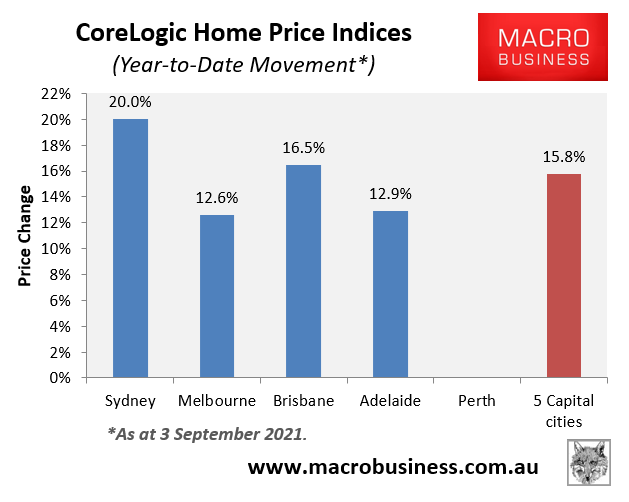

With nearly four months to go this calendar year, Sydney’s dwelling prices today hit 20% growth for 2021:

Note: Perth’s index temporarily suspended.

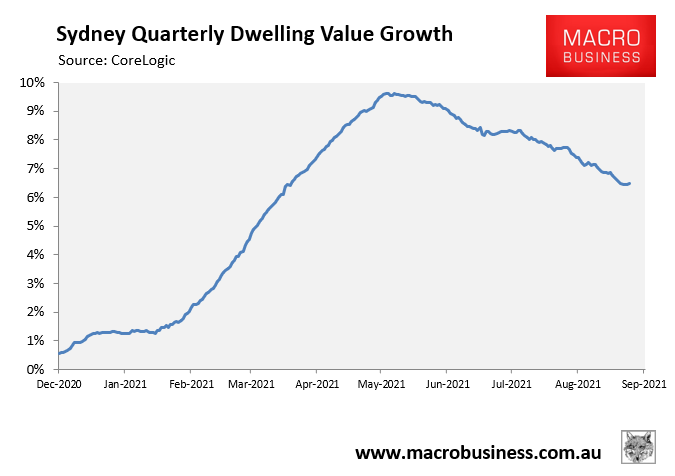

Even with Sydney’ dwelling value growth slowing (see next chart), it is easy to envisage that Sydney property values will grow by more than 25% over the full calendar year:

Growth slowing.

Advertisement

We have not seen a property price boom like this since the late-1980s.