Full note from Zero Hedge. I agree with the premises but not the conclsuion for another broad stimulus. At least, not yet. Xi appears committed to giving this reform round a genuine crack.

Something historic will happen this week: as Beijing warned last week, China’s largest and most indebted property developer, Evergrande, will default on some (or all) of its $313 billion in debt. And while some in the financial media are trying to talk down the significance of this event, make no mistake – this will be China’s “Lehman moment”, the only question is whether it will be controlled and contained, or will it be chaotic (i.e.m the “Nightmare Scenario” discussed on Thursday) and lead to worldwide contagion and a global deflationary shockwave. The answer will depend on how Beijing reacts and what it does in response.

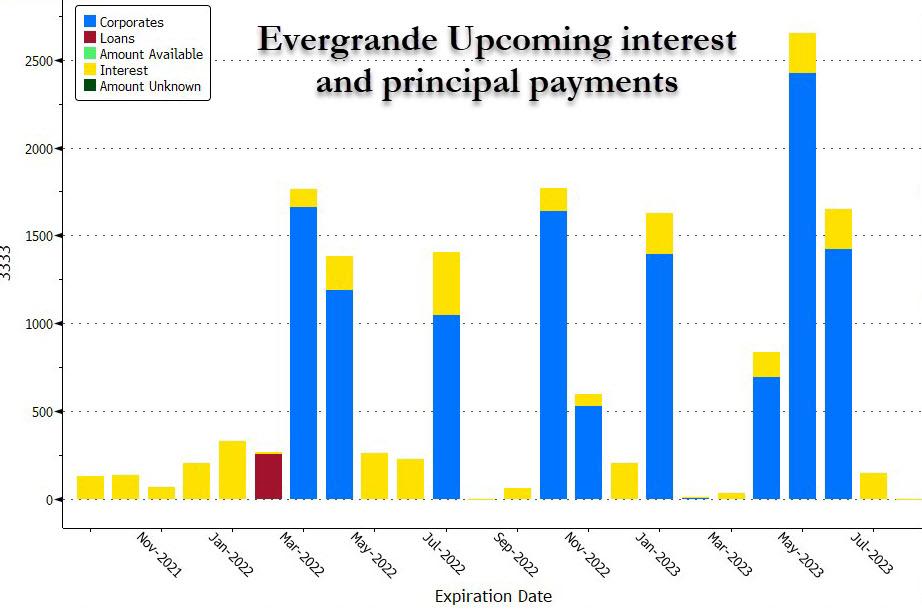

In terms of immediate next steps, the sequence of events is well-known. Evergrande is due to pay $83.5 million of interest on Sept. 23 for its offshore March 2022 bond. It then has another $47.5 million interest payment due on Sept. 29 for March 2024 notes. The bonds will default if Evergrande fails to pay the interest within 30 days, and as shown in the chart below, it’s only downhill from there. We now know that Evergrande will not pay the interest, nor will it pay upcoming principal maturities, meaning that a technical default is just a few days away.