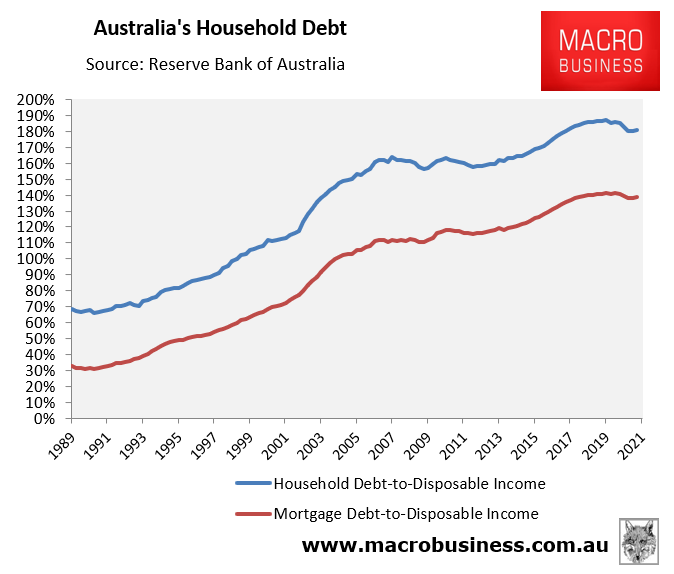

The Reserve Bank of Australia (RBA) yesterday released household finances data for the March quarter of 2021.

This data showed that the ratio of household and mortgage debt to disposable income rose slightly to 180.9% and 138.8% respectively over the March quarter:

Still below peak.

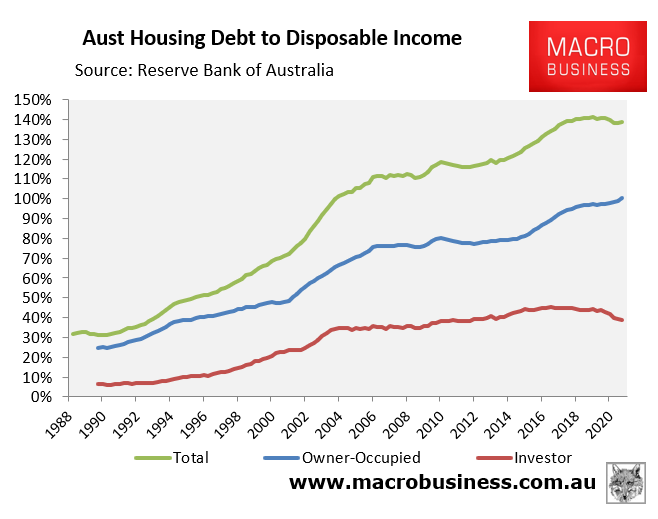

Household debt is being driven by owner-occupier mortgages, where debt levels hit a record high 100.2% of household disposable income in the March quarter, whereas investor mortgage debt fell to 38.6% of household disposable income:

Owner-occupier debt at a record high.

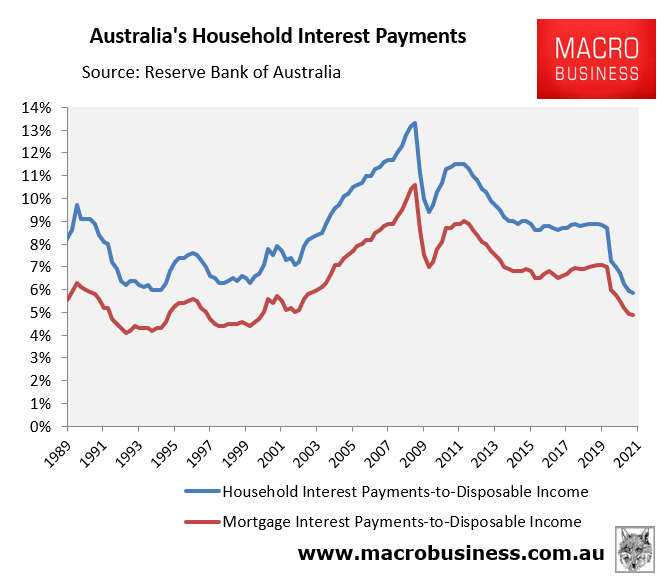

At the same time, the collapse of mortgage rates has driven the ratio of interest payments as a share of household disposable income to a 21-year low, as illustrated in the next chart:

Cheap money.

Specifically, the ratio of household debt to income fell to 5.8% in March 2021, less than half the peak of 13.3% in December 2008.

In a similar vein, the ratio of mortgage debt to income fell to 4.9% in March 2021, less than half the peak of 10.6% in December 2008.

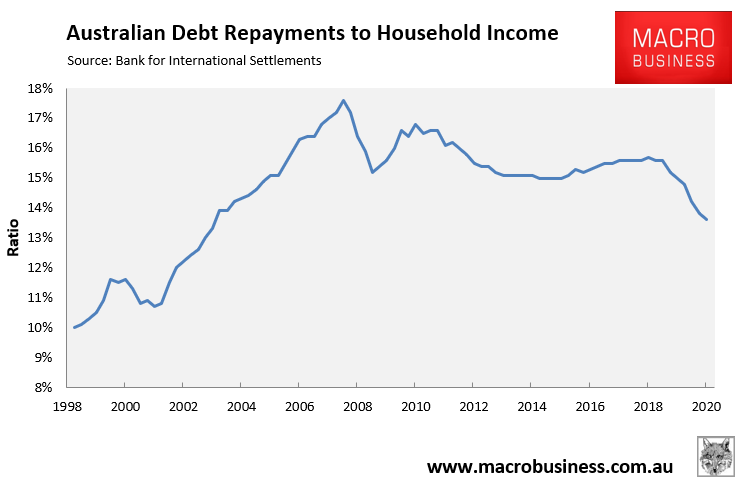

Finally, separate data from the Bank for International Settlements shows that debt repayments (both principal and interest) as a share of household disposable income fell to a 17 year low of 13.6% in the December quarter of 2020, which is 4.0% below the June 2008 peak of 17.6%:

Household’s debt repayment burden has shrunk.

In summary, Aussie households are sitting pretty despite their big household debt loads. Problems won’t arise until interest rates begin to rise.