By Gareth Aird, head of Australian economics at CBA

Key Points

- We expect Q2 21 real GDP to increase by 0.3%.

- Household consumption, business investment and public spending will make contributions to growth.

- Net exports and inventories will be big drags on growth while dwelling investment should post a small fall.

- We expect nominal GDP to increase by a solid 2.1%.

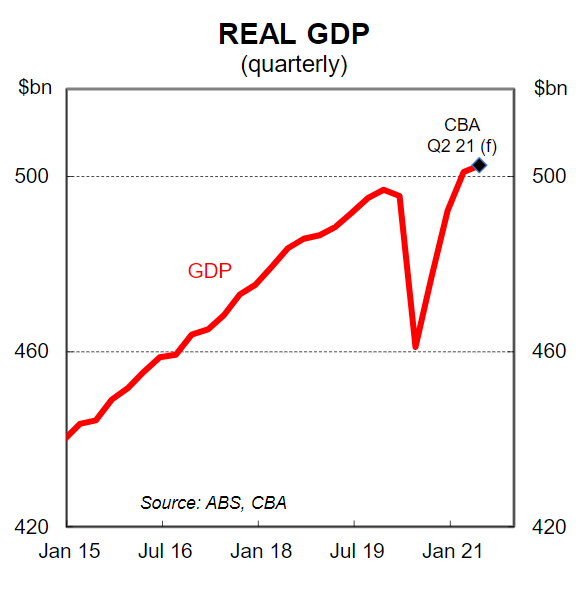

The Q2 21 national accounts, due for release on Wednesday, are expected to show that economic momentum slowed over the June quarter. Job creation was strong over the period but lockdowns around the country at various points will have hit production. Put simply there will be a disparity between strong employment growth in the June quarter and modest GDP growth – stay at home orders reconcile the difference.

The ABS has been churning out the partial data over the past two days and it’s been a mixed bag relative to our preliminary forecasts for each component of GDP. The expenditure side of GDP looks a touch weaker than we had pegged, largely because of a solid miss on inventories. But the income measures have come in a little stronger than anticipated. Indeed the different pieces of partial data are sending conflicting signals on what to expect for the GDP print on Wednesday – the income side looks a fair bit better than the expenditure measures. In some sense the data released over the past couple of days has left us none the wiser. Nonetheless we couldn’t resist the temptation to make a few more tweaks to our GDP call.

We now forecast real GDP to increase by 0.3% in Q2 21 (versus our preliminary estimate of +0.4%). The risks are tilted to a softer outcome.

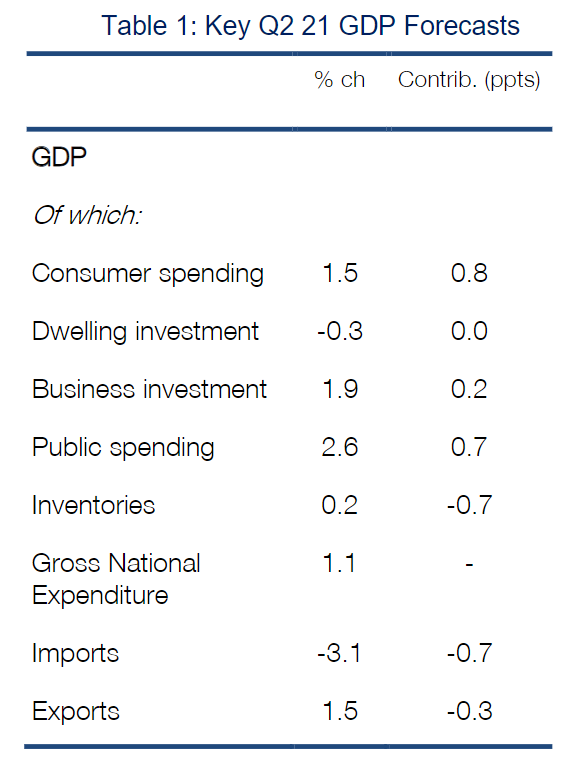

On the expenditure side we expect to see:

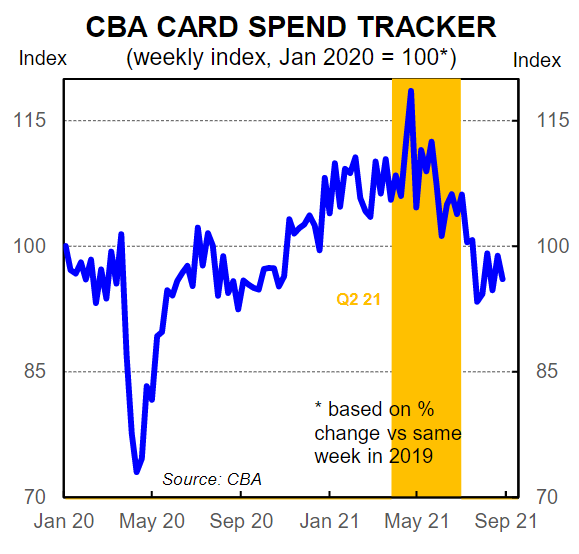

- another decent increase in household consumption: CBA(f) +1.5% (note that this is the key source of uncertainty and the risk lies with a weaker increase based on our internal data – see chart opposite);

- a very small decline in residential construction: CBA (f) ‑0.3%;

- a healthy lift in business investment driven by plant and equipment: CBA(f) +1.9%;

- a strong lift in public demand which comprises a massive lift in public investment and a decent increase in recurrent expenditure: CBA(f) +2.6%;

- a 0.2% increase in inventories which will subtract 0.7ppts from growth; and

- a solid 1.0ppt negative contribution to growth from net exports (export volumes down and imports up).

See Table 1 for our Q2 21 GDP call by component.

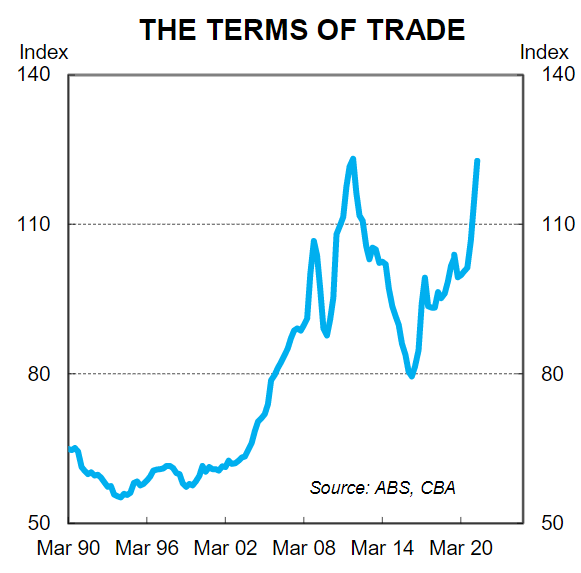

The whopping 7.0% increase in the terms of trade over Q2 21 will have a large positive impact on nominal GDP which will also reflect the modest rise in consumer prices (recall that the Q2 21 trimmed mean CPI was +0.5%/qtr).

We have the GDP deflator at 1.8% in Q2 21 which means we expect a quarterly increase in nominal GDP of 2.1%. The Government’s coffers will have received a welcome boost in the June quarter thanks to the solid expected lift in nominal GDP. But of course the Commonwealth Budget is currently being hit hard by extended lockdowns in NSW and Victoria.

The savings rate is expected to fall over Q2 21 but still remain well above pre‑COVID levels which means there will be a further accumulation in savings across the household sector (CBA (f) is for the savings rate to be 9.1% in Q2 21 – down from 11.6% in Q1 21).

GDP is backward looking and the economic outlook has changed radically because of the delta variant. As such, financial markets will largely discount the data tomorrow. Policymakers, however, will be desperate to avoid a negative GDP print because it would rubber stamp that the Australian economy is in recession. The difference, however, between a small positive or small negative growth rate for GDP in Q2 21 is simply optics. For all intents and purposes the Australian economy is currently in a manufactured recession as we go through another huge negative shock. The Government, RBA and most in the media have reframed from using the ‘R‑word’ to date to describe what is currently happening in the economy. That will be inescapable tomorrow if the ABS throws up a negative number.