Below is an article written by me published this week at News.com.au:

The usually buoyant Aussie property market is facing its biggest test yet. Can the house price boom survive another lockdown?

With more than half the nation likely to remain in lockdown for the foreseeable future, there is a big question mark over whether Australia’s record-breaking property price boom can be sustained.

A fortnight ago, I argued that Australia’s property boom would “fizzle” based on four observations:

1. Falling auction clearance rates;

2. Falling new mortgage demand;

3. A sharp increase in dwelling construction amid the lowest rate of population growth in a century; and

4. Declining affordability.

Based on the above factors, my base case was “for Australian property price growth to decelerate over the remainder of 2021 and then slow more sharply in 2022 once regulatory mortgage curbs are introduced, with the next property downturn to arrive in late 2022 or early 2023”.

Now there is an alternative scenario to consider in which the Australian economy drops into recession followed by a troubled recovery in 2022 amid a disintegrating national Covid strategy and crashing commodity prices.

In this scenario, the Reserve Bank of Australia (RBA) will further lower mortgage rates in a bid to support a flagging economy and could perversely add fuel to the Australian property market, extending the price boom.

Even lower mortgage rates?

The biggest driver of Australia’s property market is undoubtedly mortgage rates.

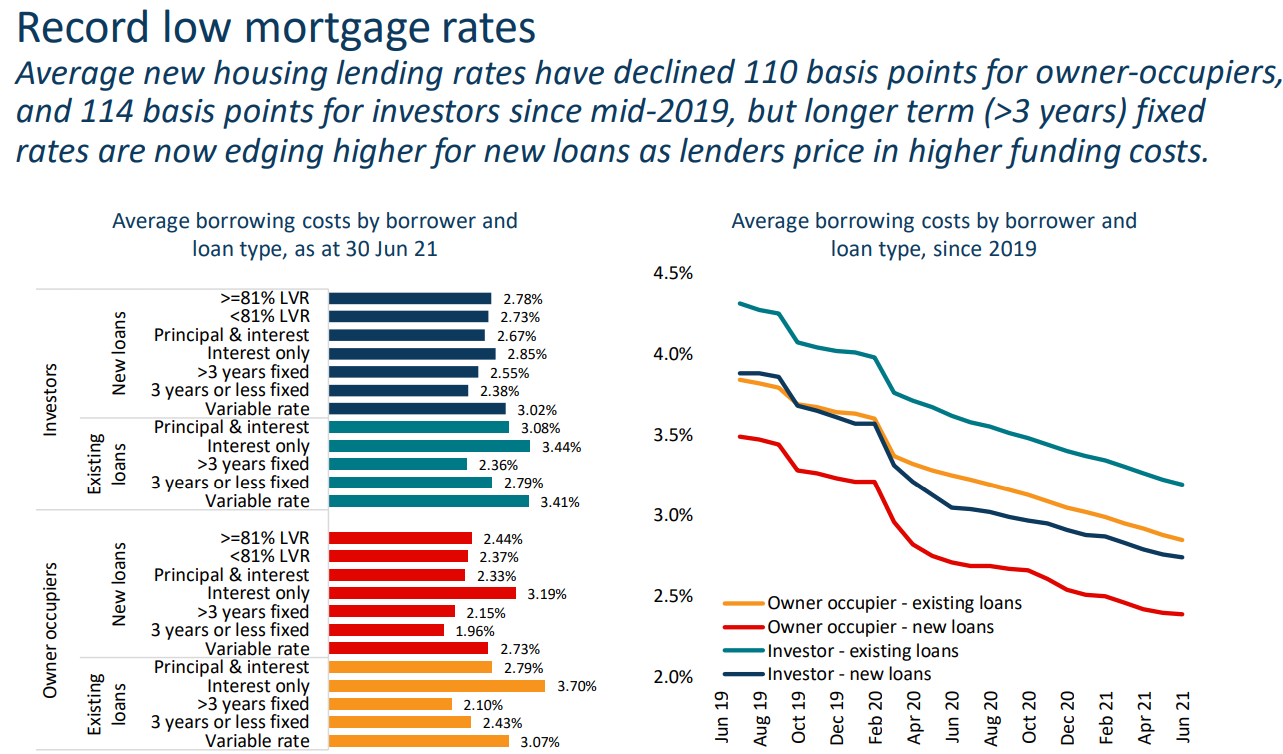

As illustrated in the next chart from CoreLogic, Australian mortgage rates have fallen heavily since the coronavirus pandemic began.

Mortgage rates have been driven to record lows courtesy of cuts to the official cash rate to only 0.1 per cent, alongside the introduction of the RBA’s Term Funding Facility (TFF).

The TFF provided low cost three-year funding for authorised deposit-taking institutions (ADIs) to support the supply of credit. And it has been highly successful in replacing relatively expensive wholesale funding with cheaper funding from the RBA.

As a result of the RBA’s actions, new variable rate mortgages can now be obtained at interest rates of just 2.7 per cent for owner occupiers and 3.0 per cent for investors.

New fixed mortgage rate loans are even cheaper, available for owner-occupiers at rates of between 2.0 per cent to 2.4 per cent versus around 2.7 per cent for investors.

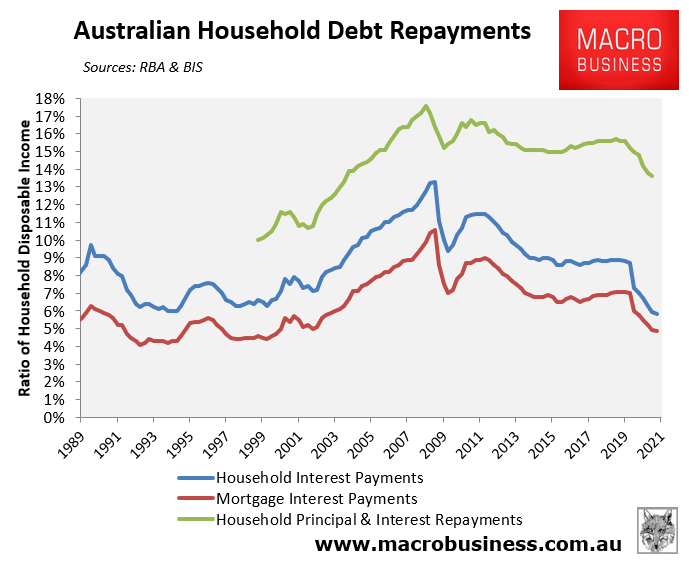

Existing mortgage rates have also fallen considerably, driving mortgage interest payments as a share of household disposable income to a 21-year low, whereas household principal and debt repayments as a share of disposable income have fallen to a 17-year low.

Double-dip recession

However, the prospect of lockdowns continuing for months on end and the economy entering a ‘double-dip recession’ will see the RBA respond with further monetary stimulus that would drive mortgage rates even lower and add fuel to property prices.

First, the RBA could reinstate the TFF program, print more money, and effectively pay banks to lend by offering a negative interest rate (e.g. -0.01 per cent). Alternatively, the RBA could cut its cash rate into negative.

Either measure would have the effect of driving Australian mortgage rates to fresh lows, again especially fixed rate loans, in turn stimulating further price growth.

Over the past few years, financial markets have become accustomed to regular stimulus to the point where ‘bad news’ is now perceived as ‘good news’ as asset prices rise.

The same dynamic is developing in Australian property.