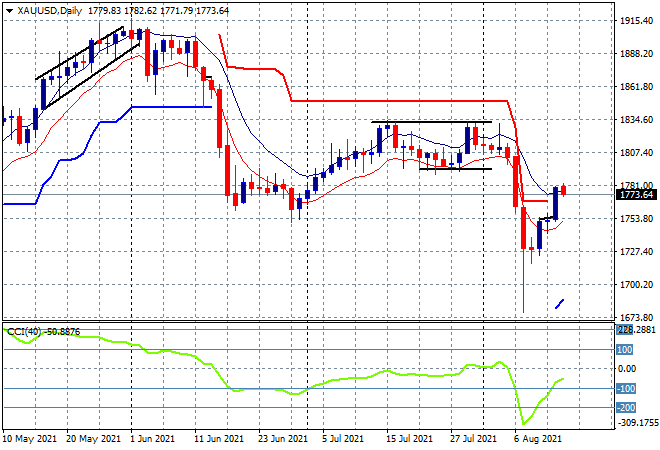

It’s a sea of red across Asian stock markets as we start a new trading week, following Friday night’s meek moves on the latest US consumer sentiment survey and of course, the Taliban taking over “Afghanistan” (which is likely not to exist as a nation from here on in). This has seen increased volatility across commodity markets with oil prices slumping, while the USD remains weak against most of the currency majors. Gold has pulled back slightly from its surge on Friday night, currently at the $1773USD per ounce level but looking tenuous:

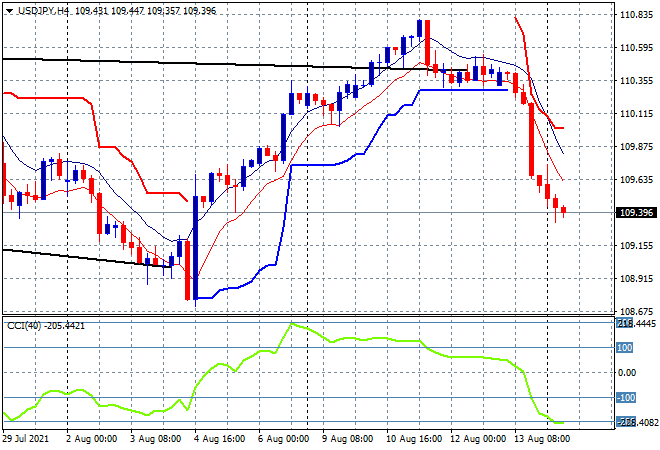

The Shanghai Composite is again unable to gain traction, drifting 0.1% lower at 3512 points while the Hang Seng Index is still in reverse gear and down over 1% at 26113 points. Japanese stocks didn’t like the surprise uplift in GDP figures today, held back by a much stronger Yen as the Nikkei 225 slumps more than 1.6% to 27523 points. The USDJPY pair is about to put in a two week low, still falling after the major retracement on Friday night and barreling in on the 109 handle presently:

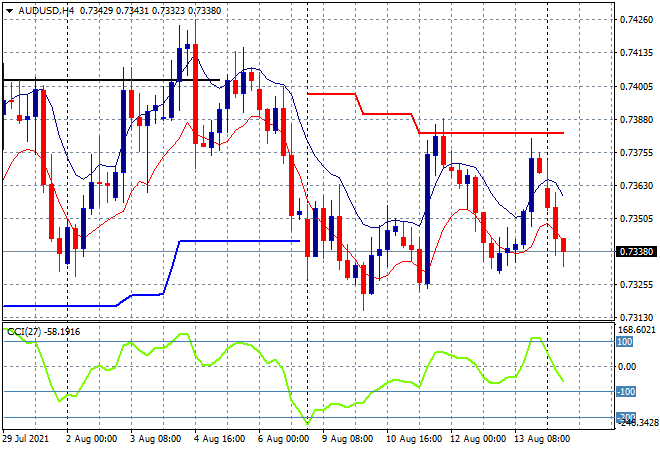

Australian stocks are selling off but not too sharply, with the ASX200 taking back the Friday gains to be down more than 0.6% and back below the 7600 point level as the Australian dollar flounders away still despite all the other strong undollars, almost back to the previous weekly low at the 73.40 level:

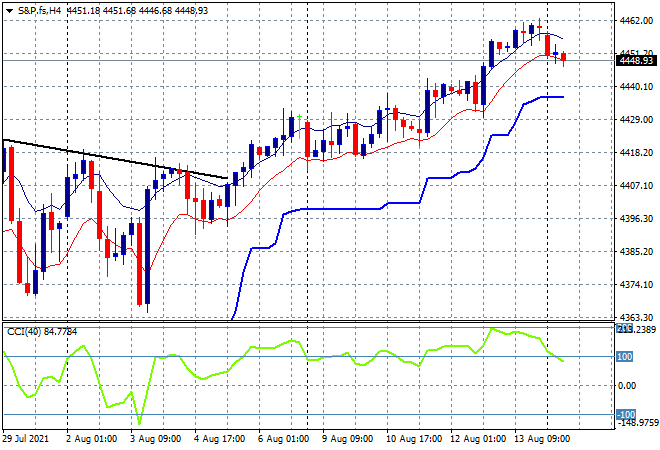

Eurostoxx and S&P futures are slowly fading away going into the London open, with the four hourly chart of the S&P500 showing price retracing from the record highs on Friday night, with momentum now reverting from the extreme overbought stage:

The economic calendar starts the week with a nearly clean slate with more Treasury bond auctions overnight and not much else.