Courtesy of the always excellent BankingDay:

Oceans of liquidity in the banking system are transforming the operational and financial markets sides – but not the policy sides – surrounding the conduct of monetary policy in Australia. At least until the next crisis.

Late last week, the RBA informed banks and other participants in the Reserve Bank Information and Transfer System (RITS) of a decision that jettisons 35 years of daily money market practice.

“Starting 6 October 2021, the Reserve Bank will conduct open market operations weekly, on Wednesdays, instead of daily,” the RBA advised all RITS users.

The Reserve Bank said it “may, if required and at its absolute discretion, announce additional open market operations on other business days”.

David Lynch, CEO of the Australian Financial Markets told Banking Day “the RBA’s announcement has not been raised with AFMA by members.

“The volume of OMO has fallen and so the change is regarded as an operational measure to reflect this situation.”

Across the Covid-19 pandemic, the apparatus of monetary policy in Australia has undergone, in stages, material innovation, headlined by QE-style bond-buying and the (now discontinued for new funding) A$188 billion Term Funding Facility, which put a floor under industry funding costs.

“There was just an overabundance of liquidity anyway,” Shayne Elliott, ANZ’s CEO, told the House Economics Committee last Thursday, when challenged on its late rush to draw its full TFF allowance.

“You had extraordinary levels of deposits, both from small businesses and from mums and dads.”

In his new textbook, Banking & Financial Institution Management in Australia, emeritus professor Kevin Davis writes that repos “are the major tool used by the RBA in managing system liquidity”.

RBA open market operations, Davis explains, “are primarily via repo transactions, with the RBA buying securities in exchange for providing cash”, and thus refers them as ‘reverse-repos’.

In the RBA Bulletin in June, Sean Dowling and Sebastien Printant from the from Domestic Markets Department supplied a lengthy (if now dated) analysis of ‘Monetary Policy, Liquidity, and the Central Bank Balance Sheet’.

Since the introduction of the Reserve Bank’s policy measures in early March 2020, the balance sheet has more than tripled in size from around $170 billion to around $590 billion.

“In contrast to the decade prior to the pandemic, the Reserve Bank’s policy measures have directly influenced the size of its balance sheet,” the authors explain.

“Accordingly, the size and composition of the balance sheet can reveal how these policy measures have been used, and provide insights into the Reserve Bank’s policy stance.

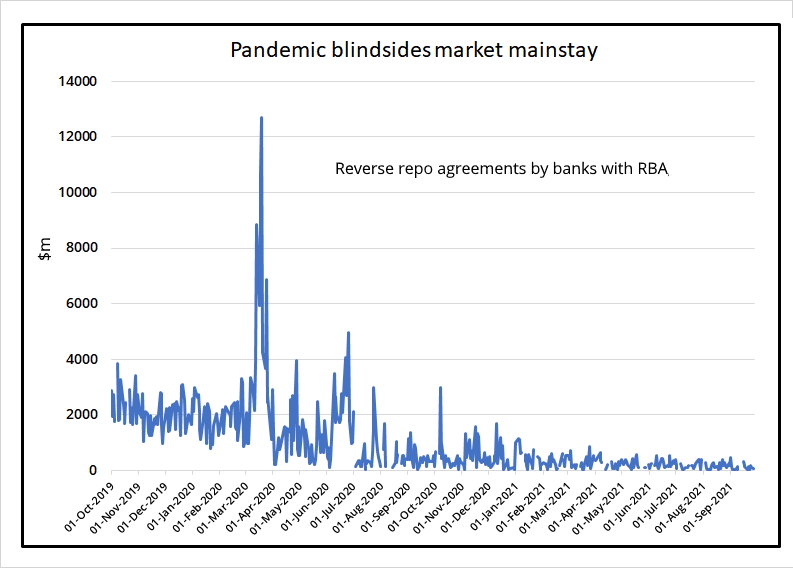

“Reflecting the initial policy response to the pandemic, the Reserve Bank’s balance sheet grew by around $90 billion between early March and early April 2020. The stock of outstanding OMO repos (also known as the OMO repo book) doubled in size to $100 billion, and accounted for as much as 37 per cent of the Reserve Bank’s assets in June 2020 (compared to around 25 per cent before the pandemic).

“More recently, the OMO repo book has fallen to around $10 billion,” they wrote, the number accurate in mid-June 2021.

In the four months since then the OMO repo book more or less halved again, to around $6 billion a couple of days ago.

The values dealt in Open market operations daily so far over September were less than A$100 million, on average; this mainstay of the short-term rates market overwhelmed, like so much else, by Covid.