Nordea with the note:

We generally had the feeling that the Jay-Man was a dead man walking within the Fed as Lael Brainard’s style and opinions suited the Biden administration much better than Powells, but suddenly it seems less clear that Brainard will take over the reins next year as Janet Yellen allegedly backs Powell. We always thought that the reason why Brainard was not offered the US Treasury Secretary role was, that she was the preferred Fed chair candidate, but it could in turn be that Biden picking a boomer in the US Treasury (Yellen) leads to Biden picking another boomer in the Fed chair role (Powell). Boomers pick boomers! Powell is relative to Brainard a much more hawkish choice, and it will likely postpone the otherwise almost inevitable entry of wokeism in the FOMC decision making by another couple of years.

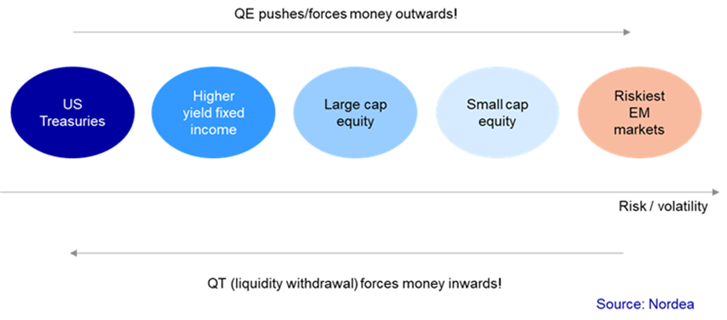

If Powell stays in the chair-role (our base case), then it increases our conviction in a hawkish shift from the Fed during the autumn due to lagged positive effects in the labor market from the stimulus seen in 2020/2021. It also risks creating a continued QT-like environment with underperformance of the riskiest assets as we have seen recently. And no, markets are not selling off due to Delta. The reason is that the Fed is about to tighten policy when the Credit impulse is already negative.