Below is an article written by me published yesterday at News.com.au:

There are two strong indicators used to predict house price growth – and both of them are showing a downward trajectory right now.

This week, CoreLogic recorded another strong 1.6 per cent rise in Australian property prices in July, with values up a remarkable 14.1 per cent over the first seven months of 2021 and 16.1 per cent over the past year.

This marked the strongest annual price growth recorded by CoreLogic in 17 years. It is also one of the broadest property booms on record with every capital city and state region recording annual growth.

There are several factors behind the strong price growth. Record low mortgage rates and an acute shortage of homes for sale has created ‘FOMO’ [fear of missing out] in the market. Household finances are in rude shape after they banked $200 billion worth of coronavirus stimulus. Finally, jobs are plentiful with the number of job vacancies per unemployed and underemployed Australian tracking at a record low.

However, while property price growth remains strong, the market is beginning to lose steam.

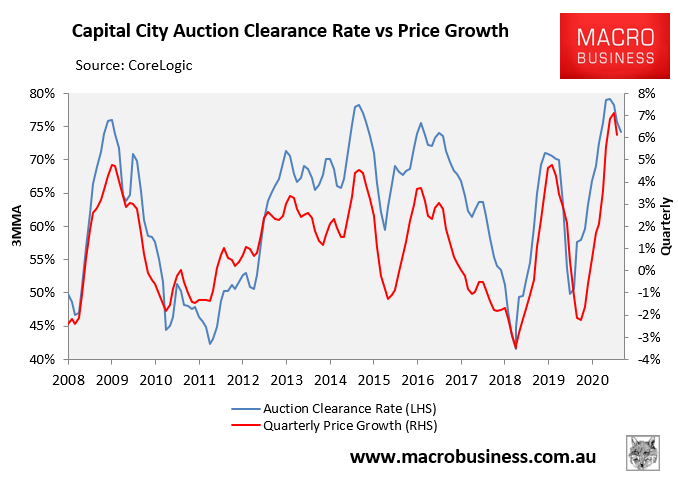

The best short-term leading indicator of price growth is the national auction clearance rate, which has fallen sharply from its March peak; albeit remains elevated from a historical perspective.

Auction clearance rate is a good short-term indicator of the market.

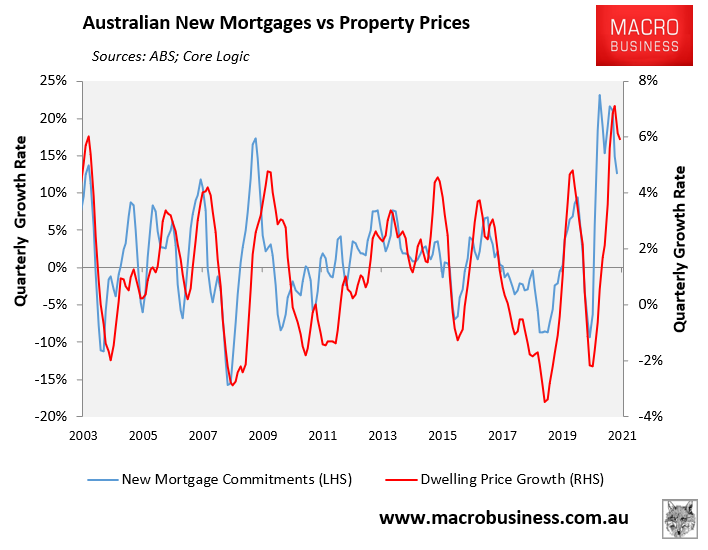

The second best leading indicator for property prices is the growth in new mortgage commitments, which have also turned down:

There’s been a recent drop in new mortgage commitments.

Later this year, the Australian Prudential Regulatory Authority (APRA) is likely to impose ‘macro-prudential’ curbs on mortgages to cool the market, such as loan-to-value ratio (LVR) restrictions, debt-to-income (DTI) restrictions, increased mortgage buffers, or restrictions on interest-only lending.

These types of restrictions were imposed by APRA in December 2014 and March 2017 and quickly reduced credit growth in the targeted mortgage products.

While it is highly unlikely that the official cash rate will rise over the next 12 months, fixed mortgage rates should also rise moderately owing to the closure of the Reserve Bank’s Term Funding Facility (TFF), which was shut to new drawdowns on June 30, 2021.

The TFF provided low cost three-year funding for banks to support the supply of credit. It was highly successful in replacing more expensive wholesale funding and driving fixed mortgage rates lower.

So, with the TFF now closed, average mortgage rates should rise from their record lows, dampening mortgage and property price growth into 2022.

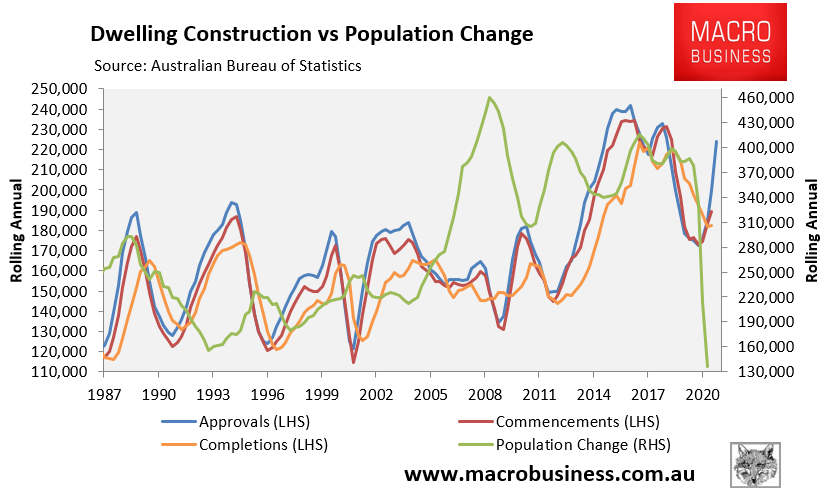

Another longer-term headwind for the Australian property market is the rising supply of homes under construction amid plunging population growth.

The federal government’s Homebuilder stimulus package has driven a huge lift in homes under construction, most of which will hit the market next year. This comes at a time when immigration into Australia is running at century lows, meaning the structural supply of homes will increase sharply (see next chart).

Population growth is going down while dwelling construction has lifted.

Finally, property price growth should slow on the back of declining affordability. Home values are rising far more quickly than incomes, meaning that an increasing share of buyers are being priced-out. As values rise, the pool of potential buyers will necessarily shrink.

Weighing all of the factors, our base case is for Australian property price growth to decelerate over the remainder of 2021 and then slow more sharply in 2022 once regulatory mortgage curbs are introduced, with the next property downturn to arrive in late 2022 or early 2023.

We do not expect recent lockdowns to alter this trajectory. Previous lockdowns witnessed a fall in both buyer activity and vendor activity before recovering to pre-lockdown levels once restrictions were eased or lifted. Essentially, the low stock levels supported prices while the various markets were placed on lockdown hiatus.