By Tim Lawless, Research Director at CoreLogic

Freshly listed housing stock is starting to lift as the spring selling season begins to heat up.

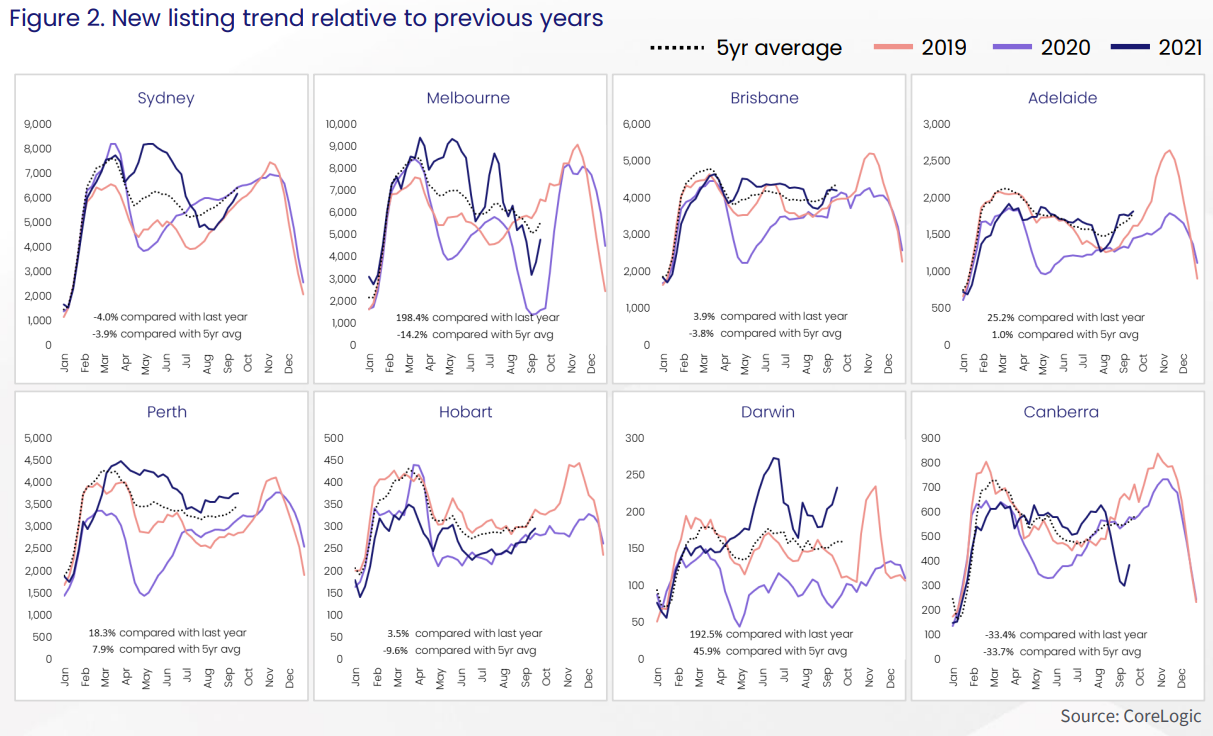

Every Australian capital city has seen a lift in the number of new real estate listings over recent weeks, with some of the largest listing increases recorded in those capitals navigating lockdown. Despite this, the new listings trends remain below the five-year average in every capital apart from Adelaide, Perth and Darwin.

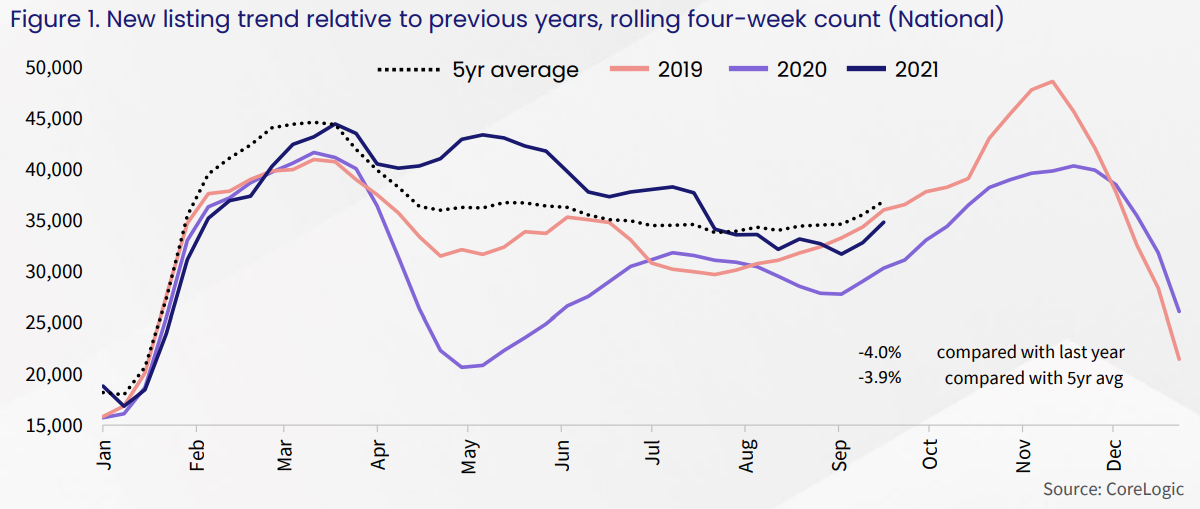

Nationally, new listings bottomed out over the four weeks ending September 5th with just 31,731 new listings added to the market, the lowest volume since the seasonal low in January this year. While new listings have since lifted by 9.8%, the

number of new listings is currently -21.6% lower than the recent high in March and -3.9% below the five-year average for this time of year.

The largest lift in new listing numbers has been in Melbourne, where the rolling four-week count reached a recent low in the first week of September when only 3,230 new listings were added to the market. Since then, the trend in new listings has

surged 48.5%. Recently eased restrictions on property inspections will have added to the lift in new listings, however there was already upwards movement prior to the announcement on September 17th. Figures show Melbourne’s new listings trends have been extremely volatile, falling sharply through each of the five lockdowns to-date, before rebounding quickly once restrictions were lifted.

Sydney hasn’t shown the same volatility as Melbourne; partly due to fewer lockdowns, but also because restrictions did not prohibit private one-on-one inspections. As a result, the rolling four-week count of new listings has steadily risen since mid-August. Based on the count of new listings as at September 19th, freshly advertised listings are up 31%, but remain -3.9% below the five-year average for this time of the year.

In Canberra, where residents are also navigating an extended period of lockdown, the new listings trend has increased by 28% since finding a low last week. Up until midnight on Friday September 17th physical property inspections were prohibited

in Canberra. With these rules now eased, it’s likely the new listings trend will ramp up more substantially.

At the opposite end of the spectrum are the cities that have mostly avoided lockdowns. In Perth, the new listings trend is tracking 7.9% above the five-year average and up 18.3% compared with the same period last year. Darwin listings are rapidly trending higher, 45.9% above the five-year average, while Adelaide’s new listings trend is 1.0% above average.

Brisbane’s new listings trend was suffering from a lockdown hangover, which had dragged the rolling four-week count of listings lower. While the hangover appears to be lifting, the upwards shift is mild and the count of new listings remains – 3.8% below the five-year average.

The new listings trend in Hobart has held consistently below average levels throughout 2021, which is likely a key contributing factor to the rapid rate of appreciation in housing values – up 24.5% over the past 12 months and the highest annual growth rate of any capital city. The new listings trend is ramping up, but remained -9.6% below the five-year average over the four weeks ending September 19th.

An increase in fresh listings will be a welcome relief for real estate professionals and prospective buyers. However, total active listings remain -29% below the five year average nationally; a symptom of the soft new listings flow, and the rapid rate of absorption due to above average levels of buying activity. More listings imply buyers will have more choice, which theoretically should help alleviate some of the urgency in the market.

With lockdown restrictions planned to ease further as vaccination targets are met, we should see an increase in confidence from vendors thinking of selling their property. At the moment, selling conditions remain skewed towards vendors rather than buyers, but a lift in listings through spring and summer should help to rebalance buyers and sellers’ places at the negotiating table. By how much will depend on stock levels as well as the depth of buyer demand amid worsening affordability challenges.