By Daan Smit

Inflationary pressures in the United States and other corners of the world have been accelerating this year as a result of supply bottlenecks, cash-flooded economic systems, and suppliers’ struggles to push their output volumes near where they were before the pandemic to catch up with pent-up demand.

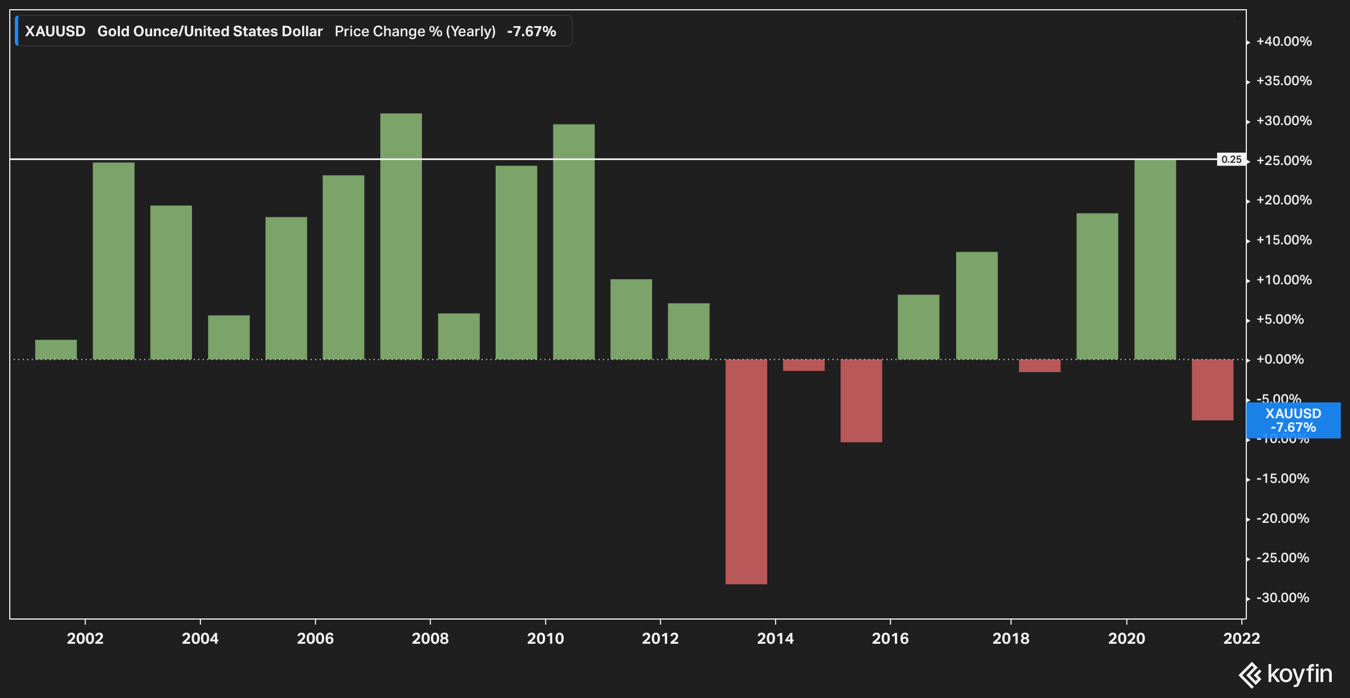

However, somehow counterintuitively, the price of gold – a traditional hedge against inflation – is down almost 8% since 2021 started.

As a result, the question in the mind of many investors who may not be familiarized with how to trade commodities is probably why the price of gold is not exploding higher in the midst of the highest inflation readings in more than a decade?

In the following article, I’ll share a few factors that may be keeping a lid on the price of the precious metal.

Supply & Demand factors

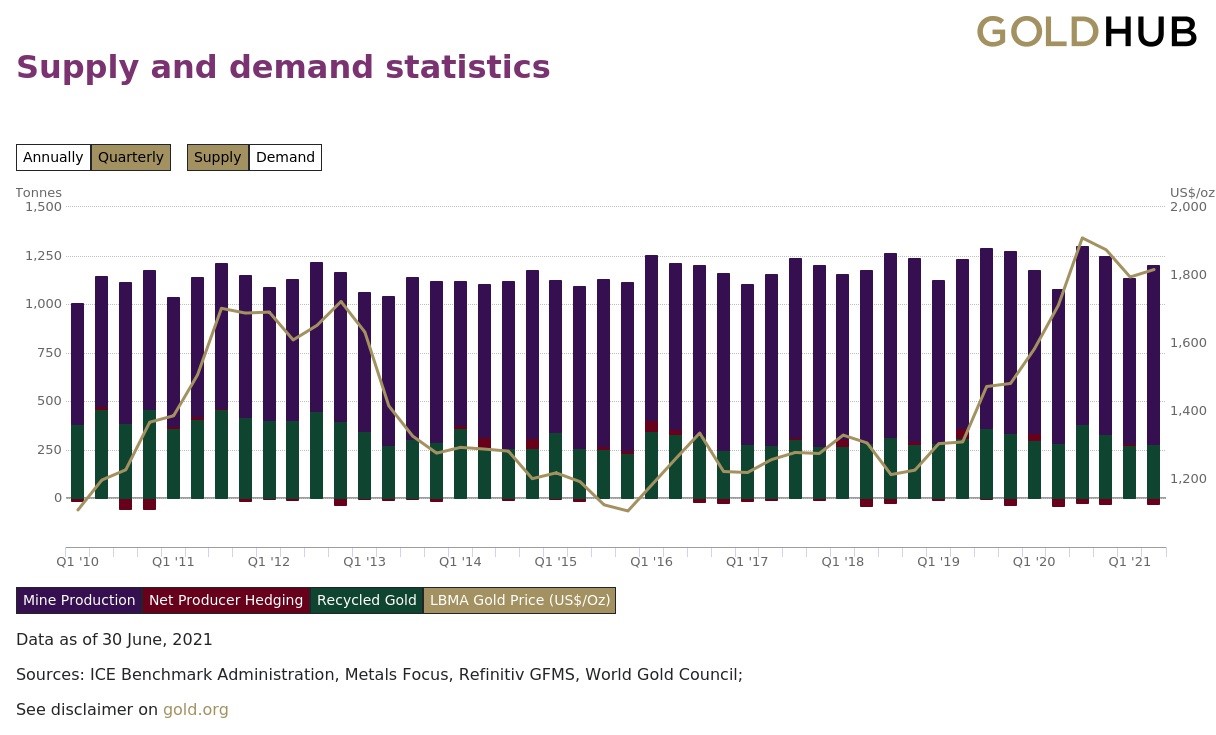

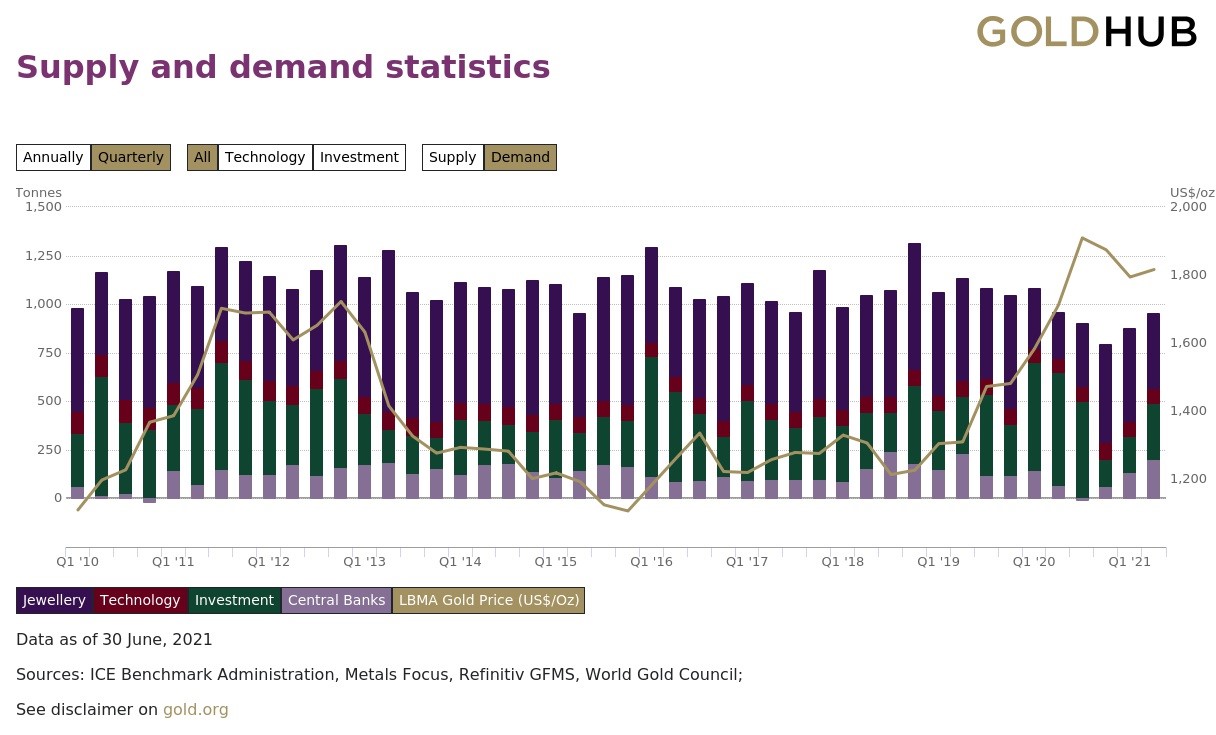

Gold prices are primarily influenced by supply and demand dynamics and to get some more insights about the evolution of these two factors in the past quarters we can rely on the data provided by the World Gold Council (WGC).

First, if we look at the supply chart, it seems that supply levels have already recovered near where they were before the pandemic started, with a total of 924 tones of the precious metal being mined during the second quarter of 2021.

Interestingly, it seems that the price of gold peaked during the third quarter of 2020, exactly at a point when mine production volumes reached their third highest reading in more than 11 years.

Meanwhile, the demand chart shows that buying volumes for the precious metal dropped precipitously during the third and fourth quarter of 2020 as demand from central banks collapsed to its lowest levels since 2010 while demand from the investment segment also dropped significantly.

Upon taking a look at the relationship between supply and demand, the first explanation for gold prices remaining fairly stalled is that demand for the precious metal has dried up and that could be explained by increased interest in other vehicles as potential hedges against inflation as is the case of cryptocurrencies.

Cryptocurrencies taking the lead as the top inflation hedge

When the demand from the investment segment declined the most for gold, during Q4 2020 and Q1 2021, the price of Bitcoin advanced from $10,000 to nearly $60,000 per coin.

This negative correlation in the performance of the two assets seems to indicate that gold’s appeal as a protective measure against inflationary pressures is fading while cryptocurrencies are emerging as a potential substitute.

One variable that may explain the increased appeal of Bitcoin (BTC) specifically as a store of value is its limited lifetime supply. In this regard, the maximum supply of Bitcoin is 21 million coins while the supply for gold is not fixated and could, in certain scenarios, fluctuate to levels that may surpass its demand.

Instead, Bitcoin’s supply will remain unchanged and that increases its ability to act as a plausible store of value as long as its underlying technology is considered safe.

Could most of the upside for gold be priced in?

At $1,752 per troy ounce, gold is trading 32% below its August 2020 all-time high of $2,075 per ounce. Back then, the demand for the precious metal hit its lowest level in the past 10 years at least.

One plausible theory that explains why gold has started to decline even as inflation accelerated is that most of the upside resulting from higher demand for the precious metal was already priced in.

This theory seems entirely possible if one considers that gold appreciated as much as 25% in 2020, this being the third largest annual gain experienced by the precious metal in the past 20 years.

Moreover, the supply/demand imbalance highlighted previously may have not been anticipated by market participants and that explains the sharp drops that the price of gold experienced in August 2020, January 2021, and most recently in April 2021.

Summarizing the findings

Based on the evidence presented above, it seems that the counterintuitive performance of gold during the latest spike in inflation levels in the United States is not necessarily hard to explain as multiple factors have played a key role in depressing the price of the yellow metal including a supply/demand imbalance, a relatively higher appeal of cryptocurrencies as a safe-haven, and overly optimistic demand forecasts that didn’t materialize.

Meanwhile, with demand levels still at historically low levels, chances are that gold’s performance in the following quarters could remain opaque, even if inflation accelerates, as long as these variables remain unchanged.

Daan Smit is a Dutch-born writer who lives in Asia. Developing feature articles, global news & technology pieces. His work explores issues related to business psychology, data science, and cyber security.

Editorial Note: The opinions are the author’s and are not necessarily the opinions of MacroBusiness.