The problem with getting the diagnosis wrong is that you mistreat the symptoms. If you think you have a cold but really have a brain tumor then soldiering on with Codral is not a great idea.

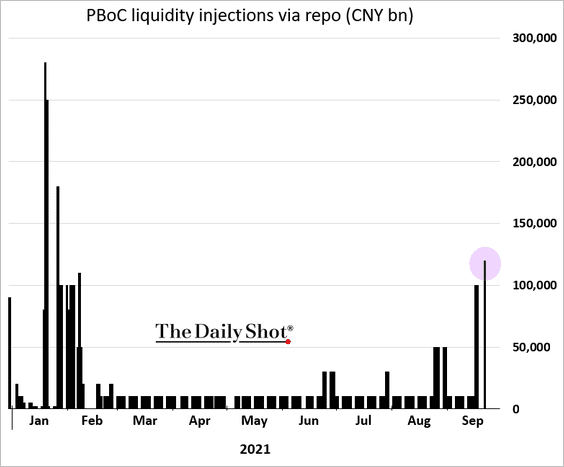

Evergrande yesterday released an unbelievably vague statement about reaching some deal with someone, somewhere. More importantly, the PBoC injected more liquidity:

If you thought that Evergrande was some kind of one-off “Lehman like” event then this would get you excited.

Advertisement