For months we have been warning that the Australian Prudential Regulatory Authority (APRA) would impose macro-prudential mortgage restrictions to cool the market by the end of the year or early next, such as loan-to-value ratio (LVR) restrictions, debt-to-income (DTI) restrictions, increased mortgage buffers, or restrictions on interest-only lending.

These types of restrictions were imposed by APRA in December 2014 and March 2017 and quickly reduced credit growth in the targeted mortgage products.

Today, The Australian reports that APRA is becoming increasingly concerned about the frenzied pace of mortgage lending and has written to banks to put them on notice:

The letter from the head of the Australian Prudential and Regulation Commission sent to the boards of the biggest banks warns lenders to be “especially vigilant in managing the risks within their residential mortgage portfolios in the current environment”.

The letter, released under freedom of information rules, also gave bank boards just weeks to sign off on assurances that lending growth across the sector wasn’t reckless…

APRA chairman Wayne Byres told the banks in the letter, dated April 23, that the lending growth was coming in a backdrop of “extraordinarily low interest rates, high household indebtedness and accelerating housing prices”…

While borrowers were expected to have serviceability buffers in place it was important that “excessive debt levels are not being incurred by customers during a period of exceptionally low interest rates,” Mr Byres said.

The chair of the Council of Financial Regulators, Reserve Bank of Australia (RBA) governor Phil Lowe, also told a parliamentary committee on Friday that he couldn’t “rule out regulators taking action to curb excessive household credit growth over the coming year… APRA at some point would be preparing interventions”.

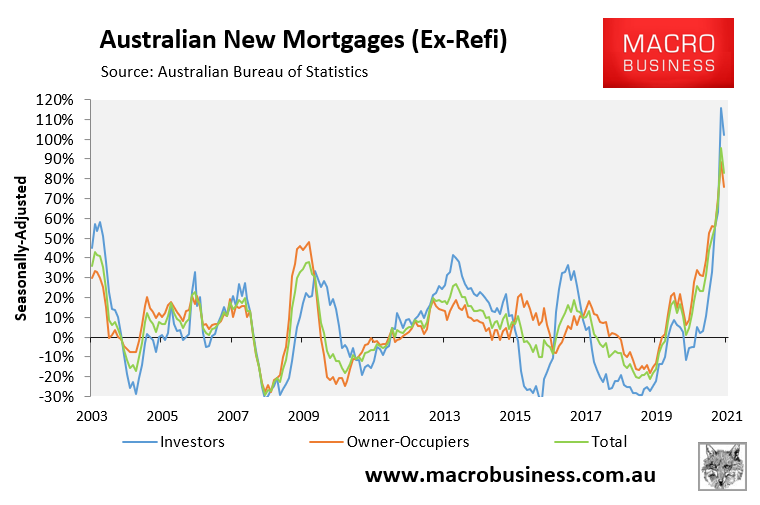

Growth in investor mortgage commitments, in particular, has surged.

So, with the RBA even less likely now to raise interest rates given the nation’s various lockdowns, and house prices and mortgages continuing to grow at a swift pace, the odds of APRA intervening with macro-prudential mortgage restrictions have increased.

The latest Delta lockdowns have pushed back the date for tightening a little, with Phil Lowe last week also suggesting that it would not happen this year.

That will take us into the question of whether regulators will pull the trigger before next year’s federal election, due in May.

Either way, macroprudential tightening is visible and approaching.