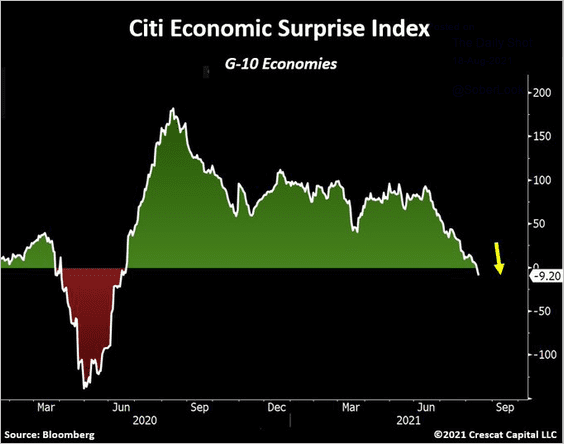

The growth scare has begun and forex is leading the way. DXY is poised to push higher on Fed policy error and safe haven flows as EUR tumbles:

Australian dollar is the free falling mirror image:

Gold is OK but oil is very definately not OK:

Copper has begun its great iron ore catch-up. All metals will follow:

Big miners are aflame:

EM stocks are a boulder gathering pace on a steepening slope:

Though junk is so far OK which means that either stocks will have to fall a lot more or a lot less than I fear:

The yield curve bull flattened:

Stocks puked 1%:

Fed minutes dominated the night. Taper is still go…ish:

Participants discussed aspects of the Federal Reserve’s asset purchases, including progress made toward the Committee’s maximum-employment and price-stability goals since the adoption of the asset purchase guidance in December 2020. They also considered the question of how asset purchases might be adjusted once economic conditions met the standards of that guidance. Participants agreed that their discussion at this meeting would be helpful background for the Committee’s future decisions about modifying asset purchases. No decisions regarding future adjustments to asset purchases were made at this meeting.

…In their discussion of considerations related to asset purchases, various participants noted that these purchases were an important part of the monetary policy toolkit and a critical aspect of the Federal Reserve’s response to the economic effects of the pandemic, supporting smooth financial market functioning and accommodative financial conditions, which aided the flow of credit to households and businesses and supported the recovery. Participants discussed a broad range of labor market and inflation indicators. All participants assessed that the economy had made progress toward the Committee’s maximum-employment and price-stability goals since the adoption of the guidance on asset purchases in December. Most participants judged that the Committee’s standard of “substantial further progress” toward the maximum-employment goal had not yet been met. At the same time, most participants remarked that this standard had been achieved with respect to the price-stability goal. A few participants noted, however, that the transitory nature of this year’s rise in inflation, as well as the recent declines in longer-term yields and in market-based measures of inflation compensation, cast doubt on the degree of progress that had been made toward the price-stability goal since December. Looking ahead, most participants noted that, provided that the economy were to evolve broadly as they anticipated, they judged that it could be appropriate to start reducing the pace of asset purchases this year because they saw the Committee’s “substantial further progress” criterion as satisfied with respect to the price-stability goal and as close to being satisfied with respect to the maximum-employment goal. Various participants commented that economic and financial conditions would likely warrant a reduction in coming months. Several others indicated, however, that a reduction in the pace of asset purchases was more likely to become appropriate early next year because they saw prevailing conditions in the labor market as not being close to meeting the Committee’s “substantial further progress” standard or because of uncertainty about the degree of progress toward the price-stability goal. Participants agreed that the Committee would provide advance notice before making changes to its balance sheet policy.

Participants expressed a range of views on the appropriate pace of tapering asset purchases once economic conditions satisfied the criterion laid out in the Committee’s guidance. Many participants saw potential benefits in a pace of tapering that would end net asset purchases before the conditions currently specified in the Committee’s forward guidance on the federal funds rate were likely to be met. At the same time, participants indicated that the standards for raising the target range for the federal funds rate were distinct from those associated with tapering asset purchases and remarked that the timing of those actions would depend on the course of the economy. Several participants noted that an earlier start to tapering could be accompanied by more gradual reductions in the purchase pace and that such a combination could mitigate the risk of an excessive tightening in financial conditions in response to a tapering announcement.

Participants exchanged views on what the composition of asset purchases should be during the tapering process. Most participants remarked that they saw benefits in reducing the pace of net purchases of Treasury securities and agency MBS proportionally in order to end both sets of purchases at the same time. These participants observed that such an approach would be consistent with the Committee’s understanding that purchases of Treasury securities and agency MBS had similar effects on broader financial conditions and played similar roles in the transmission of monetary policy, or that these purchases were not intended as credit allocation. Some of these participants remarked, however, that they welcomed further discussion of the appropriate composition of asset purchases during the tapering process. Several participants commented on the benefits that they saw in reducing agency MBS purchases more quickly than Treasury securities purchases, noting that the housing sector was exceptionally strong and did not need either actual or perceived support from the Federal Reserve in the form of agency MBS purchases or that such purchases could be interpreted as a type of credit allocation.

That reeks of hesitancy to me so a reversal may not be too hard to come by.

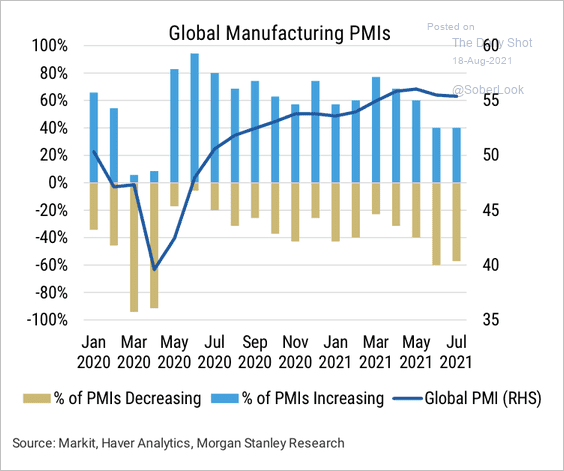

The problem is the reflation is cooked. Activity is topping as the global inventory cycle ends:

And price effects will follow in short order. In particular, in commodities as China’s credit clamps mow them all down.

If the Fed tapers on top then we’re now odds-on for building contagion into EMs, junk debt and broader equities.

The Australian dollar remains vulnerable.