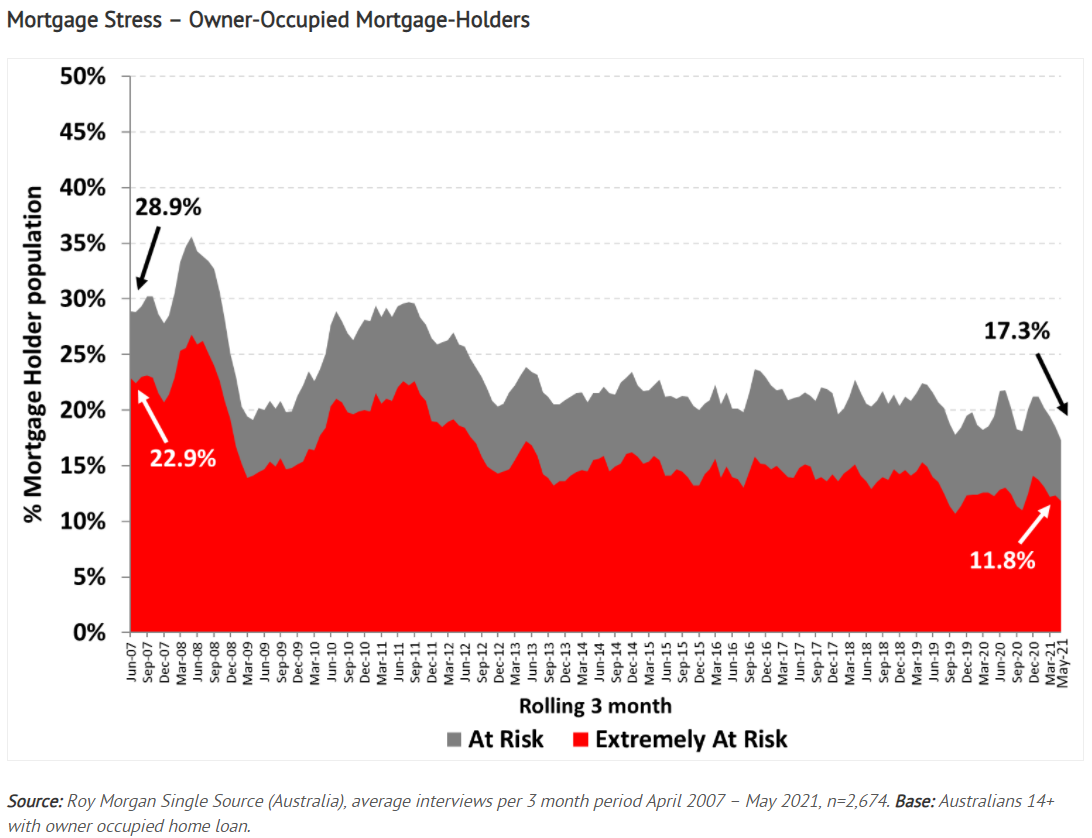

According to Roy Morgan, mortgage stress plunged to a near record low in the three months to May, driven by the lowest mortgage rates on record alongside the rebound in jobs:

New research from Roy Morgan shows an estimated 677,000 mortgage holders (17.3%) were at risk of ‘mortgage stress’ in the three months to May 2021. This period encompassed the end of the JobKeeper wage subsidy (end of March 2021), low community transmission of COVID-19 and only a few ‘short and sharp’ lockdowns and border closures to deal with outbreaks.

This level of mortgage stress is down sharply on a year ago when an estimated 794,000 mortgage holders (19.4%) were at risk during the early stages of the COVID-19 pandemic in the three months to May 2020.

The low rate of ‘At Risk’ mortgages since the pandemic began reflects the improvement in employment conditions in the first half of 2021…

The enduring impact of the record financial support provided to Australians over the last 18 months as well as the record low interest rates, set by the RBA at only 0.1%, are providing an enduring level of support to mortgage holders during 2021 even after much of this support has been withdrawn…

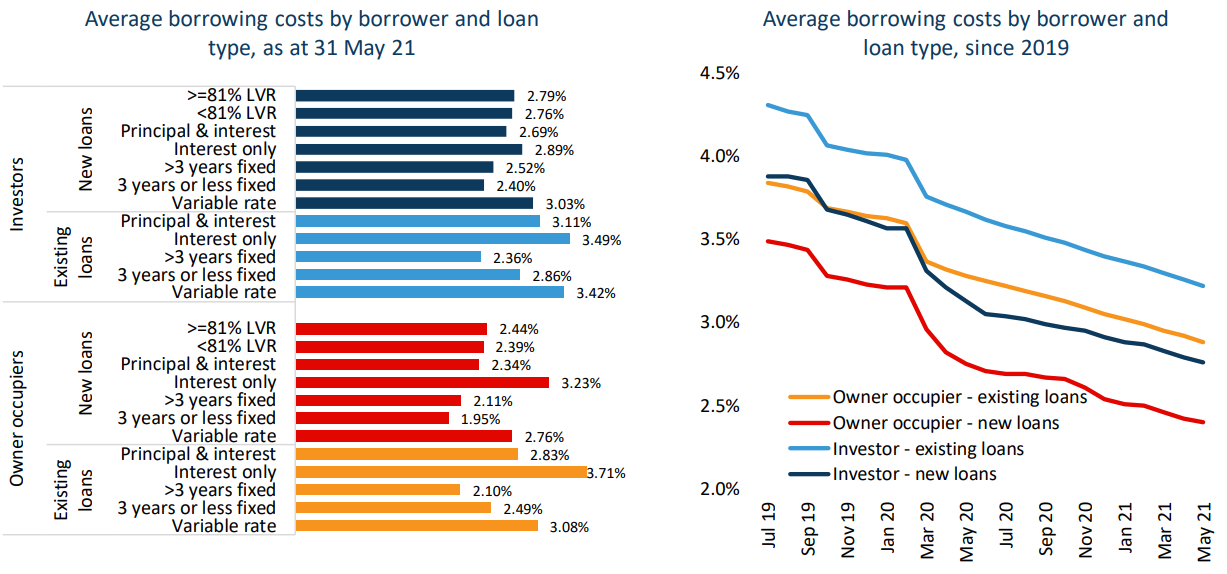

The improvement in mortgage stress makes perfect sense given the collapse in mortgage rates:

Mortgage rates at record lows.

Advertisement

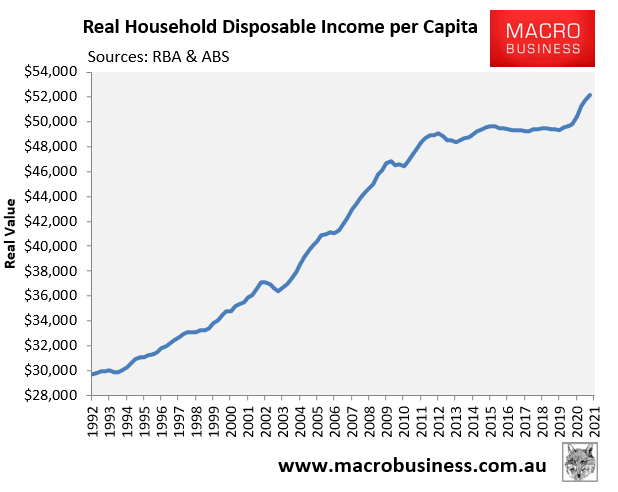

Alongside the stimulus-driven rise in household disposable income, which experienced its biggest annual rise since 2008:

Real per capita household disposable income has broken a decade of stagnation.

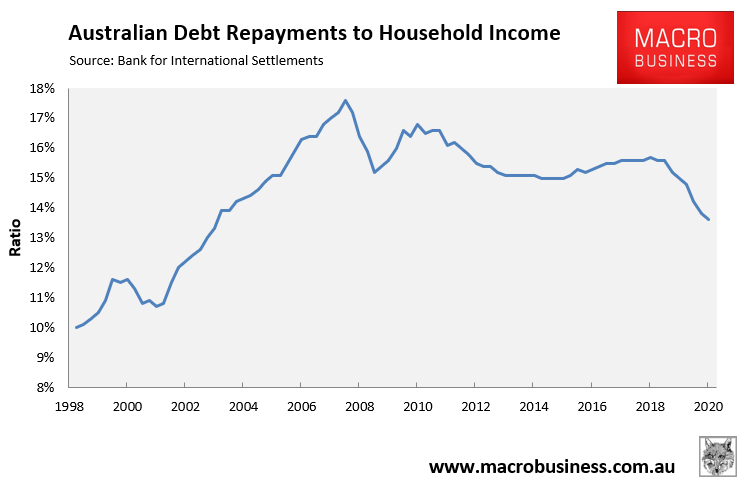

Combined, these factors have driven the ratio of debt repayments – both principal and interest – to household disposable income to a 17 year low, according to the Bank for International Settlements:

Advertisement

Australian household debt repayments have fallen to a 17 year low compared to disposable income.

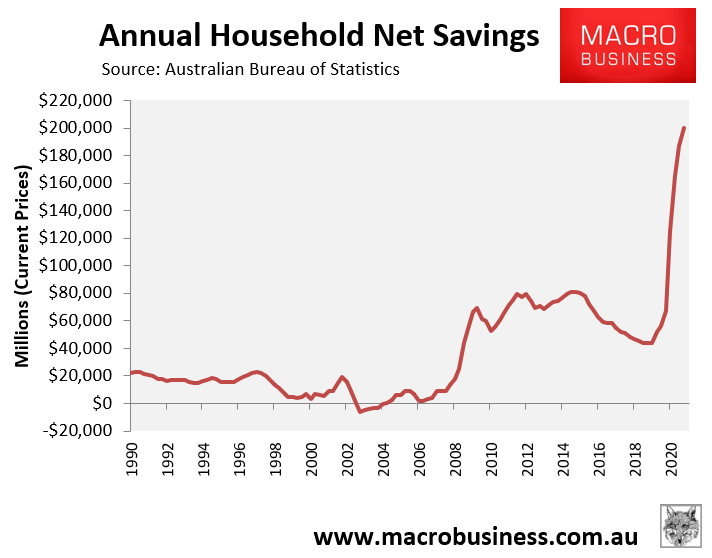

Meanwhile, Australian households have built up a massive war chest of savings, which suggests they are on aggregate households are in a strong financial position:

Australian households saved a record $200 billion in the year to March 2021.

Advertisement

Of course, all of this data precedes the latest lockdowns, which could lead to rises in mortgage stress; although this would be mitigated by renewed mortgage repayment holidays and stimulus.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.