By Gareth Aird, head of Australian economics at CBA:

Key Points:

- Remarkably high vaccination rates and an earlier reopening of NSW and Victoria means we upgrade our forecast profile for the Australian economy.

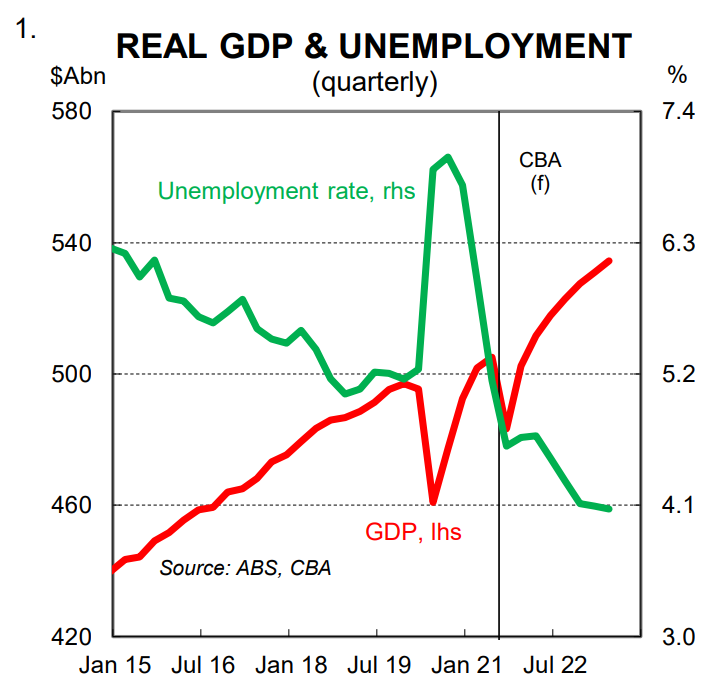

- We make an upward revision to our GDP forecast to look for growth of 2.0%/yr at Q4 21 and 5.0%/yr at Q4 22.

- GDP growth is forecast to be 3.5% in 2021 (from 3.0% previously) and 4.4% in 2022 (from 4.0% previously).

- We forecast the unemployment rate to be 4.7% at end‑2021 (from 5.2% previously) and 4.0% at end‑2022 (from 4.7% previously).

- We have upwardly revised our profile for underlying inflation to be 2.5%/yr at mid‑2022 (from 2.1% previously). That is, underlying inflation will be around the middle of the RBA’s 2‑3% target range by the middle of next year.

- We expect the RBA to taper its bond buying to $A2bn per week in February 2022 until mid‑May. We expect that to be the final tranche of quantitative easing (QE).

- We think the RBA will exit yield curve control (YCC) in Q2 22 and favour the May Board meeting for that decision to be announced (the risk is that the RBA exit earlier and the November Board meeting next week is ‘live’ regarding a decision on the yield curve target).

- We now expect the RBA to commence normalising the cash rate in November 2022 (from May 2023 previously).

Overview

There have been three key developments that mean we upgrade our central scenario for the Australian economy:

(i) the take‑up of the COVID‑19 vaccine has been exceptional;

(ii) the labour market has held up better than we feared during the lockdowns in NSW and Victoria; and

(iii) both NSW and Victoria reopened ahead of our timeline (note this is of course linked to the take‑up and speed of the vaccine rollout).

We would also add that both business and consumer confidence sit at above average levels. And the international border is now set to reopen earlier than anticipated.

In summary, there has been a host of positive developments recently that mean the economic outlook is brighter.

There is of course still a great deal of uncertainty about the future as we transition from a COVID‑19 pandemic to a world where the virus is endemic. But it is our assessment that we are in for a less choppy ride than we previously expected because the take‑up of the vaccine has been world leading.

In this note we discuss our updated central scenario for the Australian economy and our RBA monetary policy call.

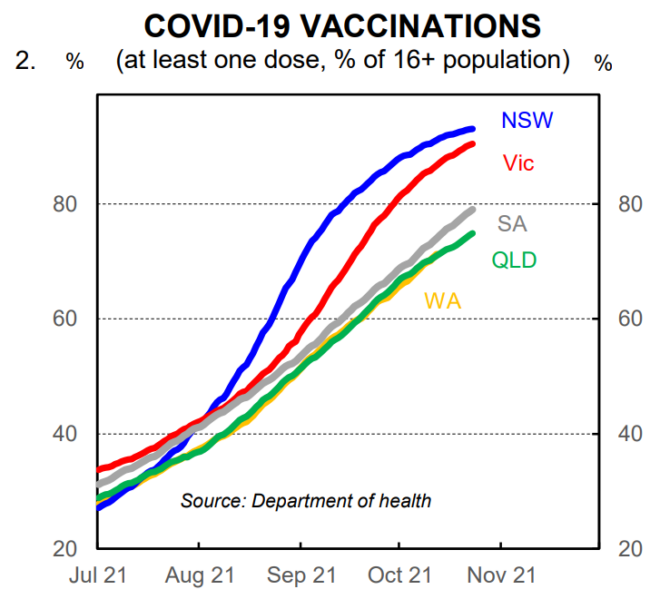

Adult vaccination rate of 95% is likely across the country

Health and economic outcomes have been inexorably linked over the pandemic. The best performing economies around the world and indeed within Australia have generally had the lowest levels of serious COVID-related illness.

Vaccination rates will be a key driver of health outcomes from here and that in turn will influence economic outcomes. On that score, Australia is now very well placed. Vaccination hesitancy dropped sharply over the past six months and inoculation rates have exceeded our expectations. The ‘carrot and stick’ type

approach used by policymakers and business leaders to get people vaccinated quickly and in large numbers has achieved the desired outcome.

As we go to press the 16 years+ vaccination rate in NSW sits at 93% (chart 2). It looks likely now that vaccination rates of around 95% across the country will be attained. This will make Australia one of the most vaccinated countries in the world. And crucially it will mean ‘living with COVID’ will be a lot less disruptive from here which means better economic outcomes.

Spending to rebound sharply in Q4 21 and then rise strongly in 2022

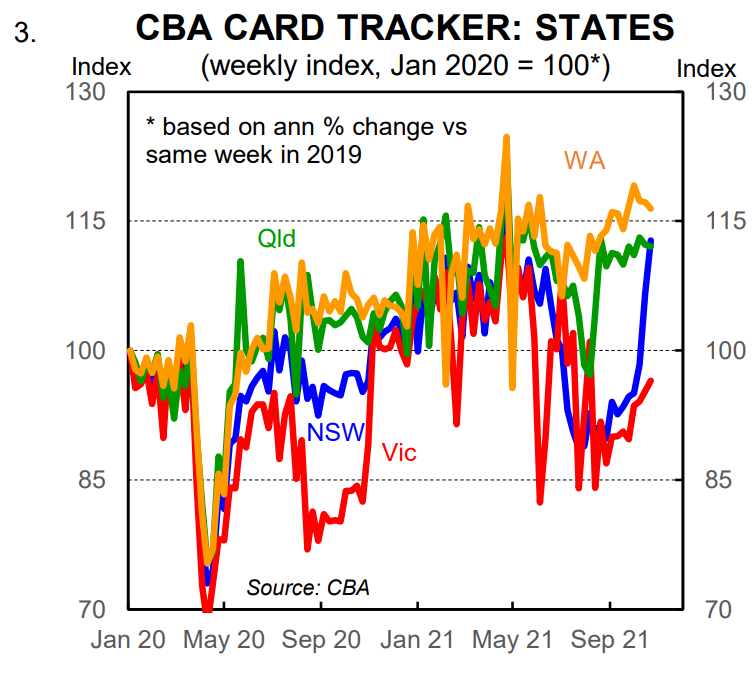

The reopenings of NSW and Victoria have occurred earlier than we had pencilled in. Our working assumption was that NSW would not reopen until early November. The reopening of Victoria was expected to follow shortly after. But the pace of the vaccine rollout was better than we anticipated.

Our internal data indicates that spending has jumped sharply in NSW on the reopening of Australia’s largest state. Spending on CBA credit and debit cards is tracking around 15% higher since the lockdown ended in NSW and is already back to its pre-delta high (chart 3). A similar outcome is anticipated in Victoria

over coming weeks, notwithstanding the more conservative approach taken to winding back restrictions.

Key interstate borders will reopen soon and the free movement again of people across large parts of the country will boost travel expenditure and the domestic tourism sector. More generally, pent up demand is about to be unleashed and discretionary services spending is on the cusp of a boom as we close out the

year.

We now expect real household expenditure to rebound by 5.9% in Q4 21 following a forecast contraction of 6.8% in Q3 21. Looking further ahead, we anticipate very strong growth in household expenditure over 2022.

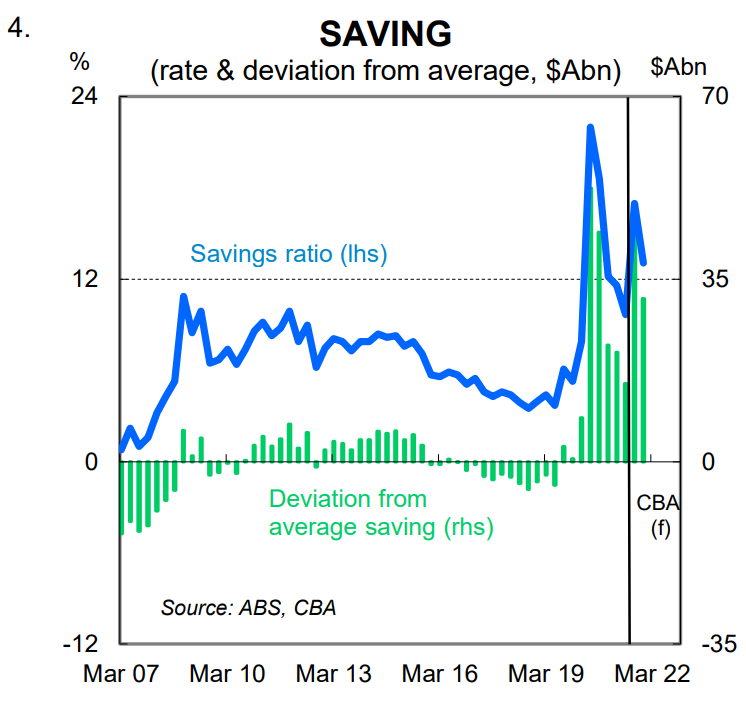

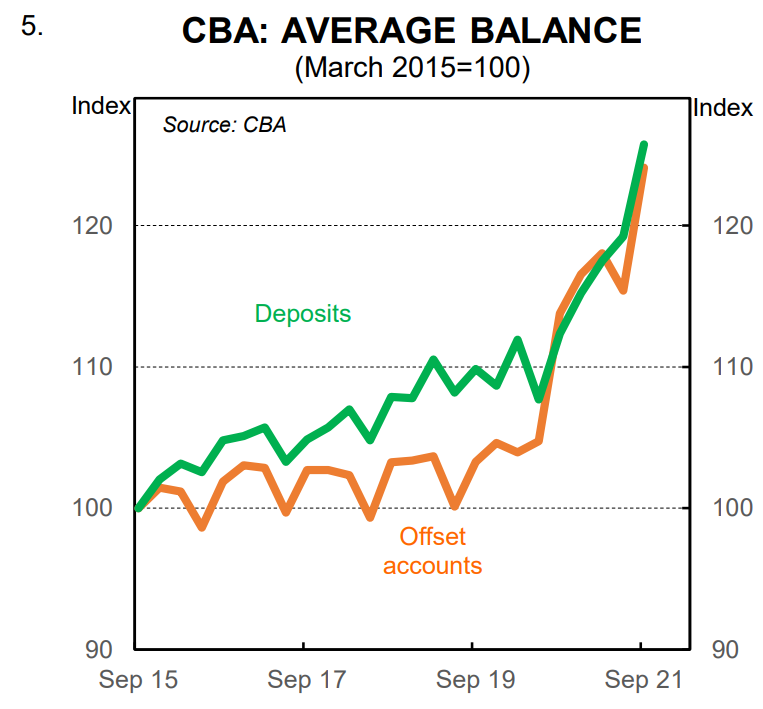

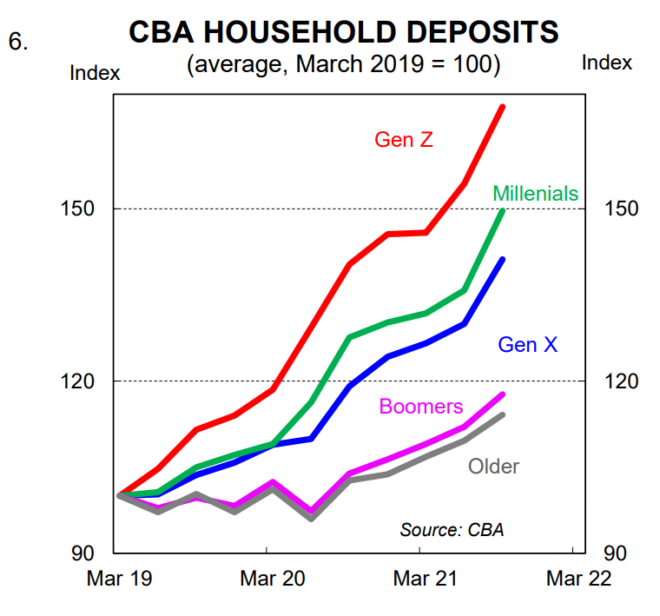

By the end of 2021 we forecast additional savings will have ballooned by $A230bn over the pandemic (11.5% of GDP – chart 4). We covered the savings story in detail recently, particularly in terms of the mechanics between savings, debt repayment and deposit growth.

The upshot is that we are more confident that a decent chunk of the increase in household deposits will be deployed to support spending given very high vaccination rates will deliver better health outcomes. In addition, a further dive into our internal data reveals that the most rapid growth in deposits has been

across the younger age cohorts (charts 5 and 6). We believe that younger people are more likely to deploy extra savings on discretionary services-related expenditure; a case of making up for lost time in lockdown over the pandemic.

It is our expectation that the extraordinarily high level of savings plus the surge in wealth driven largely by rapid growth in home prices will result in very strong real household consumption growth of ~7%/yr in 2022.

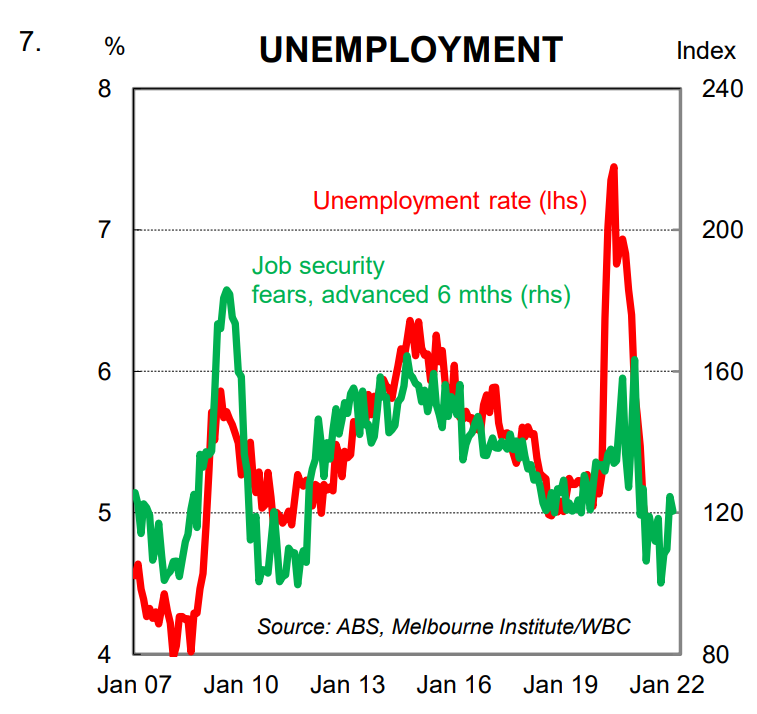

The labour market will heal very quickly The labour market has held up better than we feared through the long lockdowns in NSW and Victoria. To be clear, the drop in employment was still extraordinarily large. But headcount contracted by less than we anticipated in the absence of JobKeeper. The national unemployment rate retained a 4-handle throughout the lockdown periods due to the fall in participation.

It is our assessment that measured unemployment did not rise during the lockdowns as the vast majority of people stood down knew that they were returning to work as soon as the lockdown was over. Consumer expectations around the future level of unemployment support this view.

Job security fears, as measured by the unemployment expectations index in the WBC/Melbourne Institute consumer confidence survey, stayed low over the lockdowns, consistent with future low unemployment (chart 7).

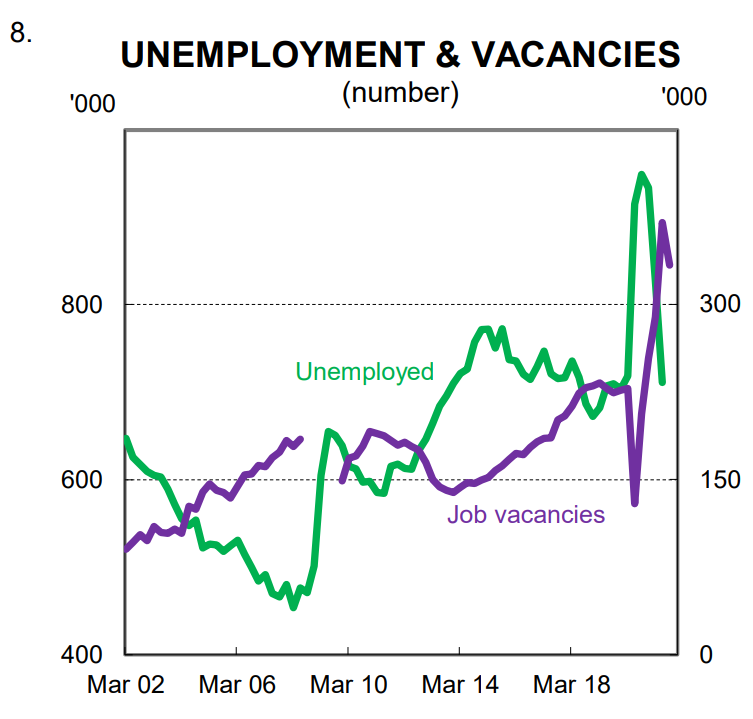

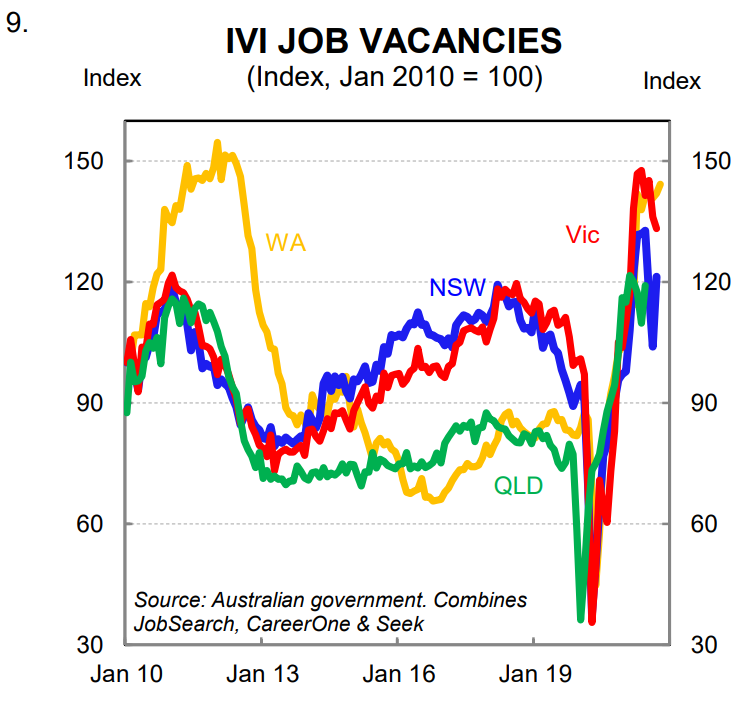

The forward looking indicators of labour demand look very healthy (chart 8). We monitor a range of job vacancies series: ABS job vacancies, ANZ job advertisements and the Australian Government’s Internet Vacancy Index (IVI) are three personal favourites. All of these series are sending the same signal –

namely, that there are a lot of job vacancies at present and they are broadbased across a range of regions and industries.

One feature of the data that is particularly encouraging pertains to the elevated level of job vacancies in NSW and Victoria – that states that were in lockdown (chart 9).

We forecast the unemployment rate to end-2021 at 4.7%. Strong employment growth over 2022 will see the unemployment rate on our figuring drop to ~4.0% by end-2022.

Inflation and wages in 2022

Regular readers will know that we have been making the case all year that higher inflation was in the pipeline (see here and here). Indeed our expectation for inflation to lift has been founded on the idea that “this time is different”. Our views appeared quite hawkish earlier this year. But the recent inflation data

overseas has supported our narrative as has the Australian Q3 21 CPI.

That said, a meaningful lift in core inflation has taken some time to appear in the official data in Australia. Indeed the Q3 21 CPI has been the only ‘strong’ print. That is in large part because a number of government subsidies and rebates have put downward pressure on measured consumer inflation over the

pandemic. And wages pressures have also been slow to emerge – which has kept a lid on services inflation.

That will change from here and we believe the Q3 21 CPI is the inflection point. The fiscal splurge, financed by money printing, is the circuit breaker the RBA has required to achieve higher inflation. The oddity would be if we did not see a continued lift in inflation next year.

We expect underlying inflation to be 2.5%/yr by mid-2022 – that is, around the middle of the RBA’s 2-3% target range.

There will be evidence of both demand pull and cost push inflation in the CPI as we go through next year. Ongoing supply side distributions will put upward pressure on input pressures. Indeed the business surveys indicate upstream inflation pressures are very significant. In addition a surge in aggregate demand

as households deploy savings will mean some businesses will lift the prices of the goods and services they are selling.

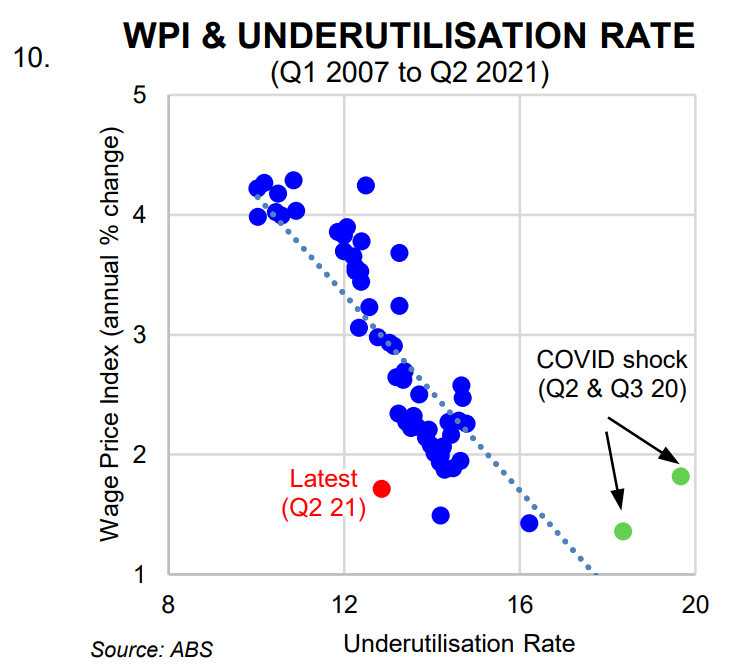

Wages growth is forecast to gradually rise as we move through 2022. The labour market will tighten and that will see more workers gain an increase in pay. To be clear, there will be a lag between falling underutilisation and wage rises. But we expect the historically strong relationship between wages growth and underutilisation to assert itself over 2022 (chart 10).

We also expect a lift in consumer inflation to help push wages growth higher. There is something of a chicken and egg relationship between wages growth and inflation. Stronger wage outcomes often lead businesses to raise consumer prices to cover the increase in the cost of production. But it is also true that higher actual inflation outcomes raise inflation expectations and that in turn boosts wages.

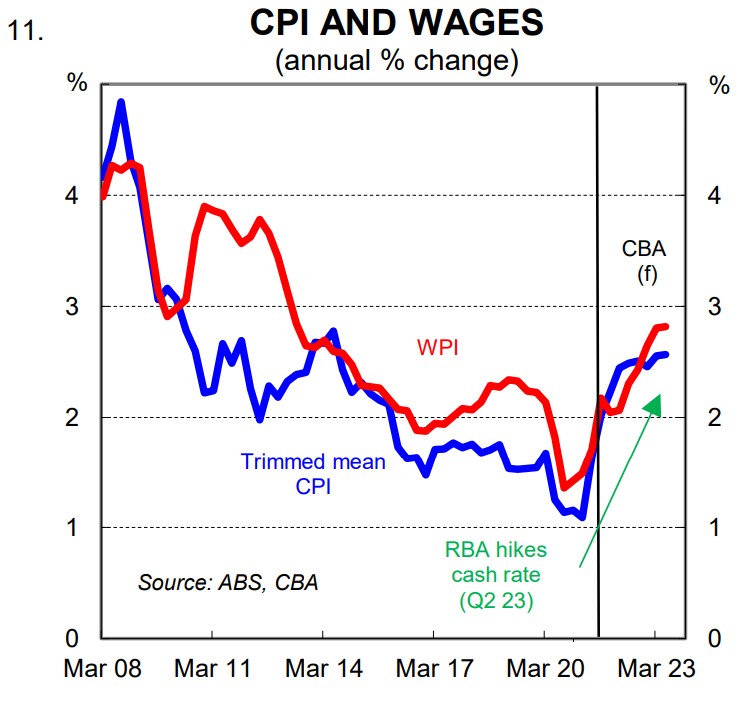

A lot of wage agreements are negotiated from a starting point of recent actual inflation outcomes. So our expectation for an acceleration in inflation over 2022 will help to push wages higher (chart 11). Indeed we expect underlying inflation to be higher than wages growth through most of 2022. Put simply there will be a positive feedback loop between higher inflation and higher wages which is exactly what the RBA is trying to achieve.

Our RBA call

There are essentially three parts to our call RBA monetary policy call: (i) the bond buying program; (ii) yield curve control; and (iii) the cash rate.

(i) Bond buying program

When thinking about the outlook for the RBA’s bond buying program (BPP), otherwise known as QE, it is helpful to review a timeline of their announcements and decisions.

At the July 2021 Board meeting the RBA announced that it would extend bond purchases from early September until midNovember at a reduced rate of $A4bn per week (it had been buying at a rate of $A5bn per week). The decision constituted a

taper.

At the July Board meeting the RBA stated it would conduct a further review in November on the BPP, allowing the Board to respond to the state of the economy at that time. Our RBA call at the time on the BPP was that they would announce a further tapering in November. More specifically, we expected them to commit to buying $A3bn of bonds per week from mid-November to mid-February 2022, with a three week pause over the Christmas/New Year holiday period. We then expected the RBA to announce at the February 2022 Board meeting that they would commit to bond buying from mid-February to mid-May 2022 at a further reduced based of $A2bn per week. We expected the cessation of bond purchases in May 2022. The tapering profile therefore that we thought the RBA would deliver was $A4bn, $A3bn, $A2bn – per week for three months each.

However the delta outbreak and associated restrictions on activity through lockdowns in NSW and Victoria meant that at the September Board meeting the RBA announced that it would continue buying bonds at a rate of $A4bn per week through to mid-February 2022.

We think that provided the economy bounces back quickly the extension of $A4bn per week through to mid-February 2022 simply replaces the originally intended $A3bn per week three month tranche of bond buying. That is, the commitment to buy bonds through to mid-February at a rate of $A4bn per week does not extend the overall program. As such, we expect the RBA to announce at the February 2022 Board meeting that they will commit to bond buying from mid-February to mid-May 2022 at $A2bn per week. In other words the RBA will be back on the implied original timeline, albeit they will have purchased an

additional ~$A10bn of bonds.

It is our expectation that by May 2022 the economy will be expanding at a sufficient pace and inflation pressures will have emerged such that the RBA will cease QE.

(ii) Yield curve control (YCC)

Regular readers will know that as far back as November 2020 we remarked that, “we think that the economy will be on a sufficiently entrenched path of improvement by the middle of next year (2021) that the RBA will need to either remove or increase the target yield on the 3 year Australian Commonwealth Government Bond (ACGB)”.

Our views on the economy and the RBA were very much non-consensus at the time. But financial markets started to support our call on YCC in mid-February when a kink developed in the three year part of the yield curve. The RBA was forced to defend its yield curve target (YCT) by buying large quantities of the April 24 bond, while the yield on the November 24 bond climbed from 0.2% to 0.43% in just over a week. As recently as last week the RBA was once again forced to defend its YCT.

In the end the RBA chose neither to remove YCC nor increase the target yield on the 3yr ACGB as we proposed. Instead they decided to keep the YCT of 0.1% pegged to the April 24 bond at the July Board meeting. We still believe that abandoning YCC would have been the most appropriate policy decision given the outlook for the Australian economy and the need for policy flexibility down the line. But the RBA took that option off the table in March 2021 when they said they would only consider whether to maintain the April 24 bond as the target bond or shift the focus of the yield target to the November 24 bond.

The RBA’s conditional 2024 forward guidance on the cash rate is linked directly to the YCT. The RBA can and will persist with the 2024 mantra and the YCT whilst they can credibly make the case that the condition to raise the cash rate, actual inflation sustainably within the target, will not be met until 2024. But once the data means they can no longer make that case we think they will be forced to abandon YCC.

It is our working assumption that the RBA abandons YCC at the May 2022 Board meeting. Our expectation is that the Q1 22 CPI, which prints just before the May Board meeting, will show that underlying inflation is close to the middle of the RBA’s 2-3% target (our forecast profile has Q1 22 underlying CPI at 2.4%/yr). This will render it no longer credible to continue with the 2024 mantra and we expect the YCT to be abandoned along with the 2024 conditional forward based guidance on the cash rate.

It is possible that the RBA exit YCC earlier. That exit could come as early as the November Board meeting next week. While we think it unlikely that the RBA will abandon it so soon, it’s a risk and the November Board meeting should be considered “live” with regards to YCC.

(iii) Cash rate

The hurdle to walk away from YCC and the 2024 conditional forward based guidance on the cash rate is a lot lower than the hurdle to raise the cash rate. It is one thing for the RBA to shift gear and drop YCC and abandon current forward guidance if they are no longer sure that they think the cash rate will be on hold until 2024. It is another thing to increase the cash rate.

Our call prior to the delta outbreak was that the RBA would commence normalising the cash rate in November 2022. We pushed that out to May 2023 in late July because we thought that ‘living with COVID’ would set the economy back around six months compared to its pre-delta path. However, given vaccination rates have significantly exceeded our expectations we think the economy will be back on its pre-delta path a lot sooner. Indeed the increase in savings over the lockdowns means even stronger outcomes in 2022 are forecast compared to pre-delta. This means we pull our rate hike call forward, but not too far

forward.

In his speech of 6 July the Governor said, “the Board does not intend to increase the cash rate until inflation is sustainably within the 2-3% range. It is not enough for inflation to be forecast in this range. We want to see results before we change interest rates.” That statement was a little vague, but we took it to mean that core inflation around 2¼% and on a rising trend would be sufficient to raise the cash rate providing wages growth was also moving higher.

However, in his speech of 14 September the Governor stated, “it won’t be enough for inflation to just sneak across the 2-3% line for a quarter or two. We want to see inflation around the middle of the target range and have reasonable confidence that inflation will not fall below the 2–3% band again”.

The RBA Governor has effectively raised the hurdle for a rate hike in recent months.

The RBA’s explicit shift to see actual inflation around the middle of the target band before raising the cash rate is indicative of their desire to make sure the below target outcomes in the years prior to the pandemic are not repeated. The RBA wants to reset inflation and wage expectations higher so they will be deliberately late to hike the cash rate.

We return to our pre-delta call for the RBA to commence raising the cash rate in Q4 2022. We have pencilled in a first increase of 15bp in November 2022, which would take the cash rate to 0.25%. We expect that to be followed by an increase of 25bp in December 2022. We have three further 25bp hikes in Q1 23, Q2 23 and Q3 24 that take the cash rate to 1.25% (our estimate of neutral). Overall we expect it to be a shallow and gradual tightening cycle given the elevated level of household indebtedness.

Foreign labour remains a key risk to our RBA call on the cash rate

Earlier in the year we noted that the recipe for generating higher nominal wages growth and inflation is quite simple – have fiscal and monetary policy working in tandem to stimulate economic activity and job creation, whilst growth in the labour market is somewhat contained.

This does not mean that the international borders need to remain closed or that firms cannot hire from a global pool of labour. But it does mean that the targeted level of immigration in the economy will need to be recalibrated when the international borders are reopened if wages growth is to make a more permanent lift to around 3% per annum.

There is a great deal of uncertainty with regards to the speed at which foreign workers will return when the international border is reopened. If growth in labour market supply is too strong it will make it a lot harder to get a meaningful lift in wages growth and by extension it will make it harder for the RBA to raise the cash rate.

Ultimately the outcomes we get will reflect the priorities of policymakers. If full employment and a meaningful and sustainable lift in nominal wages growth is the combined priority of both the RBA and the Commonwealth Government then we believe it will be achieved by late 2022 and sustained through 2023 as monetary policy is normalised.