Equity markets continue to bounce back as central backs continue to not surprise, following the Fed meeting we had the BOE and Swiss banks overnight still steady as she goes, leading to risk currencies rising across the board as the USD continued to fallback. Gold and silver remained under pressure however while Treasury bond yields saw a big tick up, with the 10 year trading above the 1.4% level. Commodities were slightly mixed and while oil broke out to new highs, copper pulled back and iron ore rose another 3% after its epic bounce in the previous session.

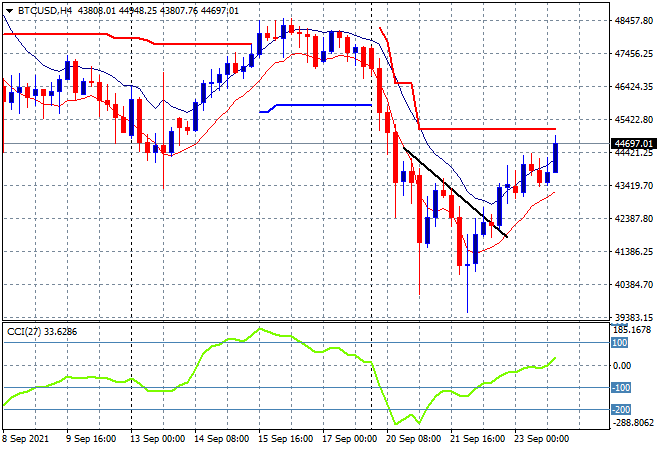

Bitcoin continued its own swing move higher overnight, putting in a strong final session to be just below the $45K level this morning. This almost completes a volatile V-pattern that has seen over 30% of total directional change this week!

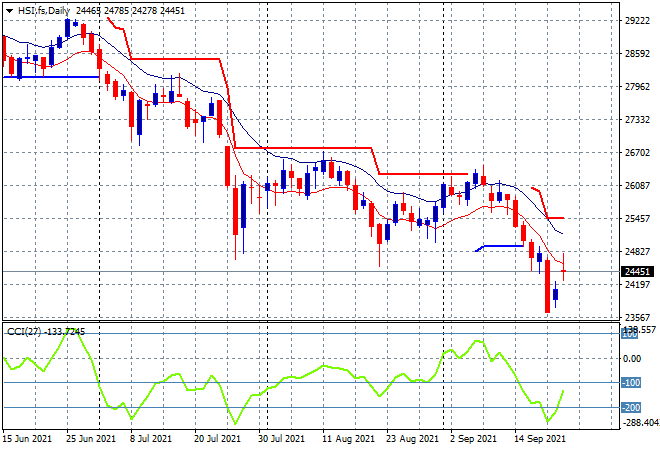

Looking at share markets in Asia from yesterday’s session, where the Shanghai Composite had a mild uptick, closing 0.4% higher at 3642 points with the Hang Seng Index reopening and launched 1% higher to finish at 24510 points but is still not yet out of trouble. The daily chart remains poised here but the recent oversold action and too pessimistic sentiment could be the precursor to a swing back higher, so watch for a move above the 25000 point level to bring price at least back to the recent weekly lows experienced in July:

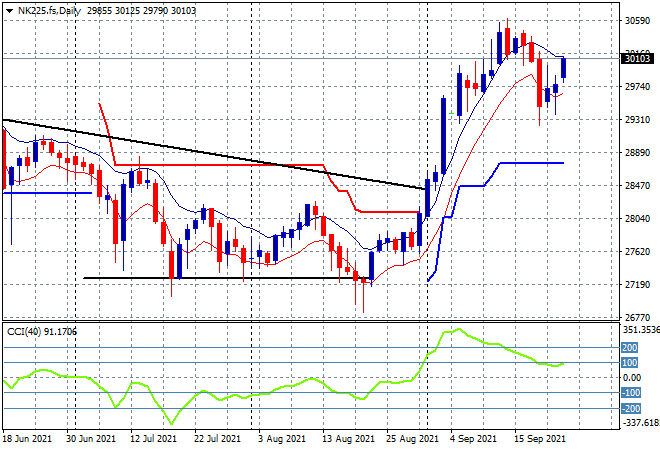

Japanese stock markets were closed for yet another holiday with Nikkei 225 futures indicating a surge higher on the open today with the 30000 point level to likely be breached. Support is now fairly obvious at the 29300 point level so if Yen remains depressed we could see more upside here setting up for the next trading week:

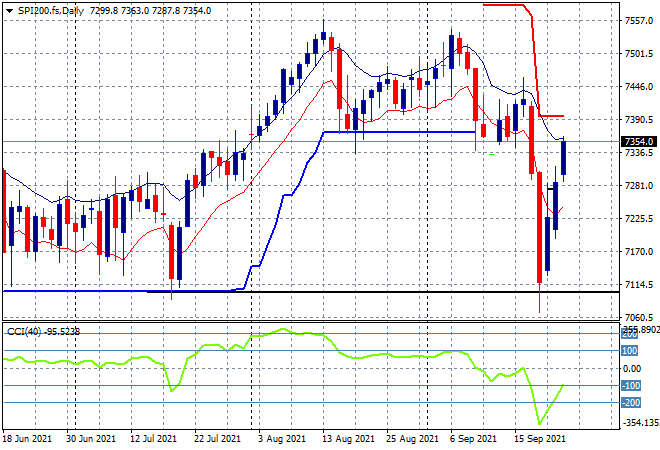

Australian stocks put in a very solid session, with the ASX200 finishing exactly 1% higher at 7370 points as price gets back to previous medium term support and almost fills out the current dip action. SPI futures are up around 10 points or so with the daily chart showing the potential to finish the week above previous support as this swing trade continues. Notably however, daily momentum is not yet positive so until that level is broken through again this dip is not yet over:

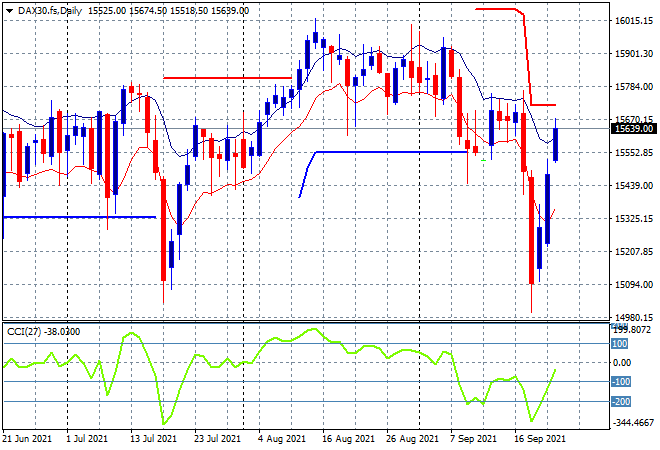

European markets were green across the board, except the FTSE which tread water after the BOE meeting, with the German DAX gapping 0.9% higher at 15643 points. The daily chart is similar to other equity markets with a sharp dip that has been nearly filled although a case can be made that support is better here with price back above previous ATR support at the 15500 point level. A higher Euro maybe a barrier to further price increases however with the next level of resistance not that far away:

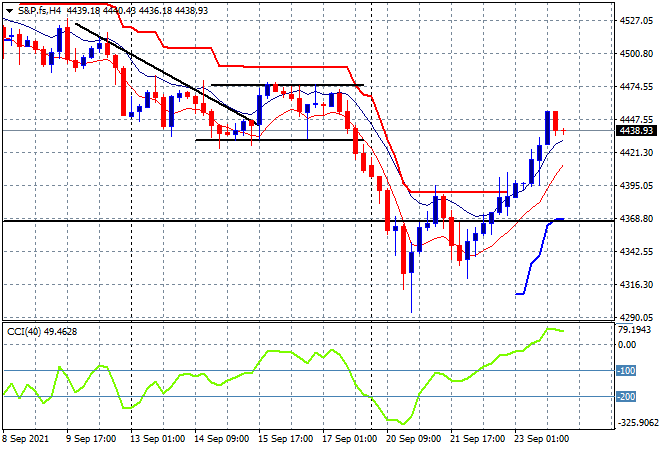

Wall Street surged back the strongest as hope overruled fear once again, with the NASDAQ up 1% while the S&P500 shot up even higher, lifting 1.2% to close at 4448 points. This takes price well above the neckline at the 4400 point level of that large head and shoulders pattern on the daily chart and back above the July lows in a classic dip filling play. Momentum is back to a positive setting in the short term at least with the 4500 point resistance level the next upside target:

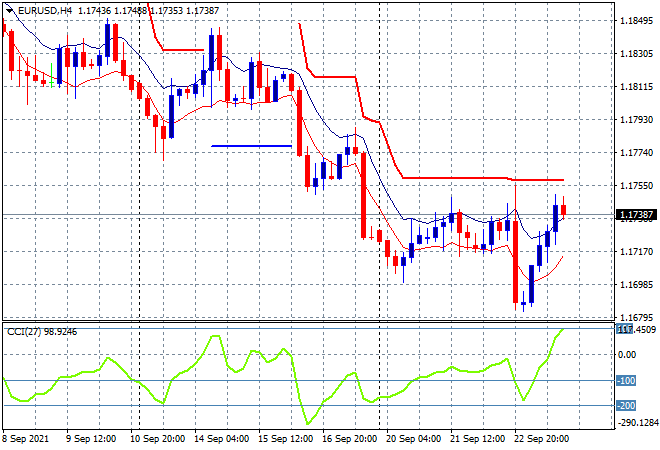

Volatility returned to currency markets with the USD broadly sold off as Euro finally broke out of its tight trading range with an initial breakdown that proved false below the 1.17 handle before returning to the previous short term resistance level. Momentum is now positive again but overhead trailing ATR resistance at the mid 1.17 level is not cleared at all so this may well turn into another false play:

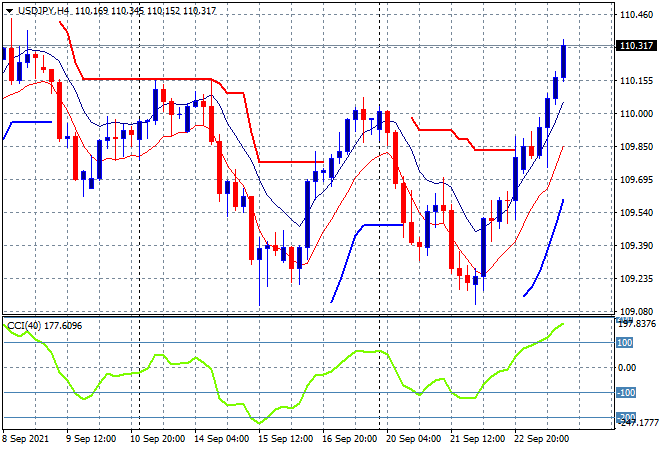

The USDJPY pair continues to act as a risk proxy and this time proved even better in terms of short covering as Yen sold off sharply through the 110 handle to a new weekly high! This is putting a lot of pressure on the medium term trend even, with momentum nicely overbought now but price actions seems to be accelerating far too quickly, so watch for a potential reversion back to the 110 level proper:

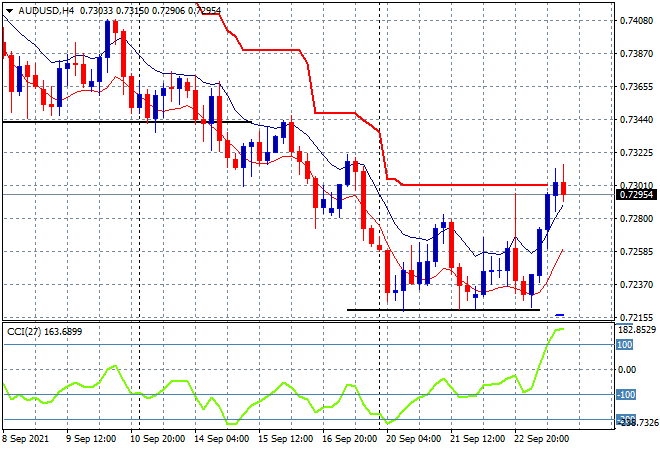

The Australian dollar was also able to break out, following the trajectory of iron ore once more, pushing up to but not through the 73 handle overnight. Overhead ATR resistance remains very solid here and could prove an anchor point going forward:

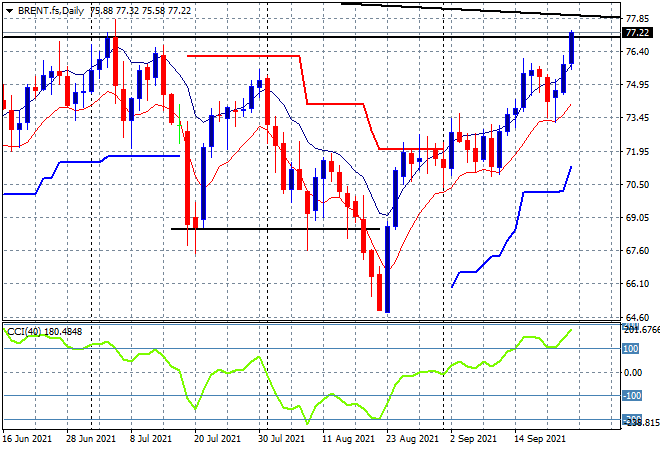

Oil proved the best movers overnight in terms of providing some big catalysts for longs to pour in. Brent crude finished more than 1% higher, breaking through the previous weekly and daily highs at the $77USD per barrel level with price action almost pushing through the medium term downtrend. Momentum readings are poised here to continue higher with building support at the low moving average level as a great uncle point:

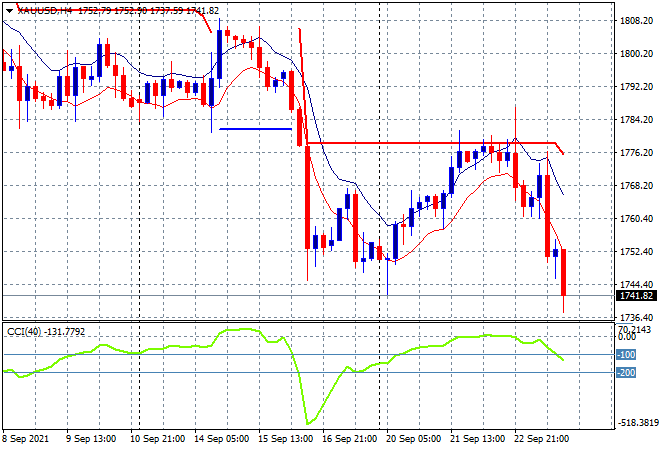

Gold however was the odd one out with central back action (or lack of action) going against the shiny metal, pushing it significantly lower overnight to the $1741USD per ounce level. The four hourly chart is very illustrative on how overhead resistance that had been building mid week was unable to be cleared, resulting in an abandoning of long positions. As I said previously, we could see a full retracement to the previous flash crash lows at the $1700USD per ounce level:

Glossary of Acronyms and Technical Analysis Terms:

ATR: Average True Range – measures the degree of price volatility averaged over a time period

ATR Support/Resistance: a ratcheting mechanism that follows price below/above a trend, that if breached shows above average volatility

CCI: Commodity Channel Index: a momentum reading that calculates current price away from the statistical mean or “typical” price to indicate overbought (far above the mean) or oversold (far below the mean)

Low/High Moving Average: rolling mean of prices in this case, the low and high for the day/hour which creates a band around the actual price movement

FOMC: Federal Open Market Committee, monthly meeting of Federal Reserve regarding monetary policy (setting interest rates)

DOE: US Department of Energy

Uncle Point: or stop loss point, a level at which you’ve clearly been wrong on your position, so cry uncle and get out!