The USD fell back again overnight as the weekly initial jobless numbers were slightly lower than expected, setting up for a dovish NFP print tonight that will set the risk taking for the month ahead. Notably, US GDP estimates have been pulled back which will add to the “don’t taper too soon please” dogma on Wall Street, which of course raced to a new record high. Risk currencies moved higher again while Treasury yields were relatively calm in a tight trading range and oil prices finally found some life with Brent crude futures lifting nearly 2%.

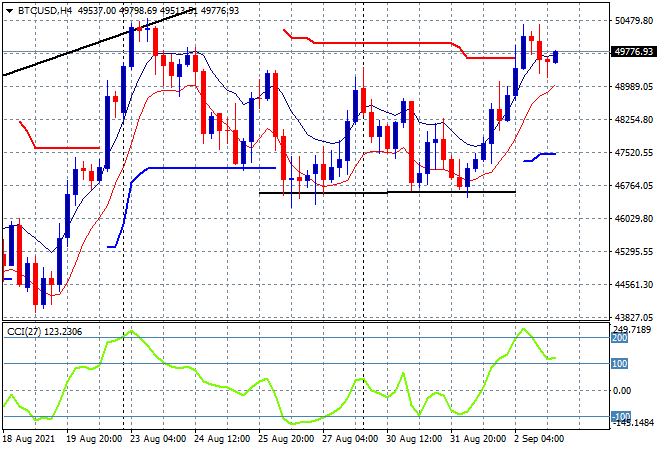

Bitcoin continued its bounce and just pushed through the $50K level but was thwarted and unable to make a new weekly high, stalling just below that level this morning. It may have another go tonight, watch for the low moving average to be supported at the $49K level on the four hourly chart:

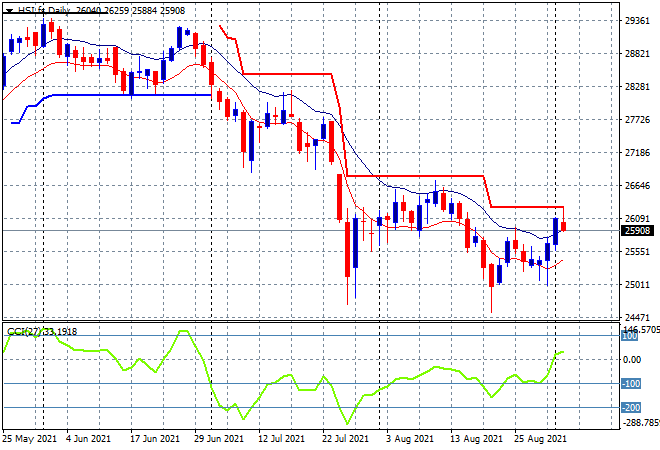

Looking at share markets in Asia from yesterday’s session, where the Shanghai Composite has closed nearly 0.9% higher, building on its breakout above the 3500 point level, finishing just shy of 3600 points. Meanwhile the Hang Seng Index managed to stay just above the 26000 point level but only just, lifting 0.2% to finish at 26090 points. The daily chart is still struggling to properly put in a bottom pattern, and while price cleared its own high moving average its still shy of trailing ATR resistance above the 26000 point level. Early days yet, but watch for a follow through above to enact a new reflation rally:

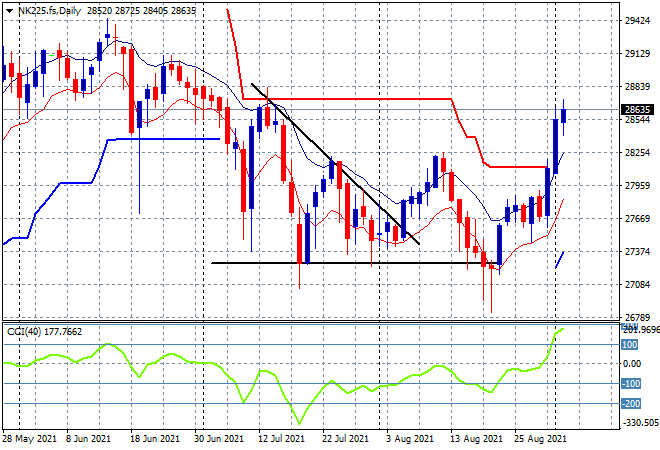

Japanese stocks continued their own breakout, with the Nikkei 225 finishing 0.3% higher to close at 28543 points. The daily chart shows price decisively bursting through ATR trailing resistance above the 28000 point level confirming a new uptrend with daily momentum nicely overbought and ready to move higher with the previous June highs at the 29000 point level the target here:

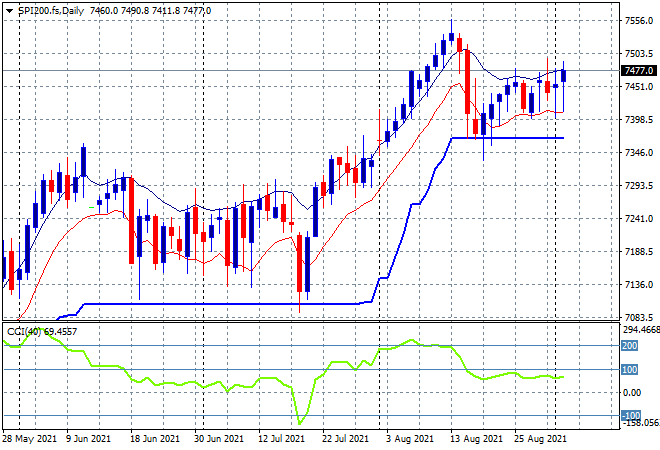

Australian stocks continued to pullback with the ASX200 stalling yet again, closing 0.5% lower to break below the 7500 point level, finishing at 7485 points. SPI futures are up nearly 20 points so far with the daily chart still looking a bit tepid here, so we’re likely to see a stalled finish to the trading week as price still needs to clear its own high moving average and remain well above ATR support at the 7360 point level:

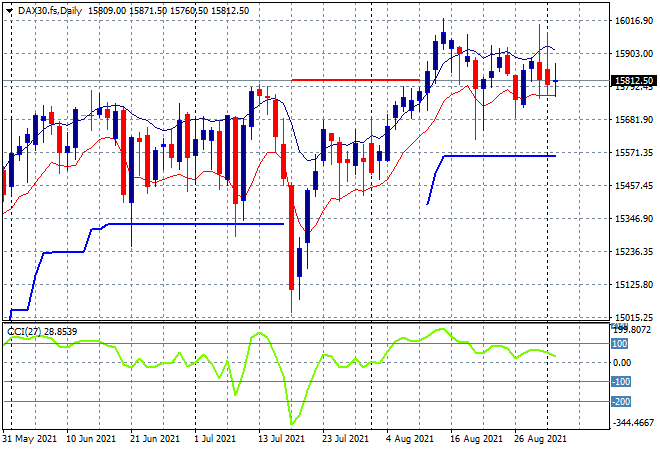

European markets muddled through yet more scratch sessions, this time all through the continent and in Brexit land with the German DAX closing only 0.1% higher at 15840 points. The daily chart is showing more and more hesitation with a continued failure to make any new daily highs or clearing of the high moving average since early August, with resistance firming at the 16000 point level. Its hard to be bullish here, so step up with some volatility plays instead:

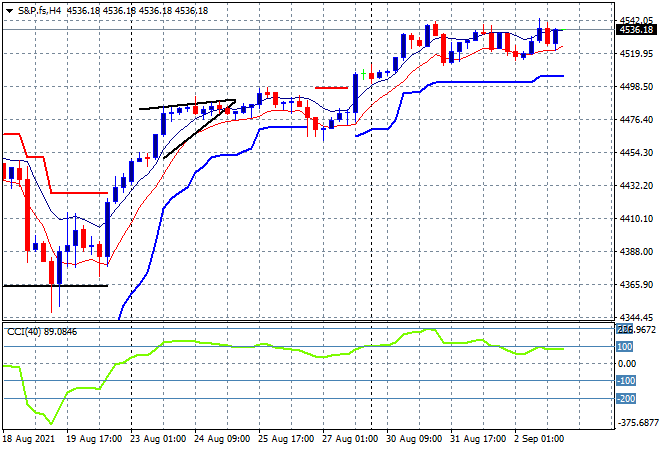

But it was green across the board on Wall Street with the S&P500 eventually putting in a new record high, closing 0.3% higher at 4536 points. The four hourly chart shows prices continuing to base around the 4500 point level with short term momentum still below previous overbought levels. Going into tonight’s NFP print, we could see a mild pullback to ATR support at the 4500 level proper before the BTFD crowd inevitably steps in once again:

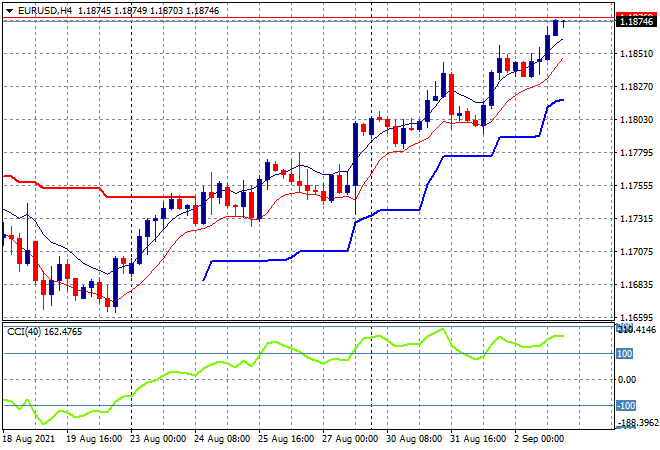

Currency markets saw a continued weakness in USD following the initial jobless prints with Euro moving ever higher, surging towards the 1.19 handle. Momentum remains nicely overbought here and ready for another leg higher, but watch for the inevitable volatility around the NFP print tonight with trailing ATR support at just above the 1.18 level on the four hourly chart a potential target:

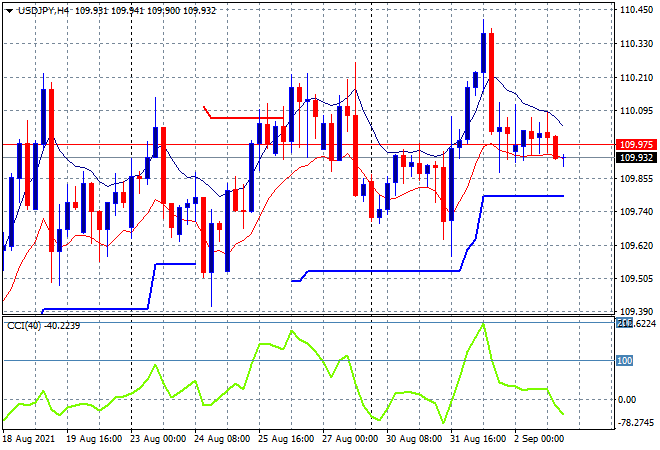

The USDJPY pair was quite contained instead, staying down on the mat just below the 110 handle after its violent slam back previously with the four hourly chart showing a lot of intrasession volatility indeed. This builds on a very hesitant sideways pattern for the last couple of weeks and will require a solid move above the 110.20 level at least to get things moving:

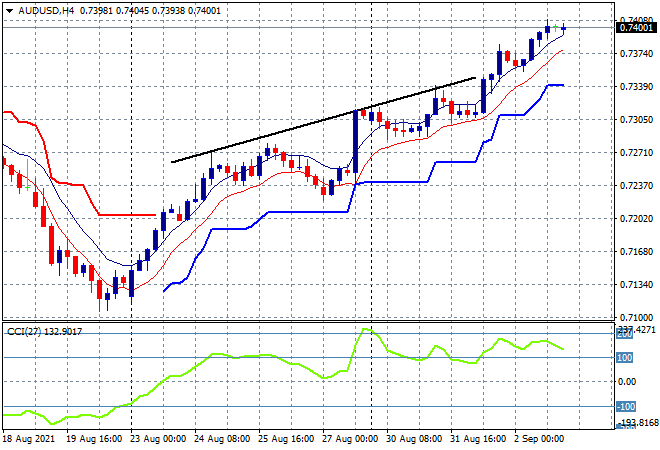

The Australian dollar continues to surge upward on USD weakness, rising above the bullish trendline from the series of highs from last week’s reflation trade to finally crack the 74 handle for another new weekly high. Momentum remains nicely overbought on the four hourly chart but this could be smacked down to trailing ATR support soon if tonight’s NFP print goes awry, so watch for some volatility plays and hedges ahead:

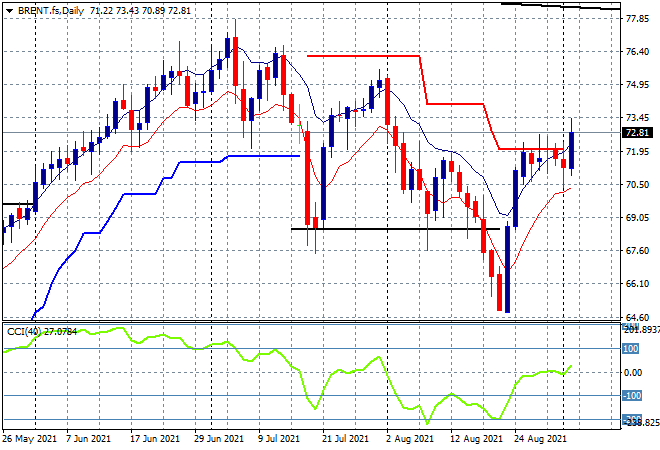

Oil prices are finally getting some headway with a solid breakout overnight helped by the lower USD, with Brent crude pushing up solidly through to almost above the $73USD per barrel level, finally making a new daily high and switching to positive daily momentum. This pushes it back above key overhead trailing ATR resistance level on the daily chart but still below the previous daily highs in late July/early August, so watch for daily momentum to build from here and have another go at the $75 level ahead:

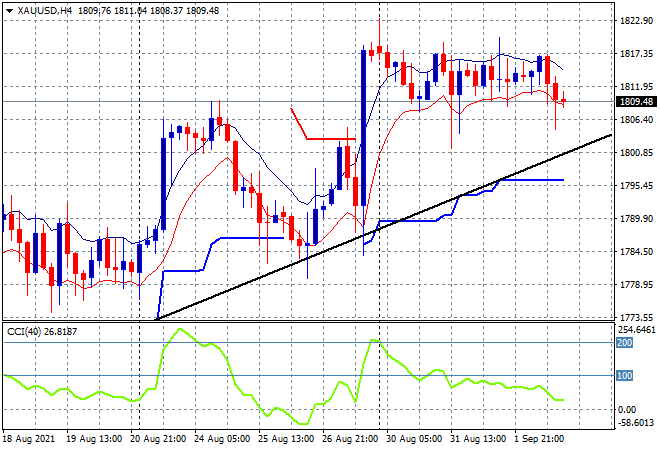

Gold is still in a holding pattern waiting for the right catalyst to springboard it higher with a droopy session overnight despite a weaker USD that put in a new daily low at the $1809USD per ounce level. While previous resistance has been pushed aside, the question still remains if it can make it back to the mid July $1830 highs as daily momentum needs to exceed overbought levels for a proper rally:

Glossary of Acronyms and Technical Analysis Terms:

ATR: Average True Range – measures the degree of price volatility averaged over a time period

ATR Support/Resistance: a ratcheting mechanism that follows price below/above a trend, that if breached shows above average volatility

CCI: Commodity Channel Index: a momentum reading that calculates current price away from the statistical mean or “typical” price to indicate overbought (far above the mean) or oversold (far below the mean)

Low/High Moving Average: rolling mean of prices in this case, the low and high for the day/hour which creates a band around the actual price movement

FOMC: Federal Open Market Committee, monthly meeting of Federal Reserve regarding monetary policy (setting interest rates)

DOE: US Department of Energy

Uncle Point: or stop loss point, a level at which you’ve clearly been wrong on your position, so cry uncle and get out!