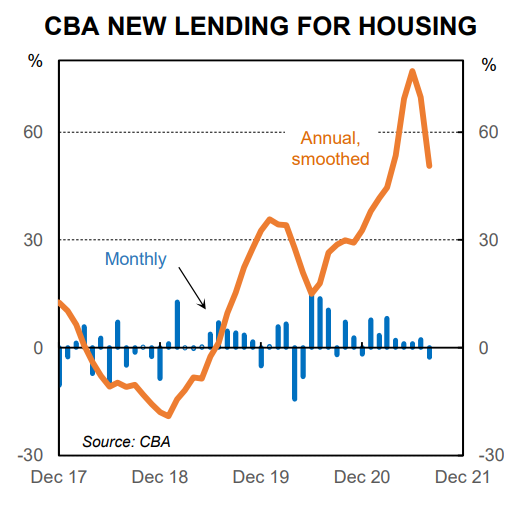

CBA has released internal data on lending, which shows that new mortgage lending eased in August amid lockdowns. The share of fixed rate lending also eased from recent highs:

New lending for housing eased in August, with housing activity dampened by the lockdowns.

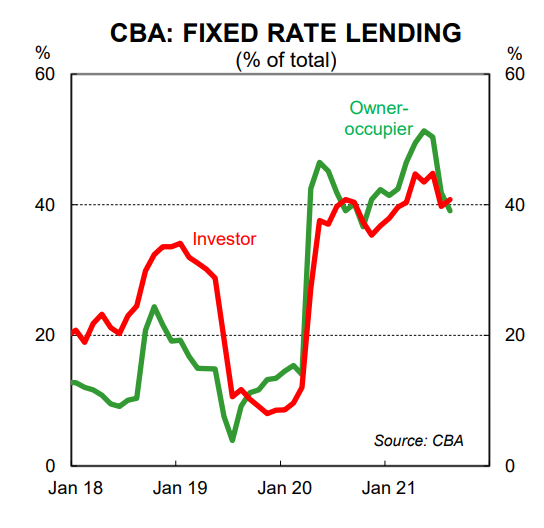

The share of fixed rate lending remains high, but below recent peaks.

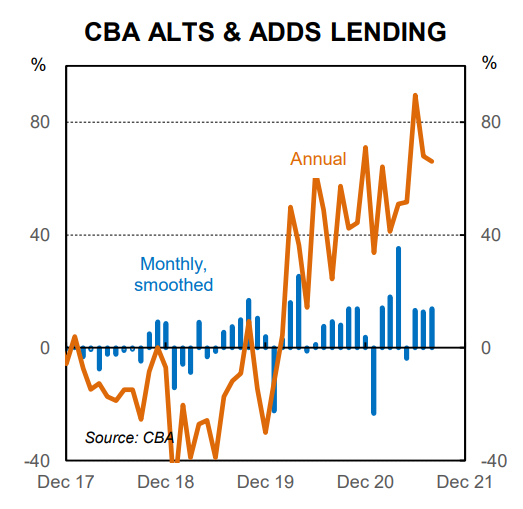

Lending for renovations continued to grow at a solid pace.

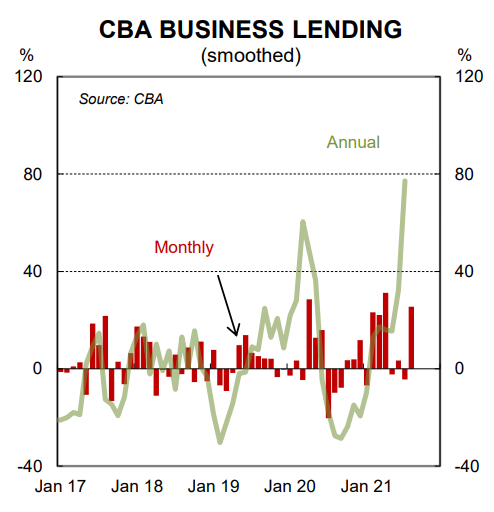

Lending to businesses has lifted over recent months as businesses draw down on existing facilities to support cash flow through the lockdowns.

New lending for housing eased in August. Lockdowns across NSW and Victoria in the month have dampened housing market activity, although prices have been resilient.

The share of fixed rate lending has eased for both owner-occupiers and investors as fixed rates have lifted a little. Nonetheless the share of fixed rate lending is still high.

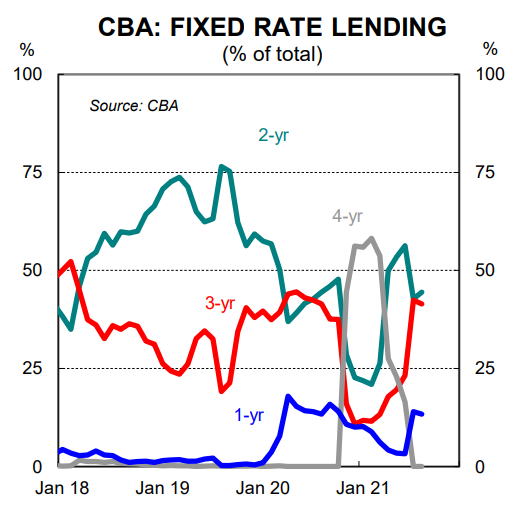

Most fixed rate borrowers fixed at the two or three year horizon.

Lending for renovations is still growing at a solid pace.

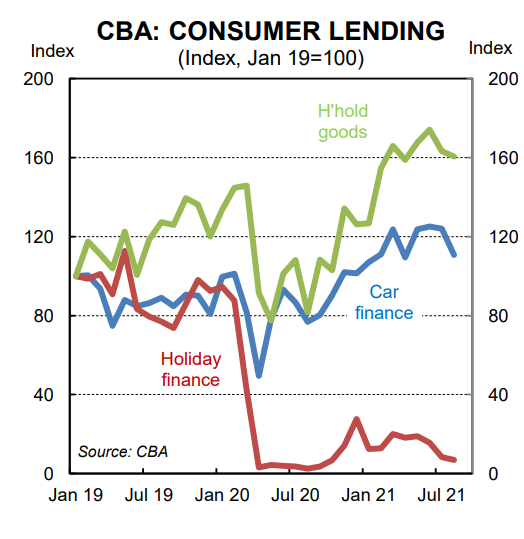

Lending for household goods and cars has pulled back a little. Not surprisingly, given the backdrop of lockdowns and interstate border closures, lending for holidays is very low.

Business lending has lifted over recent months as businesses draw down on existing facilities to support cash flow through the lockdowns.

Usually, the fall in new mortgages would indicate slower price growth. However, it has been met with lower listings and likely sales volumes, which would support values.

Basically, the reduced demand amid lockdowns has been met with reduced supply. Both will rise once lockdowns are lifted.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.