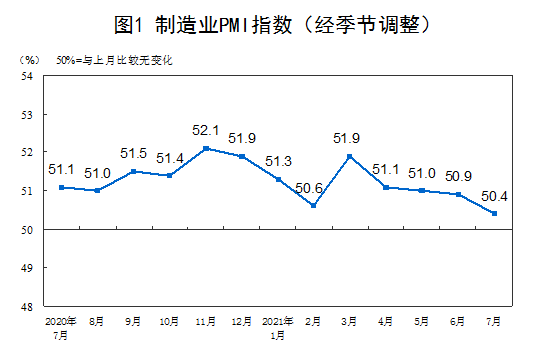

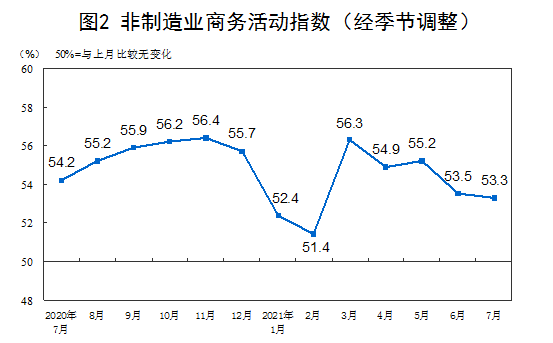

Over the weekend China released its latest round of official PMIs with manufacturing fading at 50.4 and services also slipping to 53.3:

New orders are also softening for both as well, and new export orders are falling away:

Advertisement

All pretty much as expected as credit tightens.