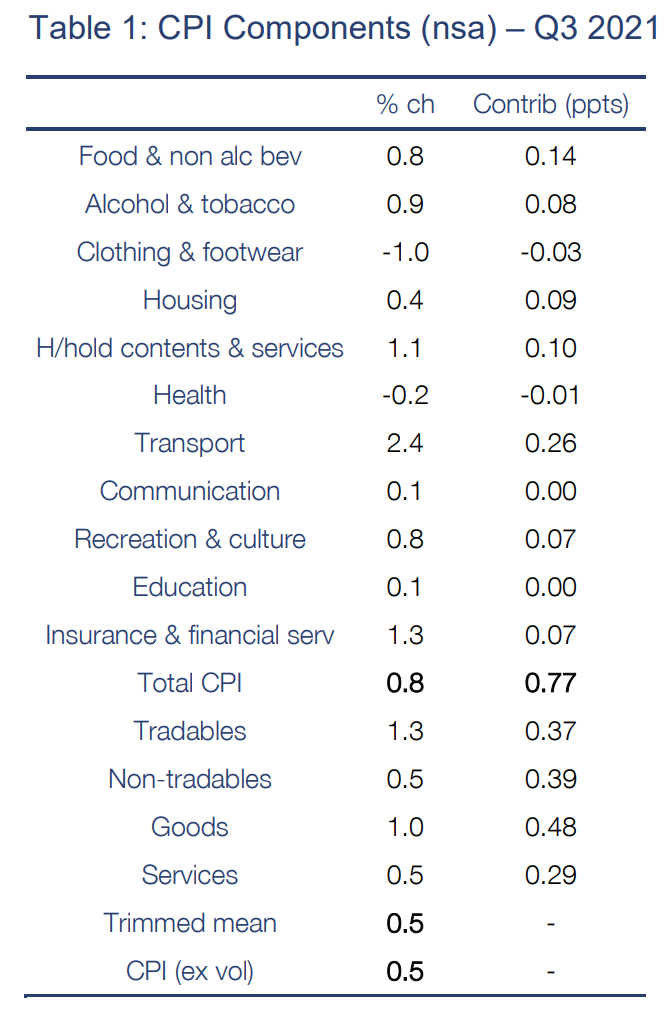

Our forecast is for the headline CPI to increase by 0.8% in Q3 21 which would see the annual rate dip to 3.0% (recall that the Q2 21 headline CPI leapt to 3.8%/yr on a base effect). Tradables inflation is forecast to be stronger than non-tradables, while goods inflation should outpace services inflation.

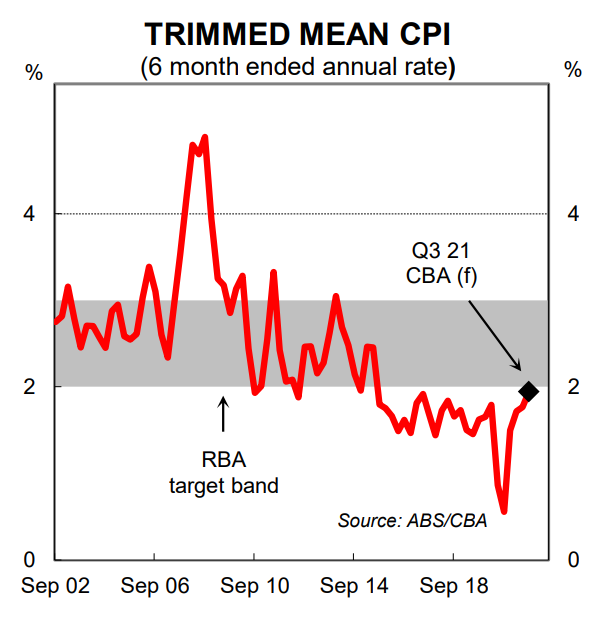

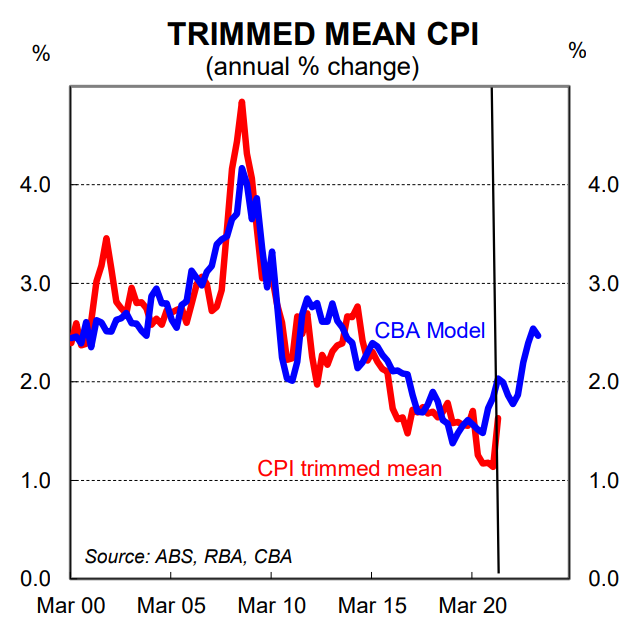

On our figuring the trimmed mean will rise by 0.5% which will push the annual rate up a little to 1.8%. The six month annualised rate, which better captures the inflationary pulse, is forecast to step up to 1.9%. The risk lies with a stronger print, particularly in light of the Q3 21 NZ CPI (see below).

The detail

The main features of our call are as follows:

- a decent rise in food prices of 0.8% following a more modest 0.5% lift in Q2 21;

- a solid 2.4% increase in transport primarily driven by a 5.5% increase in petrol prices;

- a 1.1% increase in household furnishings, equipment and services;

- seasonally low increases in health and education prices; and

- a modest 0.4% rise in the housing component despite strong upstream price pressures in the home construction space (see below).

Table 1 below contains our detailed forecasts for the Q3 21 CPI basket.

A closer look at housing

The housing component of the CPI is worth just under a quarter of the basket (it was slightly upwardly reweighted in the annual re-weight). It essentially comprises three components: (i) the cost of building or renovating a home; (ii) rent; and (iii) utilities and other charges.

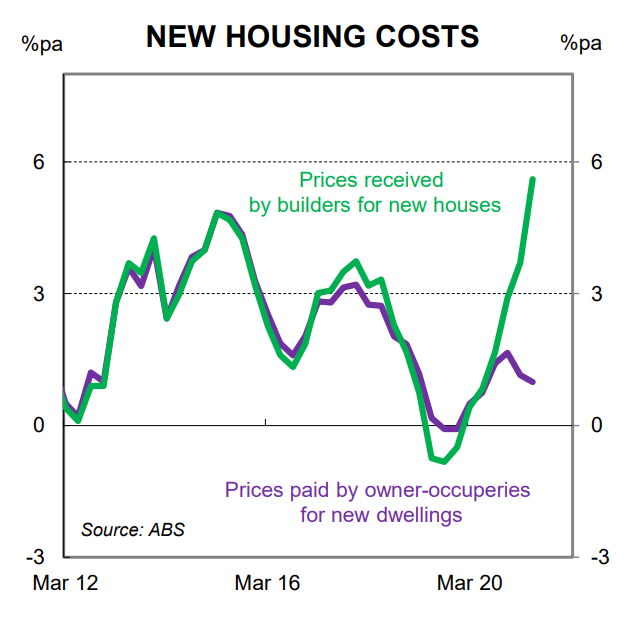

The Government’s HomeBuilder package has been an incredible success and residential investment has surged. This has been accompanied by an increase in prices charged due to both a spike in the demand for labour, which allows builders to charge more, and also a lift in the cost of materials. But that lift in

output prices has not been reflected in the CPI given the price rises are discounted by the grants (see facing chart). The measured price of building a home is likely to stay artificially supressed in Q3 21 as the grant continues to influence outcomes. But that will change next year.

On rents, our internal data indicates that average rent paid has lifted quite significantly. And the CoreLogic data, which captures advertised rent rather than rent paid, is sending a similar signal. We forecast that rents rose by 0.7% in Q3 21 with the risk skewed towards a stronger outcome. And finally we expect little change in utilities prices over the September quarter.

A reminder – it’s an 8 capital city inflation gauge

The CPI measures quarterly changes in the price of a ‘basket’ of goods and services for metropolitan households. It is based on capital city indexes which measure price changes across each capital city in Australia individually. It does not include price changes in regional Australia. In ‘normal’ times this does not

matter much. But it stands to reason that price rises in regional Australia have been stronger than in the capital cities at an aggregate level due to the relative strength of spending, employment and housing. In other words, the CPI is currently likely to be understating actual inflation across Australia.

Risks

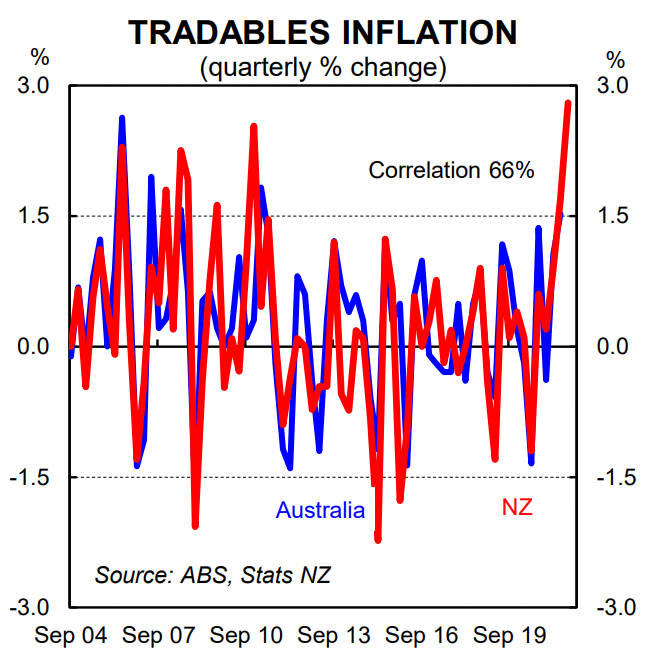

The international experience indicates the risk to our call sits with an upside surprise. The NZ Q3 CPI was very strong and printed a lot higher than the consensus (+2.2%/qtr vs +1.5% consensus). Tradables inflation rose by a large 2.8% in the NZ Q3 CPI while we have it pegged at 1.3% in Q3 21 (there is a decent correlation between tradables inflation in Australia and NZ ).

That said, the market may be disappointed even with an upside surprise against our numbers given the significant sell off in rates over the past few weeks (see here from our rates strategists).

Inflation and the RBA

The RBA has forecast the trimmed mean to be 1¾% at Q4 21 which implies quarterly growth rates of 0.4-0.5% over the September and December quarters.

As such, if the trimmed mean CPI prints in line with our call it would be broadly in line with the RBA’s forecast. Such an outcome would likely mean that the RBA will not make any material revisions to their forecast profile for underlying inflation in the November Statement on Monetary Policy. This means they will retain their current forward guidance.

Here we stress that the RBA will stick with the 2024 mantra until actual outcomes on inflation and wages mean they must make significant upward revision to their forecast profile which are inconsistent with their current forward guidance. We do not expect that to happen this year.

The hurdle for RBA rate hikes remain high.

As Governor Lowe said in mid-September, “the Board has said that it will not increase the cash rate until actual inflation is sustainably within the 2–3 per cent target range. It won’t be enough for inflation to just sneak across the 2 per cent line for a quarter or two. We want to see inflation around the middle of the target range and have reasonable confidence that inflation will not fall below the 2–3 per cent band again. Our judgement is that this condition for a lift in the cash rate will not be met before 2024.”

We believe that condition will be met in the first half of 2023 and our central scenario sees the RBA commence normalising the cash rate in May 2023.

Global inflation outcomes suggest the risks are firmly tilted towards an earlier lift off in the cash rate. But the lack of any meaningful lift in wages growth to date coupled with the risk that labour supply increases sharply when the international border reopens means we think the risks to our call are more evenly balanced.