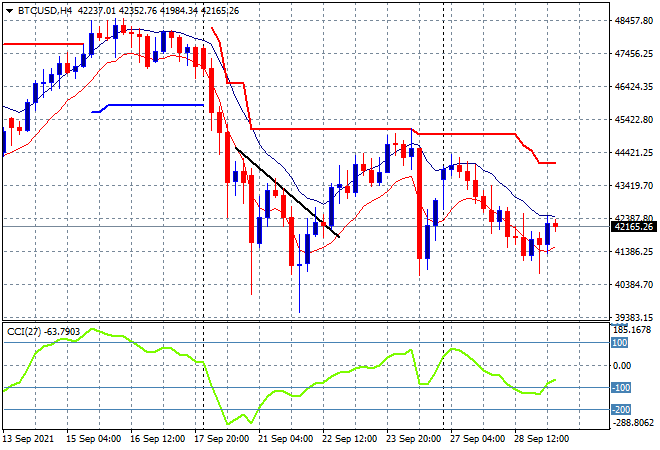

Asian stocks are selling off sharply due to regional and internal problems, let alone the falls on Wall Street overnight in the wake of the latest chicanery in the US Congress (aka the opposite of Progress) as the bond market leads the way as yields spike to new monthly highs. The USD remains relatively firm against most of the risk currencies although the Australian dollar is trying in vain to make a comeback, gold remains under pressure as it makes a new monthly low. Meanwhile Bitcoin is trying to bounce off its recent lows at the $40K level but is looking pretty weary here on the four hourly chart with short term momentum rolling over:

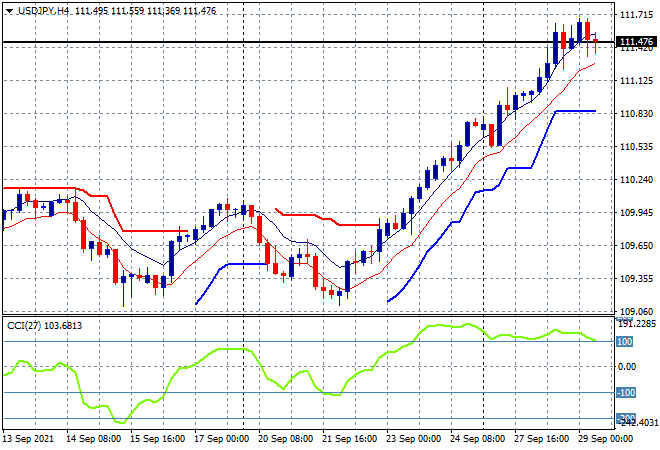

The Shanghai Composite gapped significantly lower on the open and is struggling going into the close, down over 1.7% to 3540 points while the Hang Seng Index remains the odd one out, lifting nearly 0.5% to 24638 points. Meanwhile Japanese markets are pulling back the strongest despite a new Prime Minister, with the Nikkei 225 closing 2% lower at 29554 points as the USDJPY pair again pauses at the mid 111 level as momentum wanes:

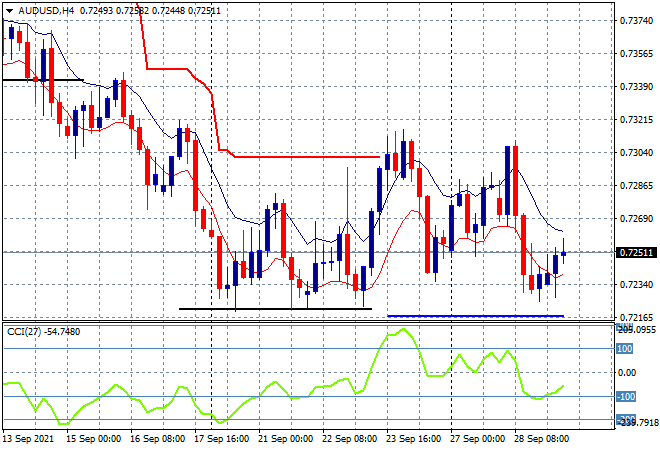

Australian stocks continued their selloff with the ASX200 falling another 1% to break below the 7200 point level, closing at 7196, still not getting any help from a slightly rising Australian dollar which is hovering above the 72 mid level after almost putting in a new weekly low:

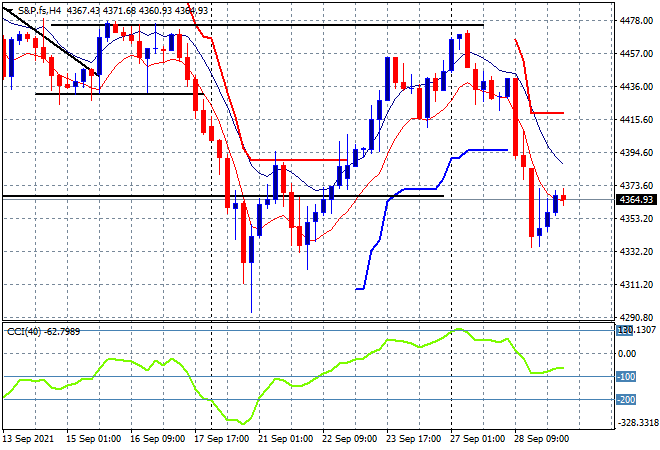

Eurostoxx and S&P futures are up nearly 0.4% or so going into the London open, with the four hourly chart of the S&P500 showing price inevitably bouncing back from last night’s swift move lower. This is all relative however and while price never made a new weekly low, and nor is momentum not yet oversold, its pretty close so this could be just a short term swing with the 4400 point level proving steady resistance:

The economic calendar includes the latest Euro-wide consumer confidence print, followed by a slew of central banker speeches including Powell and Lagarde.