The slew of central bank speeches overnight gave risk markets a small reprieve from the recent selling, helped along by a burgeoning US pending home sales data print but the latest US government shutdown is still causing concern. Treasury yields roundtripped around the 1.5% level after making a three month high while European shares came back as the latest business and consumer confidence figures surprised to the upside. The big moves were in risk currencies as they all sharply fell in the wake of the continued run to the USD, with the majors making new monthly lows in the process while gold fell another 1% again. Commodities were wobbly with oil pulling back as copper and iron ore lifted slightly.

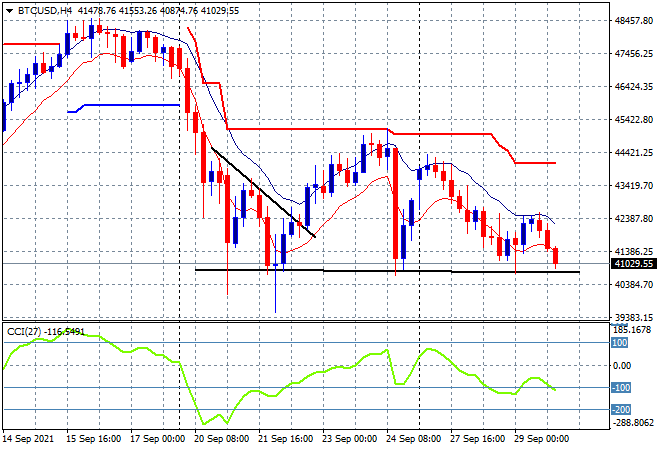

Bitcoin continues to deflate with price heading back to the previous weekly low at just above the $41K level as buying support evaporates without any dump and pump schemes underway to give it a kick higher:

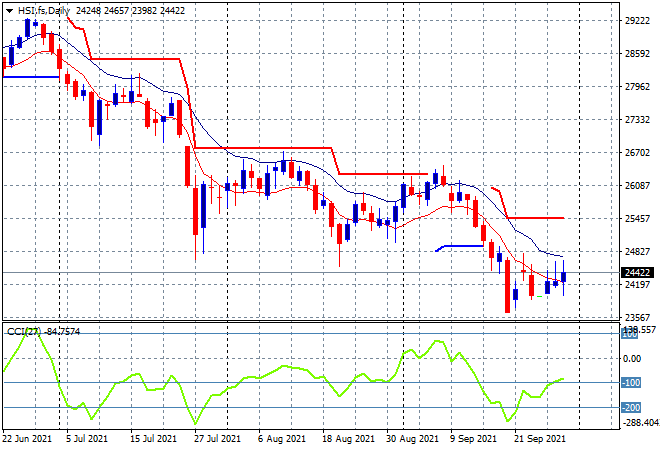

Looking at share markets in Asia from yesterday’s session, the Shanghai Composite gapped significantly lower on the open and struggled going into the close, down over 1.7% to 3540 points while the Hang Seng Index was the odd one out, lifting nearly 0.6% to 24663 points. The daily chart however remains under a lot of pressure here with resistance continuing to build and another downturn below the 23500 level quite likely given overseas markets trends but watch for a potential breakout above the high moving average on the daily chart at the 24800 point level:

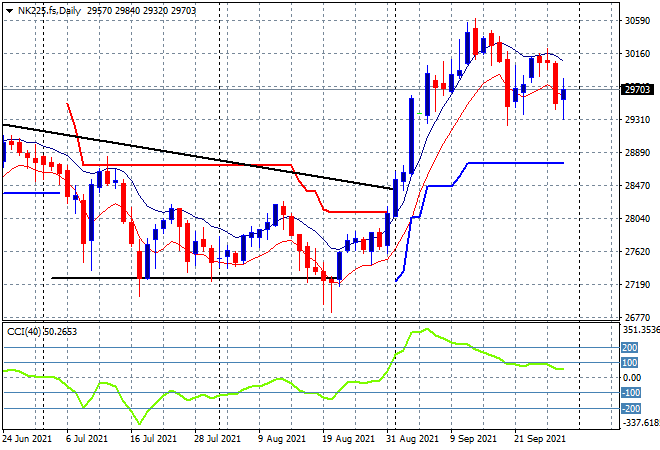

Meanwhile Japanese markets pulled back the strongest despite a new Prime Minister, with the Nikkei 225 closing 2% lower at 29554 points. Futures are indicating a slight uptick on the open today with the lower Yen helping again, so while support is pretty firm at the 29300 point level, a breakout above the 30000 point resistance zone is required before getting excited here:

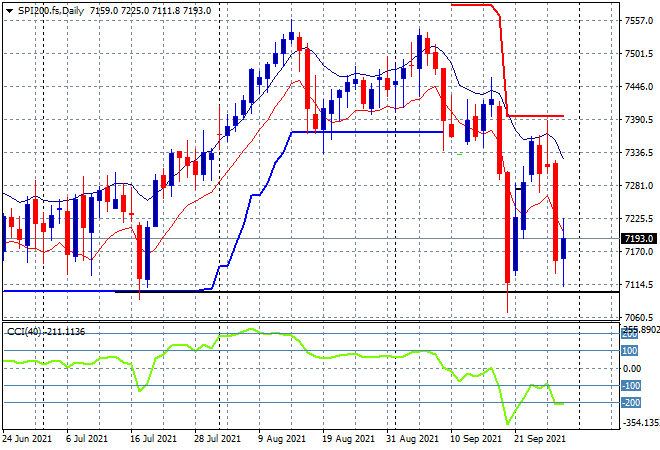

Australian stocks continued their selloff with the ASX200 falling another 1% to break below the 7200 point level, closing at 7196. SPI futures are up 20 points so a small reprieve is likely on the open today given the very small uptick on Wall Street overnight as traders will look for any opportunity to bid the beleagured bourse better. The daily chart had been showing a potential rollover of the dead cat bounce that has now taken it towards monthly support at the 7000 point level that will next come under threat:

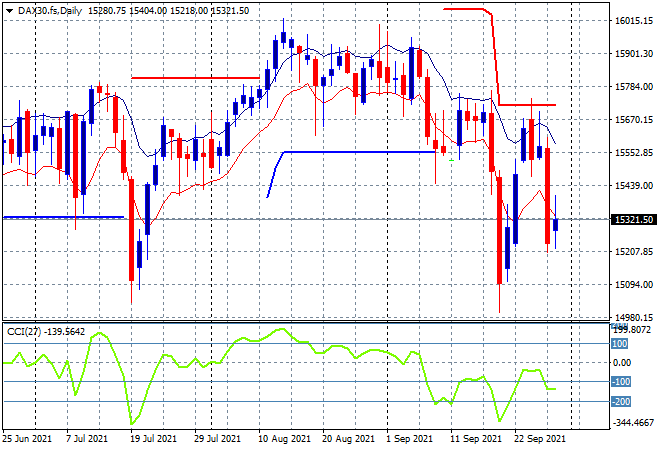

European markets started off more upbeat than expected and kept bidding throughout the session, although the Wall Street open dampened spirits somewhat as the German DAX regained 0.7% to finish at 15365 points. This is only a mild improvement given the overall picture remains quite bearish and daily momentum is still oversold so be wary for a false break here that could see a return to the previous price lows:

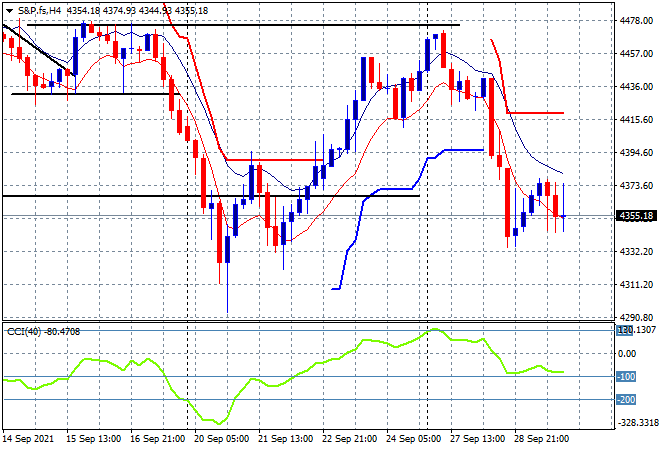

Wall Street was given only a very slight reprieve overnight on the back of Fed Chair Powell’s comments while tech stocks still under pressure as the NASDAQ fell down 0.25% while the S&P500 lifted 0.2% to close at 4359 points. The four hourly chart shows how meek this action was with no real upside potential displayed, as price action remains well below the previous neckline at the 4400 point level. It still hasn’t made a new weekly low which will keep the bulls squeezing out for hope as is momentum, which is not yet oversold here in the short term. Maybe the BTFD crowd is circling:

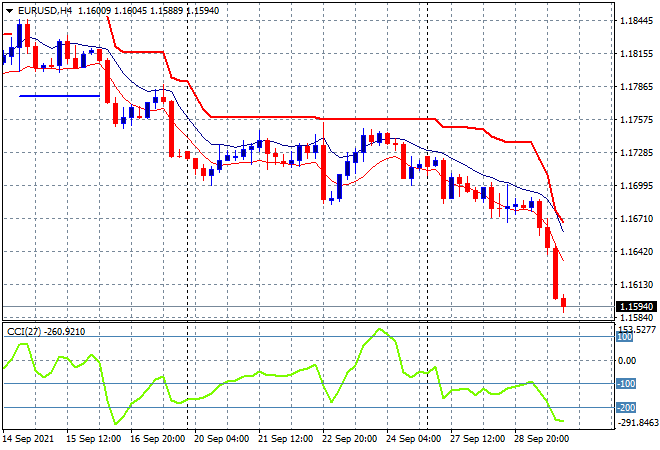

Currency markets continued the strong rise of USD again overnight, with continued selling pressure accelerating against all the majors. Euro slumped the furthest, heading straight below the 1.16 handle in a one-sided selloff that saw it make a new yearly low. Momentum readings remain extremely oversold in the short term with overhead trailing ATR resistance now at the 1.17 level proper, but we could get a small swing back towards the 1.1640 level on a low probability short trade:

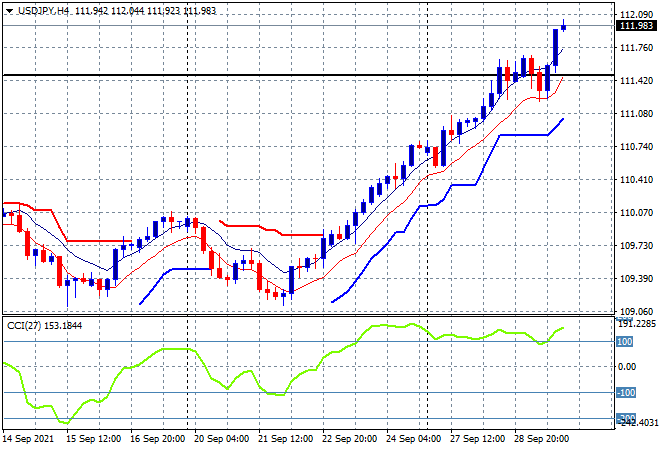

The USDJPY pair zoomed ever higher above the previous pause holding pattern, almost crossing above the 112 handle to create yet another new weekly and monthly high. Momentum remains nicely overbought with certainty around the Japanese election helping matters here with the previous highs at the 111.50 level now providing solid support in the short term:

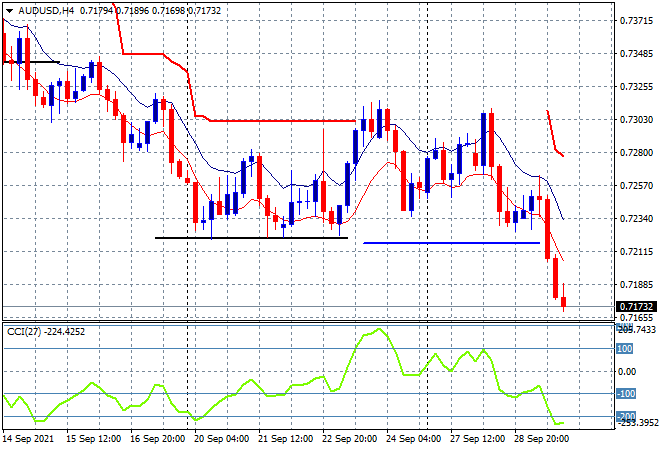

The Australian dollar was poleaxed again overnight after barely finding some intrasession support yetserday at the 72.30 level, breaking right through the previous weekly lows to be well below the 72 level against USD. Momentum readings are extremely oversold but the longer term charts are pointing to more downside below with parity at the 70 major handle the next likely target:

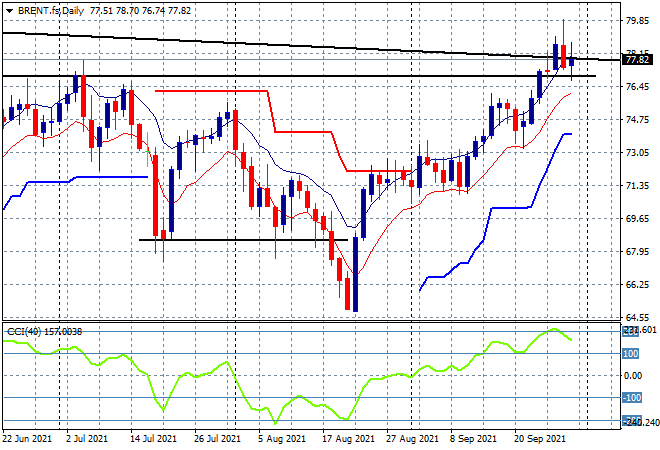

Oil prices were looking to breakout again overnight, after recently making new three year highs but were unable to gain further upside momentum although Brent crude futures managed a small tickup to finish just below the $78USD per barrel level. Price action is still above the medium term downtrend with momentum readings well oversold here and likely to keep filling in as all short positions are wiped out with support at the low moving average level as a great uncle point:

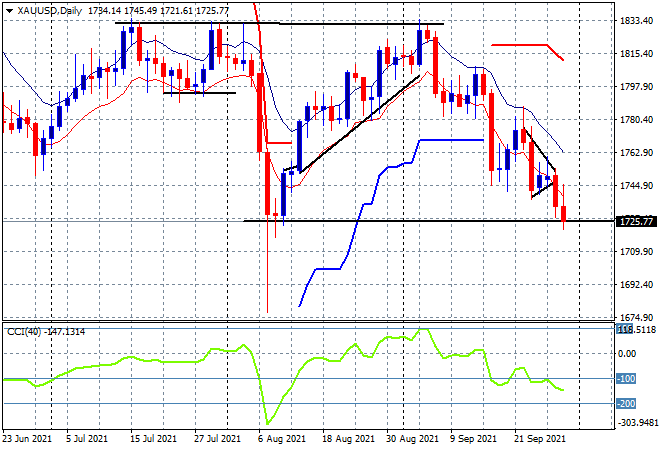

Gold continues its deepdive under the pressure of a very strong USD as it abandoned the $1750USD per ounce support level and fell further below the symmetrical pattern on the bearish daily chart to finish at the $1725USD per ounce level overnight. The full retracement to the previous flash crash lows at the $1700USD per ounce level is quickly coming to pass and if this breaks, there’s daylight below:

Glossary of Acronyms and Technical Analysis Terms:

ATR: Average True Range – measures the degree of price volatility averaged over a time period

ATR Support/Resistance: a ratcheting mechanism that follows price below/above a trend, that if breached shows above average volatility

CCI: Commodity Channel Index: a momentum reading that calculates current price away from the statistical mean or “typical” price to indicate overbought (far above the mean) or oversold (far below the mean)

Low/High Moving Average: rolling mean of prices in this case, the low and high for the day/hour which creates a band around the actual price movement

FOMC: Federal Open Market Committee, monthly meeting of Federal Reserve regarding monetary policy (setting interest rates)

DOE: US Department of Energy

Uncle Point: or stop loss point, a level at which you’ve clearly been wrong on your position, so cry uncle and get out!