RateCity has reported that the number of variable mortgage rates on its data base offered under 2% has jumped from 28 to 46 in just two months. Moreover, there are more than three times the number of sub-2% variable rates at the start of the year:

“Since COVID, the battleground for the banks has been fixed rates. However, with record numbers of customers now locked in, some lenders are shifting their sights to variable rates,” said RateCity’s research director Sally Tindall.

“Banks need to be winning new business, not losing it, if they want their loan books to keep moving in the right direction.

“Well over half of all mortgage holders are still on a variable rate. That’s a huge market of potential refinancers for the banks to target.”

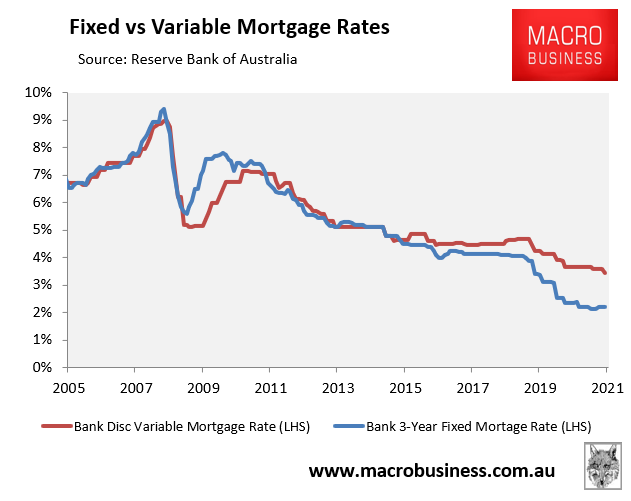

The RBA’s lending indicators data for August showed a similar trend, with the average discount variable mortgage rate falling 0.15% to 3.45% – the lowest recorded rate on record:

Lowest discount variable mortgage rate on record.

By contrast, fixed mortgage rates have begun to edge higher (to 2.19%); although they remained on average 1.26% below variable rates in August, according to the RBA.