The ABC’ business editor Ian Verrender has published an explosive report on how Australia’s wealthy use Australia’s superannuation concession system to shelter themselves from paying taxes:

Back in 1992, when compulsory superannuation was introduced, it was supposed to take the pressure off federal government finances; to augment the age pension.

But superannuation tax breaks introduced over the decades since now threaten to overwhelm the budget within the next 20 years, costing more than a national pension.

Along the way, those tax breaks have helped transform the scheme from a retirement fund into a tax shelter, primarily used as an intergenerational wealth transfer system for the nation’s richest families…

The ATO data is two years old. But it shows a dramatic lift in wealth among the top self-managed funds from the previous year, with 27 funds holding more than $100 million each…

The existing tax concessions come at a huge cost — around $36 billion, according to last year’s budget papers. That’s more than double and close to triple what we spend on unemployment benefits…

Logically, it makes no sense to force a worker struggling on $60,000 a year, probably with no house, to be paying a higher tax rate than a person with $100 million in a superannuation account…

Which makes you wonder. Perhaps we would have been better off with a government-run sovereign wealth fund, like the one set up by Mr Costello for public servant superannuation…

If the federal government ever hopes to return the budget to some kind of balance, something needs to be done and quickly.

MB has been making the same arguments for years.

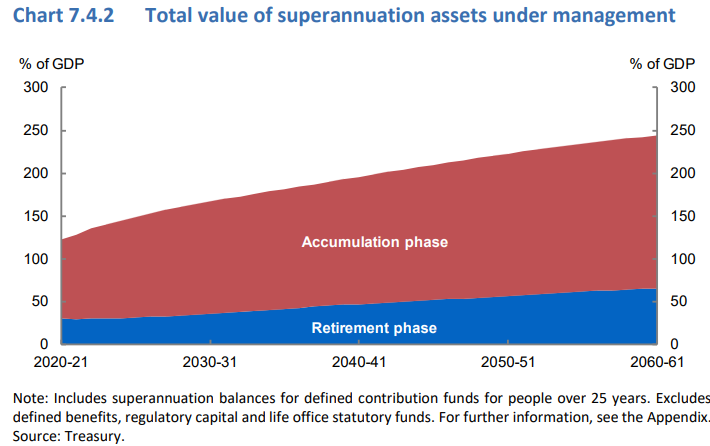

Treasury’s Intergenerational Report showed that superannuation funds under management will soar from around 157% of GDP currently to a projected 244% of GDP by 30 June 2061:

Superannuation assets will grow strongly.

Advertisement

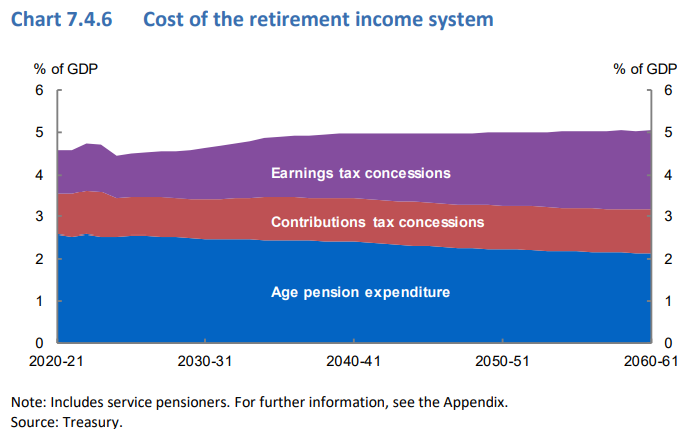

The IGR also showed that the cost of superannuation concessions will over take the cost of providing the aged pension by around 2040:

Cost of superannuation to overtake aged pension by 2040.

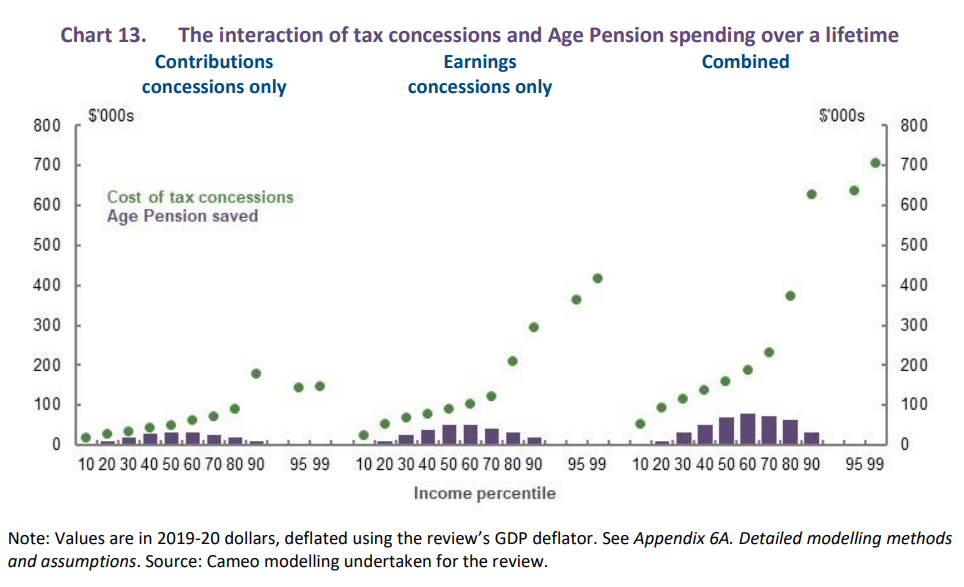

Meanwhile, Treasury’s Retirement Income Review, released last year, estimated that the superannuation system will cost taxpayers more in net terms over the long-run, that is after taking account savings in Aged Pension costs. The Retirement Income Review also showed that superannuation concessions are poorly targeted to high income earners, thereby increasing inequality:

Advertisement

To the extent that superannuation tax concessions are contributing to higher superannuation balances of lower- to middle- income earners, they help to reduce Age Pension expenditure. But the main influence behind the growth in superannuation balances is the SG. Tax concessions are largely concentrated among higher-income earners who are close to and above preservation age. Across the income distribution, the lifetime cost of superannuation tax concessions is projected to outweigh the associated Age Pension saving (Chart 13)…

Therefore, the biggest winners from Australia’s superannuation system are the funds themselves, which will get to glean fatter fees from the strong growth in funds under management.

But for Australian taxpayers, it would make more sense to unwind the superannuation system altogether and direct the budget savings into providing a more generous and comprehensive Aged Pension.

Advertisement

The decision to lift the superannuation guarantee to 12% is the entirely wrong policy that will only succeed in further feathering the industry’s nest.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.