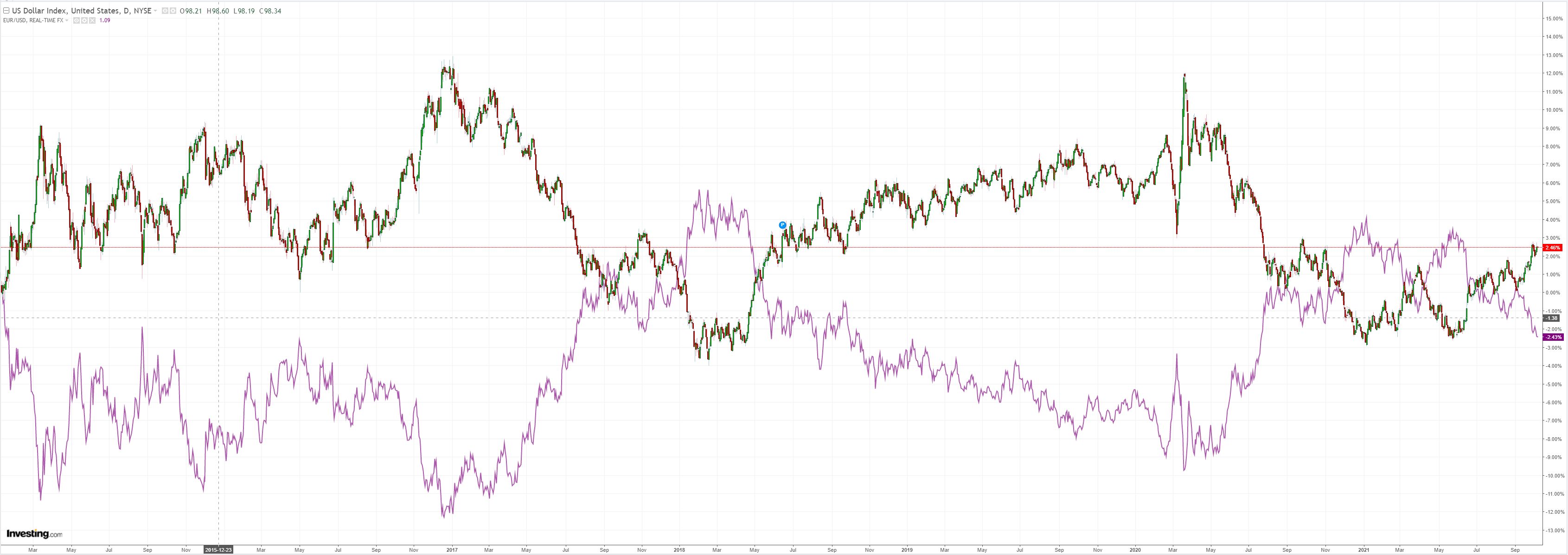

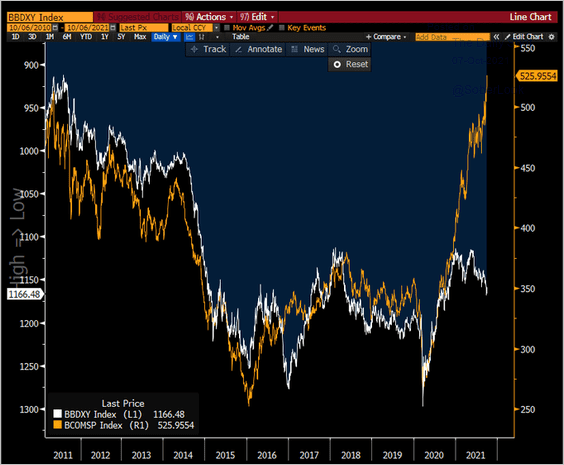

DXY was roughly flat last night EUR up:

Australian dollar is an energy rocket:

Oil held on, gold fell:

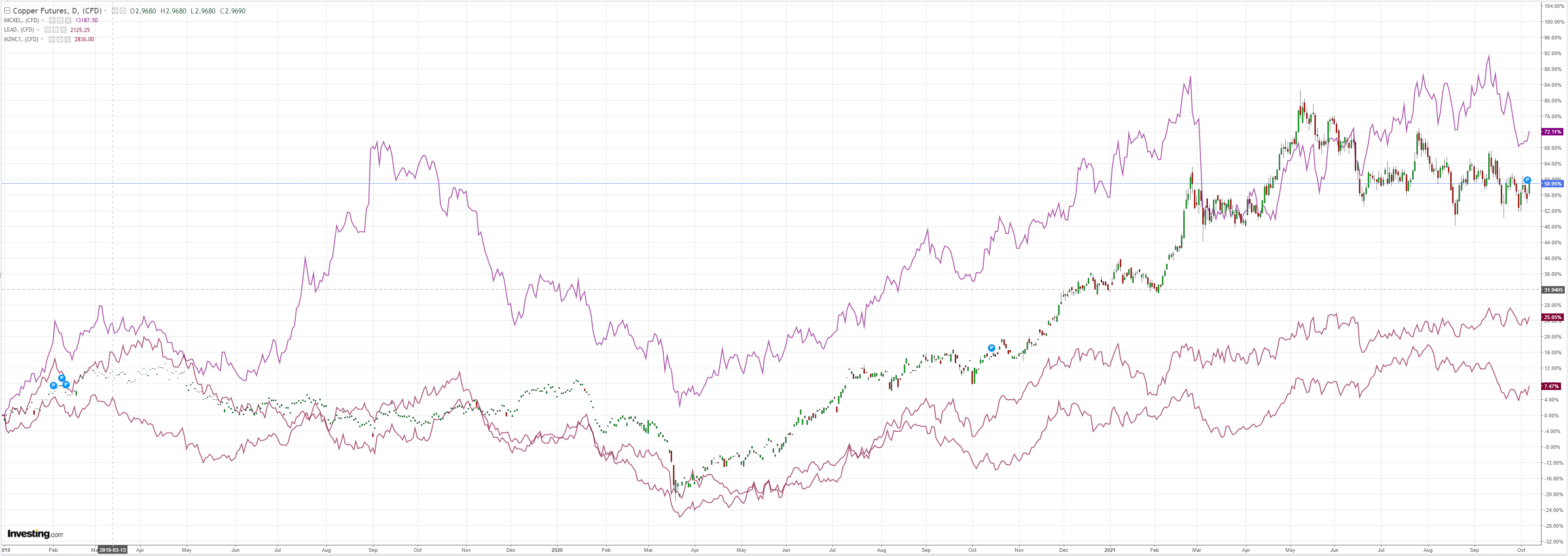

Base metals found a bid:

Big miners too:

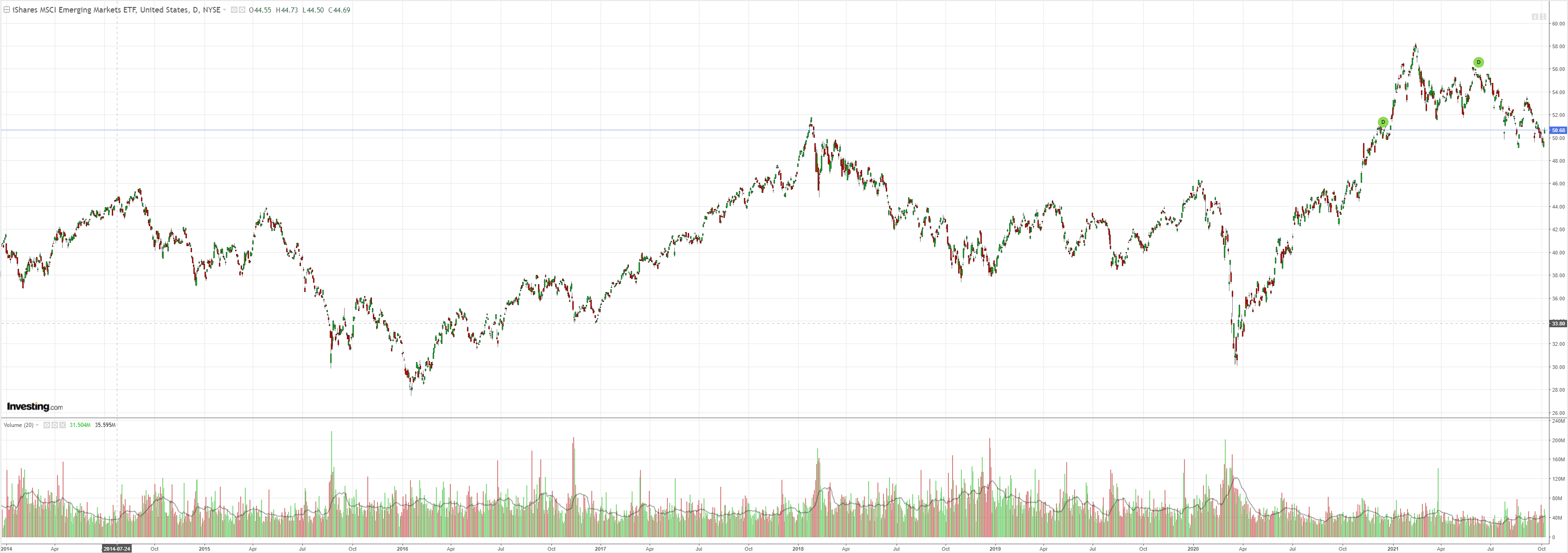

Even EM stocks:

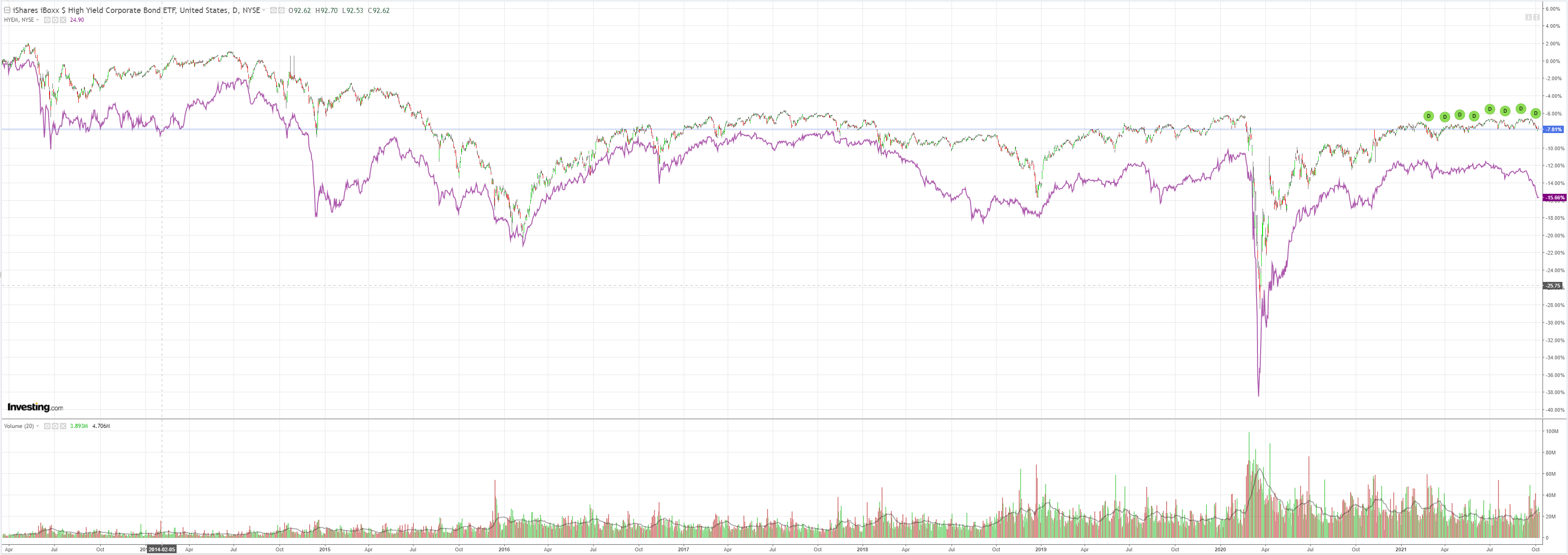

Though junk refused to play:

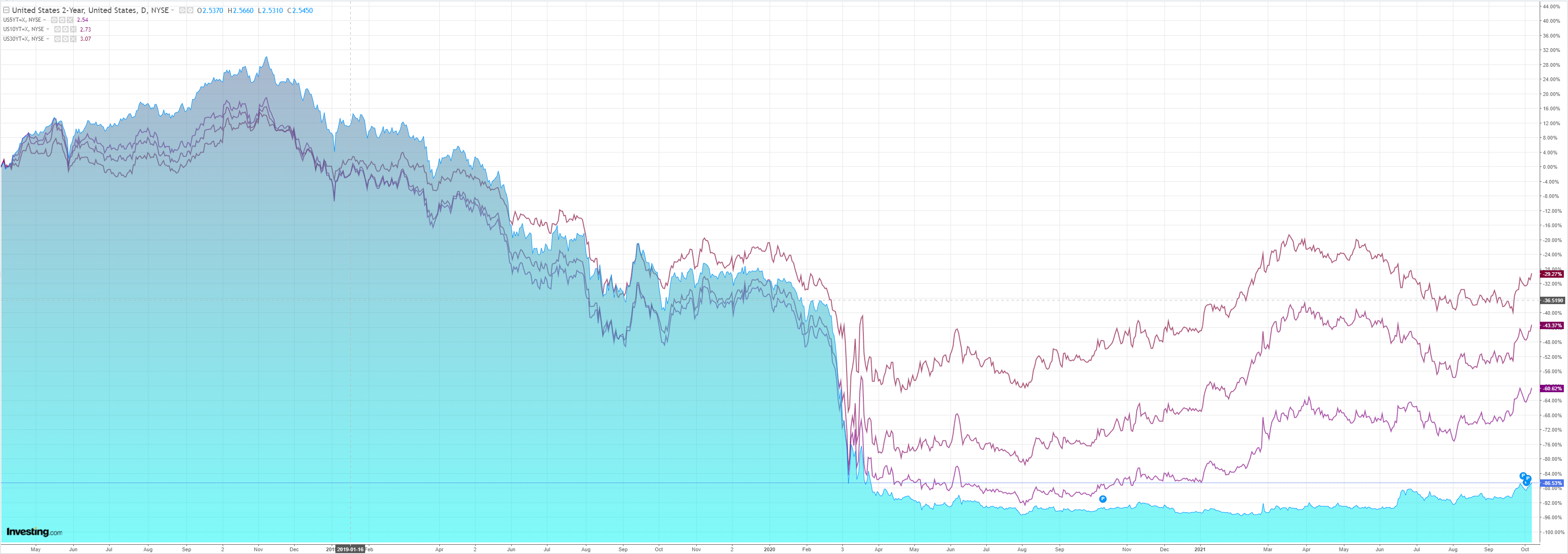

As yields roared higher:

With stocks:

Westpac has the wrap:

Event Wrap

US weekly initial jobless claims were 326k (vs 348k expected, 364k prior), with continuing claims at 2714k (vs 2766k expected, 2811k prior). This data, plus yesterday’s ADP outturn, bode well for Friday’s payrolls data.

FOMC member Mester expects the employment mandate to be reached by the end of 2022. On inflation, there is a lot of uncertainty over the outlook, with both supply and demand factors – mainly pandemic related – boosting inflation. She warned that an increase in inflation expectations could be a sign that prices are being driven more by demand than supply constraints, but that is not her base case. On wages, although they have risen, it hasn’t been a problem given the rise in productivity. She also cautioned that monetary policy should not respond to supply shocks.

Senator Schumer (Democrat) affirmed that a short term debt ceiling deal has been reached, and there will be a vote later today. While the extension is only until is only until December, it does take the immediate risk of a default off the table.

Event Outlook

Australia: The housing market will be a particular focus of the October RBA Financial Stability Review.

China: TheSeptember Caixin China services PMI is expected to rise after the NBS services PMI reported a strong bounce(market f/c: 49.2).

US: Westpac is forecasting a robust print of 600k (market consensus is 500k) for September non-farm payrolls and for the unemployment rate to fall to 5.0% (market at 5.1%), in part because of lagging participation. Lingering supply issues should support average hourly earnings (WBC f/c: 0.4%).

Not much news so we’ll have to put this sudden burst of bullishness down to the debt ceiling can kick and, more importantly, the obvious progress being made in the Biden stimulus.

Nonetheless, I maintain that things are getting worse not better. Biden’s stimulus is a year away from any impact on growth:

- US growth is slowing fast into its fiscal cliff.

- Chinese growth is slowing even faster and its property bust will put the brakes on the European recovery in due course.

- The energy shock is going to make it all worse, and

- trick the Fed into taper while driving up DXY as everything loses steam.

You tell me what comes next:

There’s no doubt the energy crisis is supportive short-term for AUD but I am still bearish.