From the excellent George Tharenou at UBS Evidence Lab:

2021 UBS EL Mortgage survey implies material deterioration in loan standards

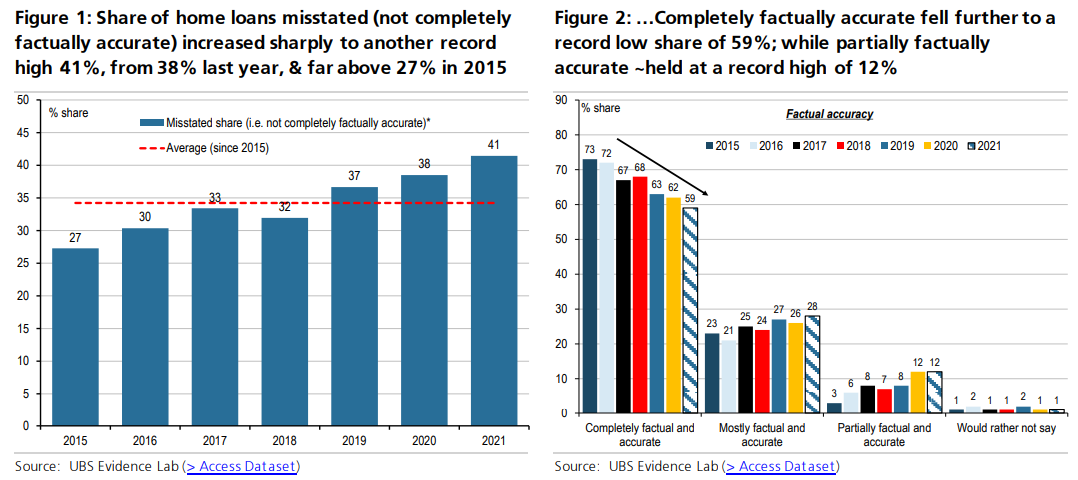

UBS Evidence Lab surveyed ~900 Australians who took a mortgage in the last year – conducted from 21 June to 5 July, at the start of lockdowns in NSW and Victoria. The 2021 vintage is the 7th year. Overall, it suggests a material deterioration of lending standards. The share of home loans misstated (i.e. not completely factually accurate) increased sharply to another record high 41%, up from 38% last year, & far above 27% in 2015. Interestingly, there was a fall in the number of areas where respondents misstated. But, in contrast, the size of misstatement lifted materially – with a much larger over-statement of income (especially by 25%-34%) and assets; with a greater under-statement of financial commitments and living costs (especially by 25%-34%).