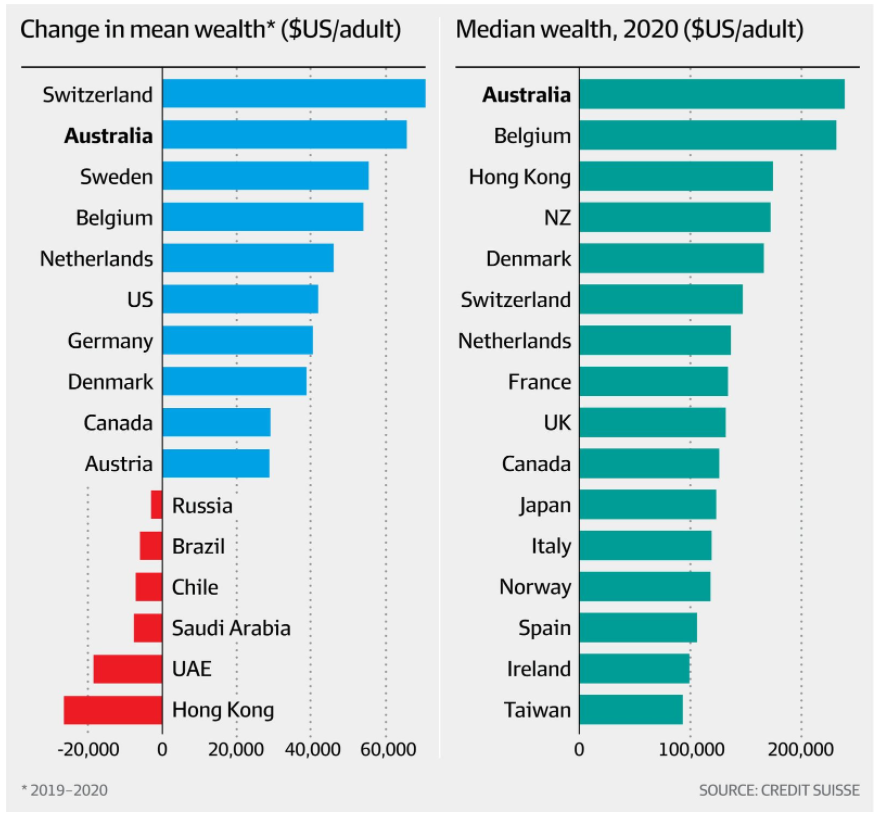

A few months back, the Credit Suisse Global Wealth Report declared Australian households the worlds richest thanks to their expensive property assets:

Aussies top global wealth rankings.

Yesterday, the ABS has released its Finance and Wealth statistics for the June quarter, which revealed a record increase in household wealth on the back of the property boom: