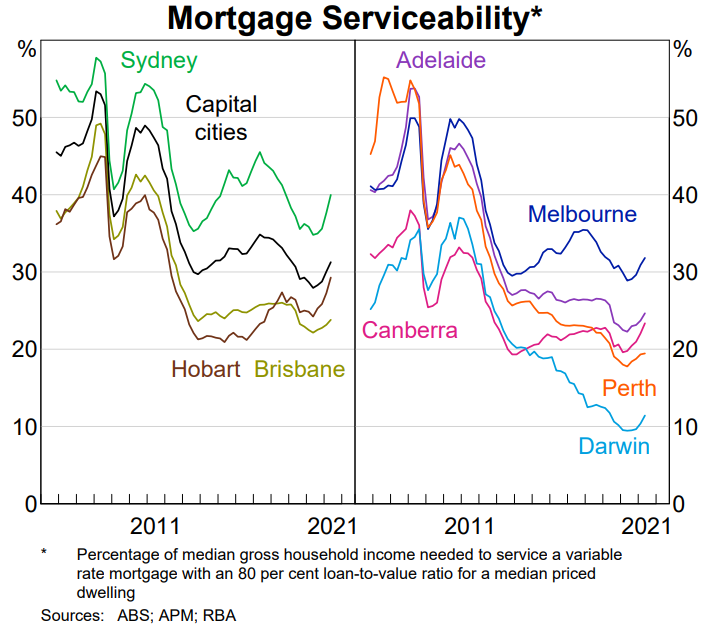

The Reserve Bank of Australia’s (RBA) submission to the House of Representatives Standing Committee on Tax and Revenue’s inquiry into Housing Affordability and Supply suggests that saving for a deposit is the biggest hurdle to home ownership.

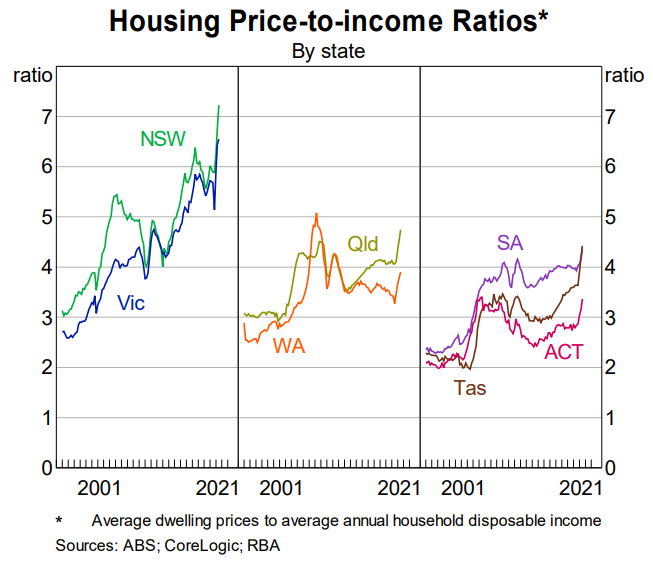

The RBA shows that while the ratio of house prices to income has soared, especially across Sydney and Melbourne:

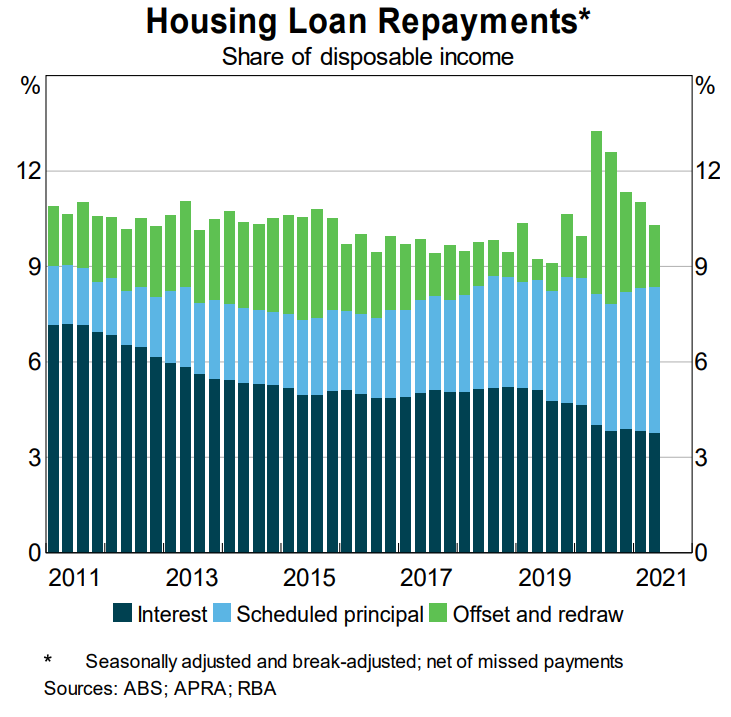

Actual mortgage repayments have shrunk as a proportion of income thanks to falling interest rates:

Advertisement