In the May 2021 Budget the Morrison Government broadened eligibility to the Pensions Loan Scheme (PLS): the government sponsored reverse mortgage scheme that allows retirees to borrow up to 150% of the aged pension rate against the equity in their home and is open to all retirees (not just pensioners) over the age of 60.

Thus, a full rate pensioner can receive a maximum income top-up that is equal to half of the age pension, whereas a self funded retiree can receive a maximum payment that is equal to 1.5 times the full age pension.

The budget changes appears to have had the desired effect with participation in the PLS increasing five-fold over the past two years:

Just 768 people had accessed the scheme at the end of the 2018-19 financial year but their numbers swelled to 4039 by the end of March this year…

Figures cited by the academics show about two-thirds of PLS participants at the end of last year were full-rate pensioners, with most of the rest part-pensioners. Uptake by self-funded retirees is relatively small.

“The Pension Loans Scheme plays an important role, as the family home is typically a retiree’s largest financial asset,” the UNSW authors say.

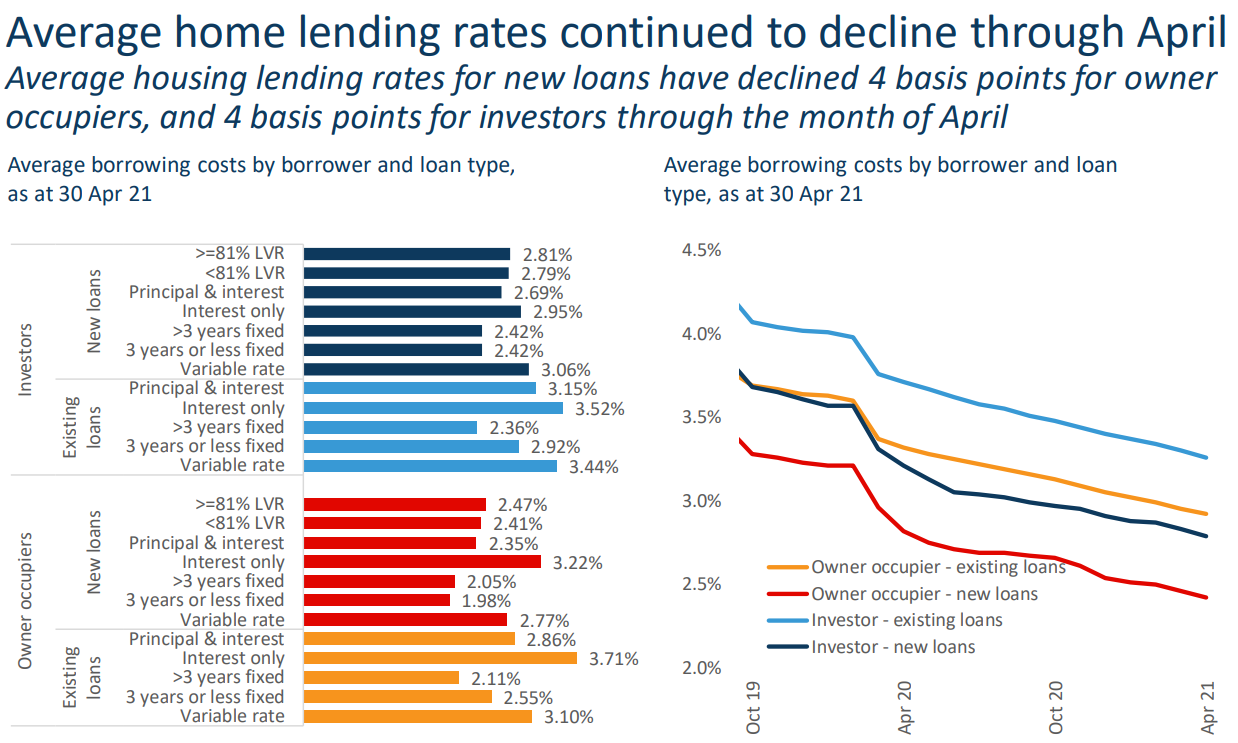

The biggest barrier precluding use of the PLS is the 4.5% interest rate charged, which is lower than commercial reverse mortgages but far higher than mortgages used to purchase homes:

Average mortgage rates are much lower than the PLS.

The federal government should probably reduce it to around 3.5% given the sharp decline in market mortgage rates and the ultra-low borrowing rates on government bonds.