By Gareth Aird, CBA’s head of Australian economics

Key Points:

- Household deposits have risen by more than household credit over the pandemic due to the extraordinary size of government transfer payments.

- Fiscal stimulus due to the COVID shock has been indirectly funded by RBA bond buying (QE), which constitutes money creation.

- We expect the potent combination of QE and direct cash payments from government to households will boost future spending and lead to higher consumer inflation over the next few years.

- We reiterate our call that the RBA will commence normalising the cash rate in May 2023.

Overview

The inflation debate will heat up in 2022 as the Australian economy recovers and then moves into expansion mode. Most forecasters will base their inflation profile on the output gap and that will mean low core inflation will be the consensus call.

Indeed below target underlying inflation is the RBA’s central scenario until mid-2023.

But we believe the outlook for inflation should be considered in the context of the intersection of monetary and fiscal policy that has occurred over the pandemic. Put another way, an unprecedented fiscal expansion that has essentially been funded

via the printing press is anticipated by us to have an impact on future inflation.

This note takes a look at a unique dynamic over the pandemic whereby household deposits have risen faster than credit due to government transfer payments. A discussion is then presented on why the RBA’s bond buying program, which has essentially funded the fiscal support payments, has boosted the money supply. And finally we argue why the fiscal expansion and increase in broad money will ultimately take core inflation back to within the RBA’s target band earlier than the

central bank expects.

Household deposits have risen faster than liabilities

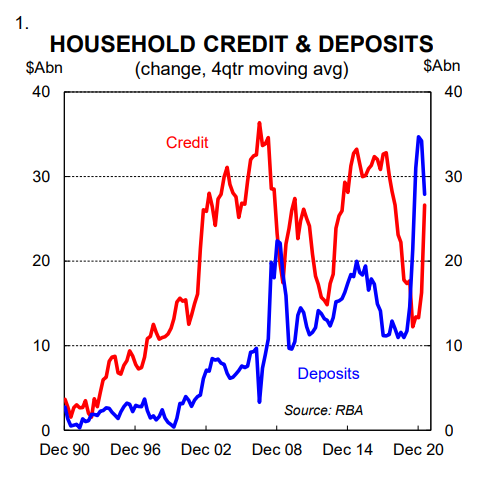

Household deposits have risen at a phenomenal rate over the COVID period. That in and of itself is not remarkable. There have been times previously when household deposits have risen quickly, most notably when household credit growth has been

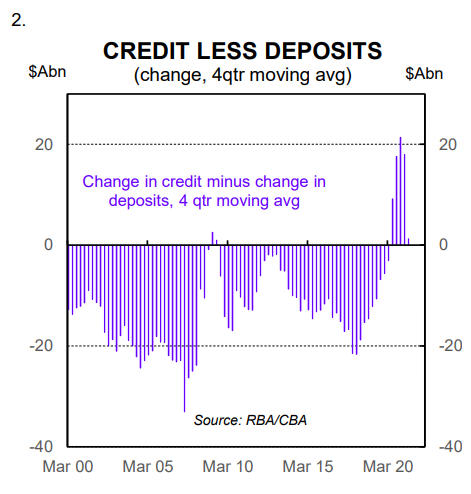

strong (loans create deposits). But what is different this time around is that the increase in deposits has significantly exceeded the lift in credit (charts 1 and 2).

In ‘normal’ times household credit rises faster in absolute terms than deposits because loans are only partially funded by deposits. But a very unusual situation occurred in 2020 whereby deposits ballooned relative to credit. The early withdrawal of superannuation played a role. But it only partially explains the story. The main driver of the increase in deposits relative to credit was fiscal transfer payments to households.

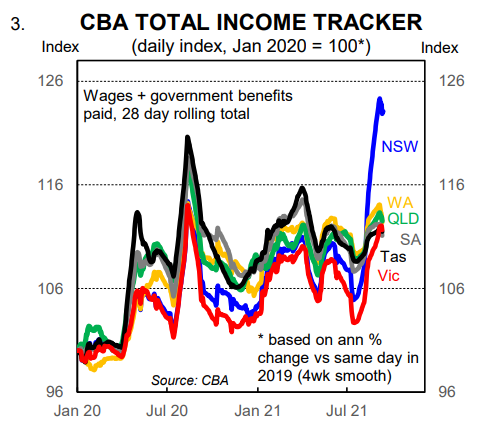

Our internal data indicates a similar story is unfolding right now because of the “COVID-19 disaster payments” in lockdown states which has seen income surge (chart 3). Note that the official data on income and deposits is only available to

Q2 21, but that our internally generated CBA data is up to 18 September.

The injection of public money into the household sector to support the economy through the pandemic has boosted household deposits without matching liabilities. Households do not have to repay this money in the same way they have to repay a loan. So the lift in deposits is potent in the context of thinking about future spending. Of course households might have to repay the money indirectly through higher taxes at a later date. But that need not necessarily be the case. In any event, it doesn’t alter the current mix of deposits and credit.

Savings have risen faster than deposits

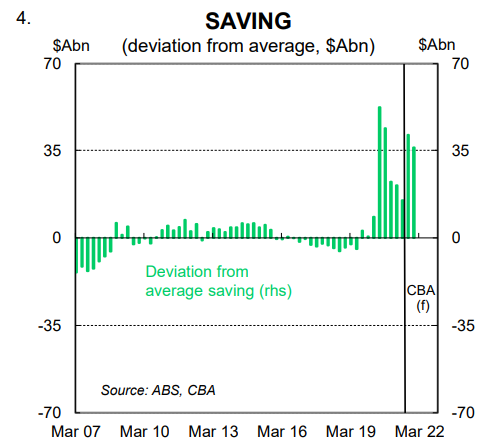

We estimate that over the pandemic to Q2 21 household deposits have risen by ~$A70bn more than they would have otherwise (3.5% of GDP). That figure is expected to swell to $A120bn by the end of 2021 (6% of GDP). Regular readers may note that these figures are lower than our estimates of accumulated savings over COVID ($A155bn to Q2 21 and $A230bn to end 2021; chart 4). This apparent discrepancy is reconciled by the difference between how household savings are calculated as opposed to changes in deposits.

Savings are the residual between income and expenditure. A large chunk of the additional savings that households accrued over the pandemic have been used to accelerate debt repayment. Those savings therefore do not show up as an increase in deposits. Rather they constitute a fall in credit, which is either housing related or personal (e.g. credit cards). In short, repaying debt ‘kills’ deposits.

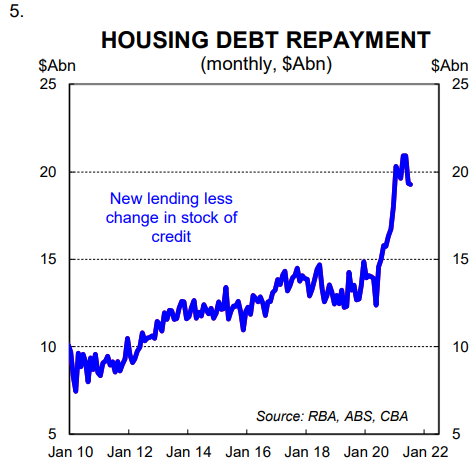

On our calculations housing debt repayments have stepped up by an average of $A4bn per month over the pandemic (chart 5). If current trends continue over the remainder of the year, households that carry debt will have as a collective paid off

$A75bn more than they would have otherwise since Q2 20. Of course households have taken on housing-related debt over the same period given the lift in new home lending. But here we are looking at what has happened to the existing stock of debt (i.e. debt repayment is defined as the flow of monthly new lending minus the change in the stock).

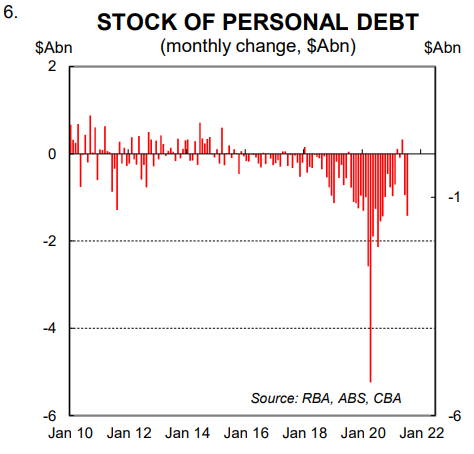

Personal debt repayment has also been impacted by the pandemic. More specifically, the contraction in the stock of personal debt underway pre-COVID has accelerated, particularly from March to September 2020. Personal debt fell by ~$A10bn more over that period relative to its pre-COVID trend (chart 6). Given that time period coincided with the early withdrawal of superannuation it is likely that many households used the opportunity to withdraw some or all of their superannuation to pay off personal debt.

We believe our forecast $A230bn in accumulated savings over the pandemic to end-2021 is the better figure to use when thinking about the economic outlook rather than the change in deposits. Why? Because people who have sped up debt repayment over COVID are more likely to consume a higher proportion of their future income. Put another way, households that have strengthened their balance sheet over the pandemic by accelerating debt repayment will feel more confident to spend in the future as they will carry less debt.

If households spend ~15% of the accumulated savings over the COVID period domestically in 2022 we will see a direct boost in consumer spending of $A35bn (equivalent to 1¾% of GDP). The risk lies with a larger number.

The printing press is funding the fiscal expansion

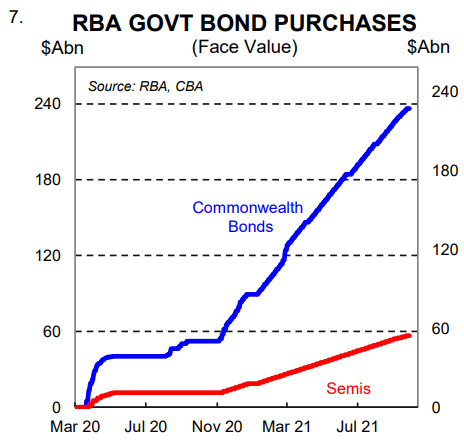

The extraordinary injection of cash into the household sector from government, which has contributed to the significant build up in savings, has been funded by public debt issuance (both Commonwealth and state). And the biggest buyer of government debt by far over the pandemic has been the RBA.

Indeed the RBA has so far bought $A236bn in Australian Government bonds since March 2020, which in net terms is not a whole lot less than the Australian Office of Financial Management (AOFM) has issued (chart 7).

The RBA’s huge bond buying program, which has largely financed the fiscal expansion, has in many respects blurred the distinction between fiscal and monetary policy. Yes, in a mechanical and operational sense the two arms of policy remain independent. But conceptually the RBA prints money, which through an intermediary ends up in the government’s hand. The fiscal authorities have then distributed money to households to support the economy which has boosted income, deposits and savings.

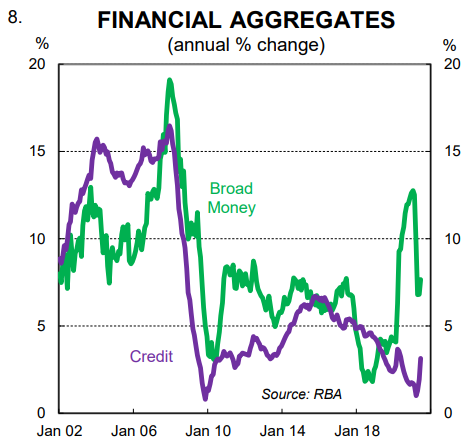

The big fiscal and monetary expansion has resulted in the money supply growing a lot faster than the stock of credit (chart 8). Proponents of monetary financing or MMT (Modern Monetary Theory) will see striking similarities between what they

advocate and what is happening. To be clear, the RBA can sell the bonds they have bought at any time in the future, which would shrink the money supply.

But if one takes a step back to look at what has occurred over the pandemic conceptually it reveals that we have entered unchartered territory in Australia. Transfer payments from the government have been indirectly funded by the central bank through money creation.

“There is no free lunch”

The RBA Governor in his speech of 21 July 2020 spoke in detail about money creation to finance the government. In many respects parts of the speech were a head-scratcher with respect to the RBA’s outlook for below target inflation.

The Governor stated that,

“one idea for the use of the central bank’s balance sheet that I sometimes hear – [is that], we should use it to create money to finance the government. A variant on this idea is that the central bank should just deposit money in every bank account in the country – this is sometimes known as ‘helicopter money’ because, before we had an electronic payments system the idea was that banknotes could simply be dropped by helicopter.

For some, this idea is seen as a way of avoiding financing constraints – it is seen as holding out the offer of a free lunch of sorts. The central bank, unlike any other institution, is able to create money and the resource cost of creating that money is negligible. So the argument goes, if the government needs money to stimulate the economy, the central bank should simply create it in the public interest.

The reality, though, is there is no free lunch. The tab always has to be paid and it is paid out of taxes and government revenues in one form or another. I would like to explain why.”

He then went on to say,

“suppose that the additional government spending is successful in stimulating the economy and this starts to push inflation up. At some point, interest rates would need to be increased to avoid inflation rising too far. If this lift in interest rates did not occur, inflation would rise, perhaps to a very high level. In this case, it would be through the inflation tax that the community pays for the extra government spending. So there is no free lunch – the spending is just paid for in a different way”

We by and large agree with Governor Lowe here. And yet the RBA does not think that what is occurring with respect to QE and huge fiscal deficits to fund transfer payments is analogous to the situation the Governor described above. In our view it is very much similar to the extent that money creation is financing fiscal spending. And we believe there will be a lift in inflation as a result.

Underlying inflation within target by mid-2023

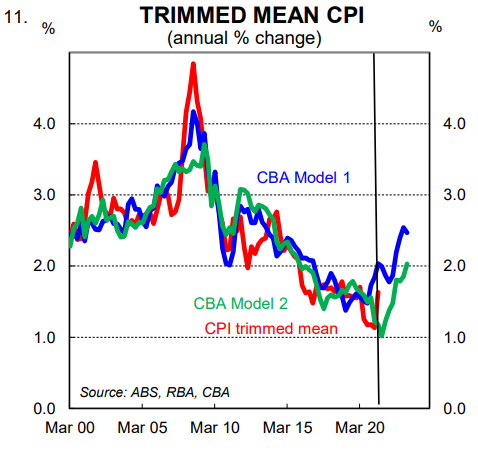

We run several models to produce our forecast profile for core inflation. It is generally the case that relying on one model is not sufficient as there are many forces that influence inflation and judgement must be made as to which factors may be more dominant at any given time.

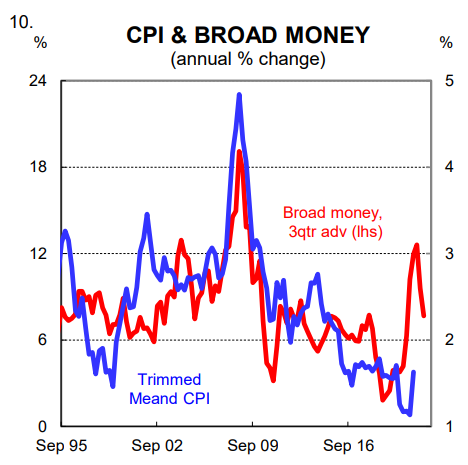

Given the unique nature of the expansion in money supply via QE that has funded government transfer payments we are placing more weight on modelled inflation that includes changes in broad money as an input (charts 10 and 11; note model 1 includes broad money as an input as well as underutilisation, inflation expectations and import prices. Model 2 for comparative purposes assumes there is no impact of money supply on inflation).

Our assessment is that the lift in money supply this time around is more important to the inflation outlook because: (i) it has not been accompanied by a commensurate lift in credit as has previously been the case (a lift in credit is a constraint on future consumption and inflation); and (ii) the increase in money supply has found its way into household bank accounts via transfer payments.

We forecast underlying inflation to be around the midpoint of the RBA’s target band at mid-2023 (i.e. 2½%). In contrast the RBA expects underlying inflation to be 2.0% at mid-2023.

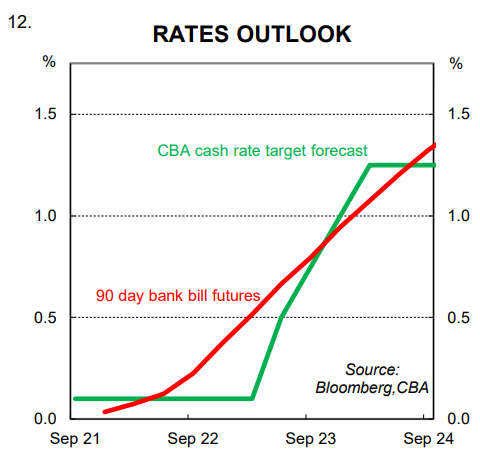

Given the inflation outlook we have described, we retain our call for the RBA to commence normalising the cash rate from May 2023 (ie. well before the 2024 start date the RBA is signalling), whilst acknowledging the risks are skewed towards a later date for lift off (chart 12).