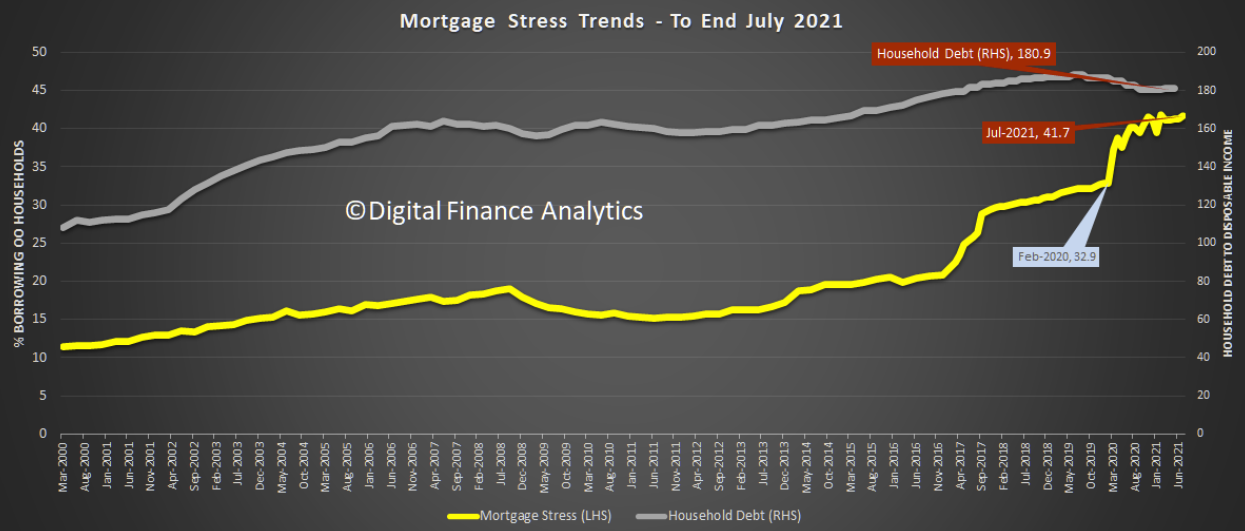

Digital Financial Analytics (DFA) has released its July mortgage stress data, which shows stress levels rising on the back of Sydney’s hard lockdown:

There is a significant correlation between mortgage stress hot spots and COVID hot spots…

Fairfield and South Western Sydney are the epicentre of COIVD, and mortgage stress. The reason is simple, more households there are in insecure work, often in multiple jobs with little fall-back, and massive spending pressures.

Analysis in other post codes across the country reveals the same findings.

More generally, mortgage stress rose across the country in July, thanks to the lock-downs, and also more mortgages being written at high LVR and DTI ratios. Overall mortgage stress rose to 41.7%, while household debt ratios also rose…

There was significant spike in NSW – at 40.15%, compared with 38.62% a month earlier.

The monthly increase in mortgage stress across Sydney makes sense, given its long hard lockdown. It is also confirmed by the latest mortgage deferral data from the Australian Bankers Association:

Since 8 July 2021, more than 14,500 home loans have been deferred…

NSW home loan deferrals account for more than two thirds of total deferrals, while almost 80 per cent of deferred business loans are also from NSW…

Almost 24,000 people since early July have accessed a range of support measures offered by their bank and 64% of these have opted to defer their loan repayments for up to 3 months.

Advertisement

That said, the dramatic rise in mortgage stress since February 2020, from 32.9% to 41.7% nationally, doesn’t make sense.

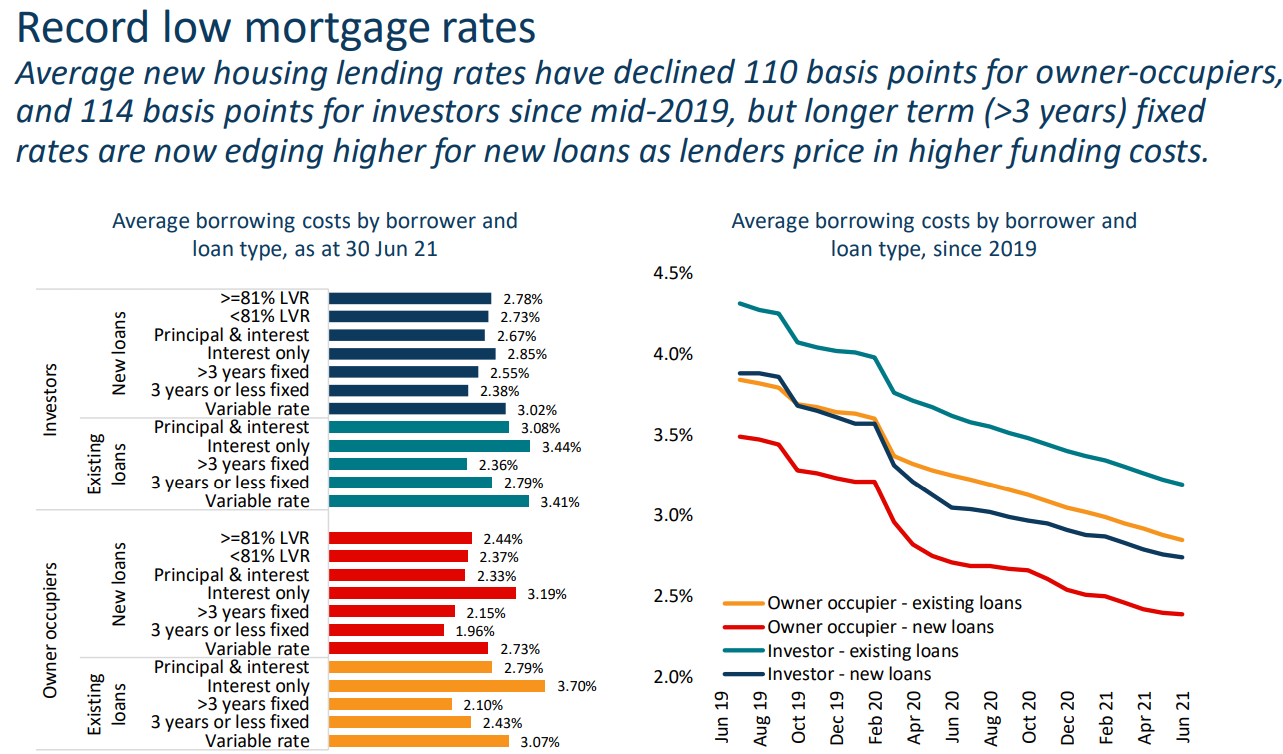

First, mortgage rates have collapsed, which should have lowered mortgage stress (other things equal):

Huge fall in mortgage rates.

Advertisement

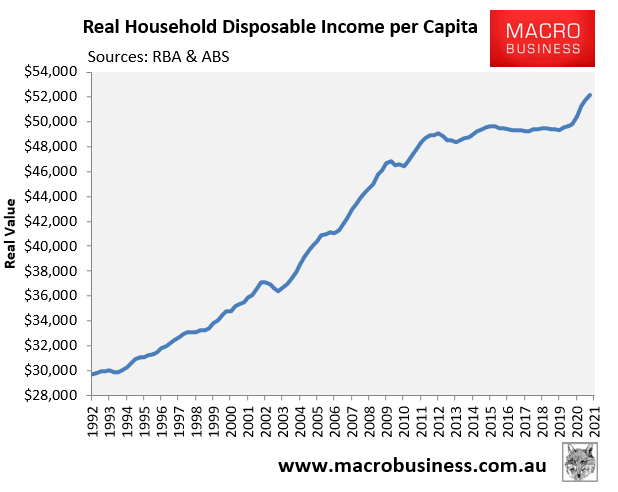

Second, household disposable income experienced its biggest annual rise since 2008 on the back of stimulus:

Real per capita household disposable income has broken a decade of stagnation.

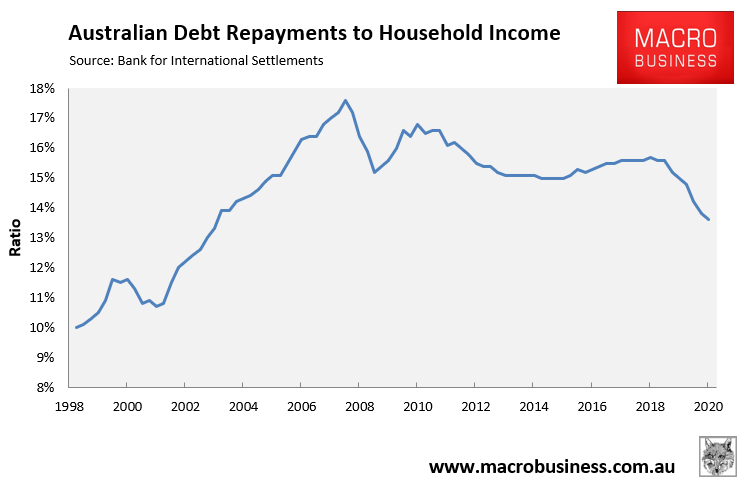

These factors have combined to drive the ratio of debt repayments – both principal and interest – to household disposable income to a 17 year low, according to the Bank for International Settlements:

Advertisement

Australian household debt repayments have fallen to a 17 year low compared to disposable income.

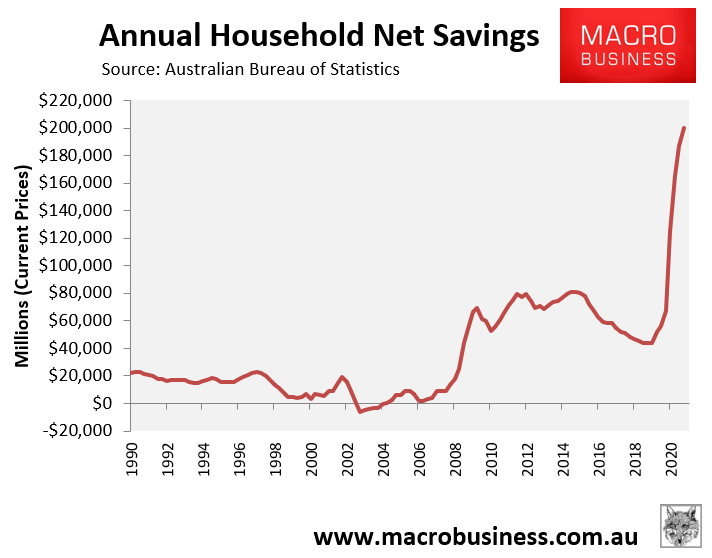

Meanwhile, Australian households have built up a massive war chest of savings, which suggests they are on aggregate households are in a strong financial position:

Australian households saved a record $200 billion in the year to March 2021.

Advertisement

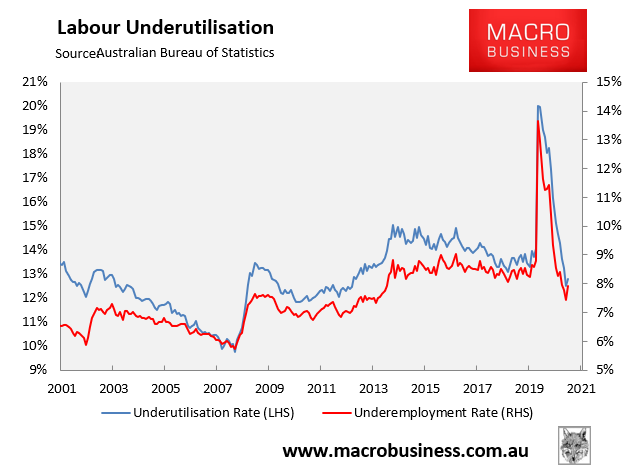

Finally, unemployment and underemployment have fallen well below their pre-COVID level:

Below pre-COVID levels.

So while recent lockdowns have thrown a spanner in the works, over the 18 months since the pandemic hit mortgage stress levels should have fallen, not risen.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.