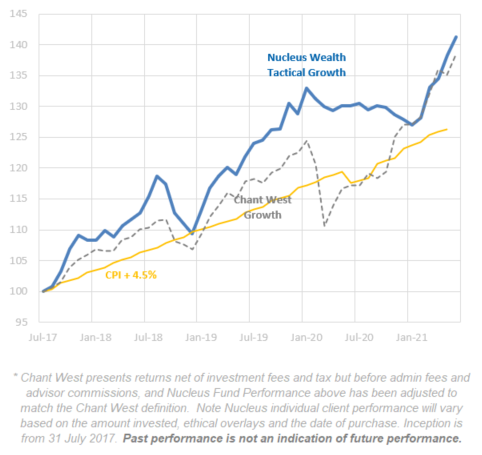

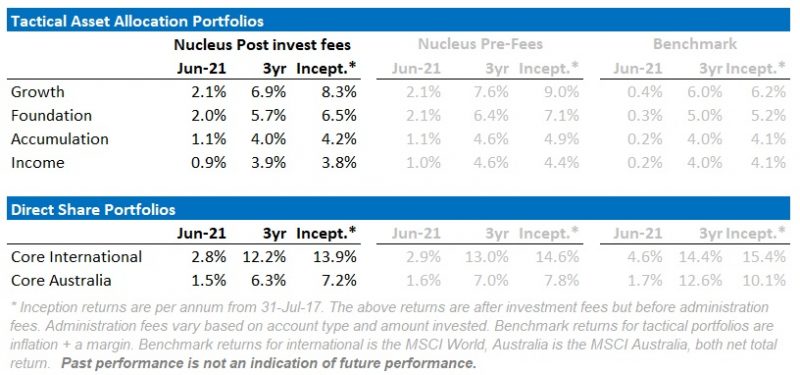

June was another strong month for the stock market. Our tactical portfolios performed well, up between 0.9% and 2.1% over the month. On the one hand, we timed the rotation out of value stocks and into quality stocks well; the inflation fears that were so prevalent a few weeks ago have faded as our inventory supercycle thesis plays out largely as expected. On the other hand, travel stocks were hit hard as the delta variant extends lockdowns and limits imminent reopening prospects.

Sometimes in investment, you need to take your lumps and move on – the market is telling you that you are wrong. Other times, you need to hold your nerve until the market realises the value. After a stellar opening to the year, travel stocks have been a drag on our performance for several months now. On travel stocks, we are opting to hold our nerve. Vaccines are proving effective, and our view is that when reopening happens there will be a pent up demand for travel which will drive these stocks higher.

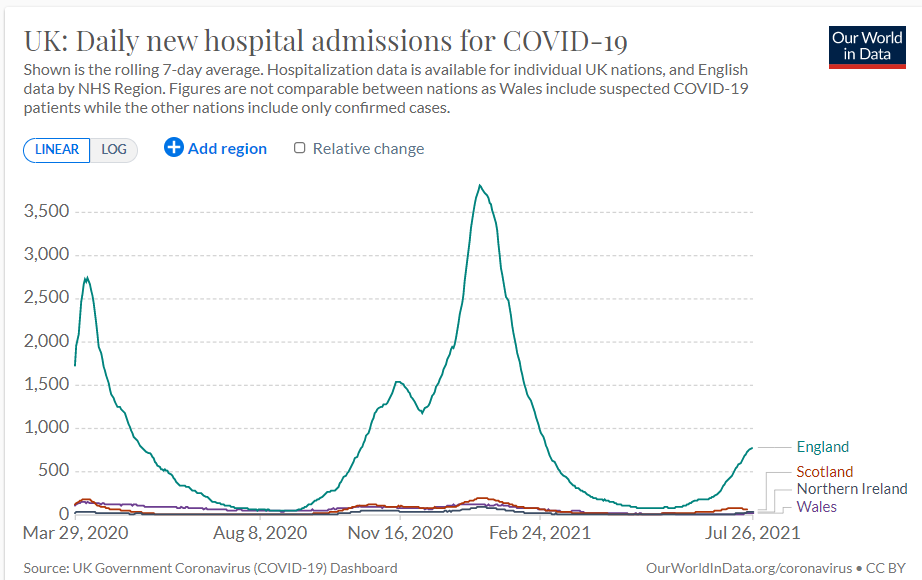

There are two main countries to watch. The UK is the primary test case. What happens when a (mostly) vaccinated population opens up without regard to the virus. Case counts have turned down. Hospitalisations are up but nowhere near prior levels. Vaccinated people appear well protected from the most negative outcomes. But, the trend is not good (see below). I’m optimistic, but the results are inconclusive so far.

The US is also a fascinating experiment in which levels of vaccination matter. Effectively there is a giant experiment with 50 states having varying lockdown rules, vaccination levels and economic support. It will provide insights into what are the vaccination thresholds for opening.

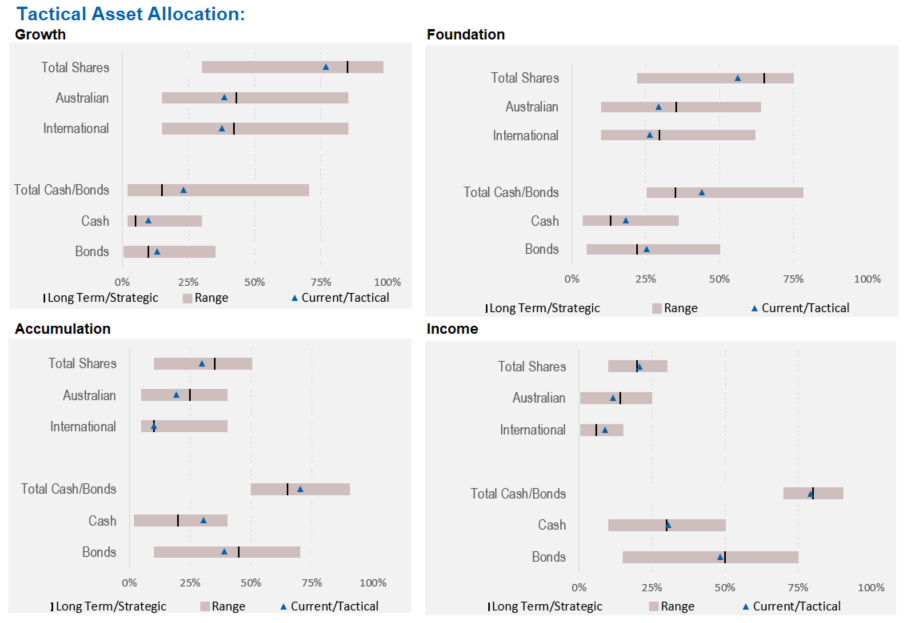

Asset allocation

Stock markets are expensive. Debt levels are extremely high. But earnings growth is strong. Really strong. And government/central bank support continues. Which means asset allocation is tricky.

Markets are supported to a great degree by central banks and governments. Policy error is every investor’s number one risk.

But, any number of other factors could force this off course and see unexpected inflation. Mutations could disrupt supply chains again. Chinese/developed world tensions might rise further, leading to more tariffs. Or, China might reverse its tightening on property sectors. Biden may get through additional stimulus, driving increases to minimum wages.

If we knew for certain inflation would fall, and tail risks would be quiet, then a barbell portfolio with long-dated bonds, defensive equities and growth equities would be a good option. Underweight banks, resources, cyclical equities. Overweight international stocks.

This is our aspirational portfolio. But it isn’t time to go 100% there yet. The inflation scare will probably ebb rather than collapse. We are progressively shifting our portfolios as pricing permits.

Earlier in the year, we were hiding at the short end of the bond yield curve. Last month we normalised that exposure and bond yields have continued to fall throughout July vindicating the shift to duration.

Australian equities have been a good source of investment performance in recent months. Now, they are facing a higher risk of reversal. It is time to use the high prices here to switch to international equities. We are building the defensive side of the portfolio up, changing out of value winners like resources, banks and cyclical industrials. A more aggressive switch into quality/growth is ahead if we see the opportunity developing.

We have two main scenarios:

- Stock markets grind higher on the back of improving earnings and fiscal support

- A growth “hole” emerges and markets fall until more support is provided

Stockmarket Grind Higher Case

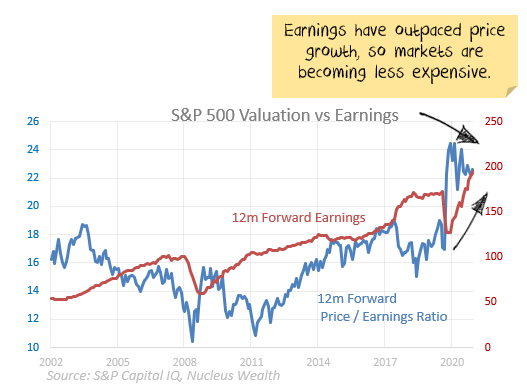

There are two ways to fix overpriced stockmarkets: prices fall or earnings rise. So far it has been the latter:

Could earnings continue to rise on the back of:

- Supply chain bottlenecks clearing and input prices falling.

- Continued productivity gains from business changes brought on by lockdowns (less staff, more automation, more work from home, lower commercial rents).

- Continued low wage growth.

- Government support.

- Reopening demand.

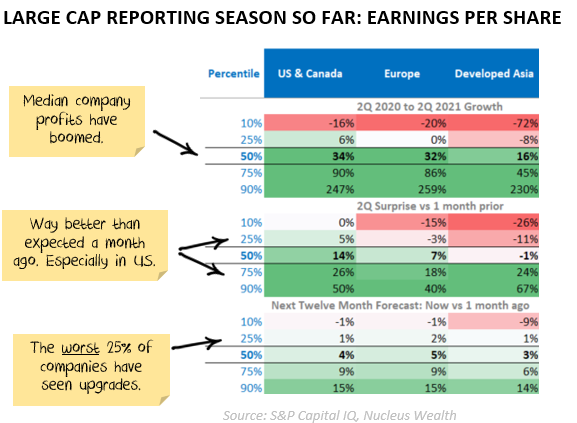

Absolutely. The 2nd quarter earnings season shows how:

If you avoid equities, your key risk is earnings boom more than expected. By my numbers:

- the median stock P/E is about 15% above both its 10 and 25 year averages

- it more like 20% in the US and on a cashflow basis

- it gets worse the more expensive you go – i.e. the 25th percentile (expensive) of stocks is about 25% more expensive than average but the 75th (cheap) is only 5% more expensive than average. The 90th percentile is actually cheaper than average.

- could earnings be 15% better than expectations based on government support and pandemic-led productivity gains? Quite possibly. That would put valuations back to their 10/25 year averages.

The danger of being out of the market is that government support remains high, bond yields low, inequality remains high. There is a surplus of investment over consumption and so valuations bounce between being (say) 5% and 25% more expensive than in the past. If we are trapped in this scenario for the next decade, then markets might continue to grind higher and more conservative investors might never get a signal to invest.

Stockmarket Downside Case

The bigger risk for markets is a growth “hole” emerging. There are two sources of this: China and the US.

China Growth

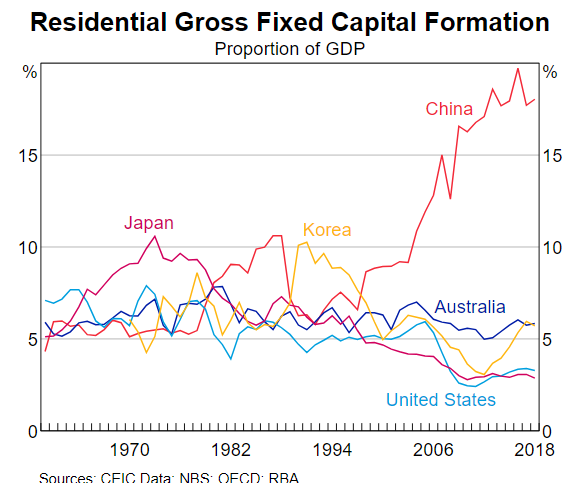

Chinese growth is a major consideration. Debt growth has slowed considerably, and a broad range of measures are rolling over. Effectively China is using the strength in the manufacturing sector to rebalance its economy away from its unsustainable reliance on property development. Residential investment in China as a proportion of GDP is double the level of Japan before its housing crash, and three times higher than the US before its housing crash:

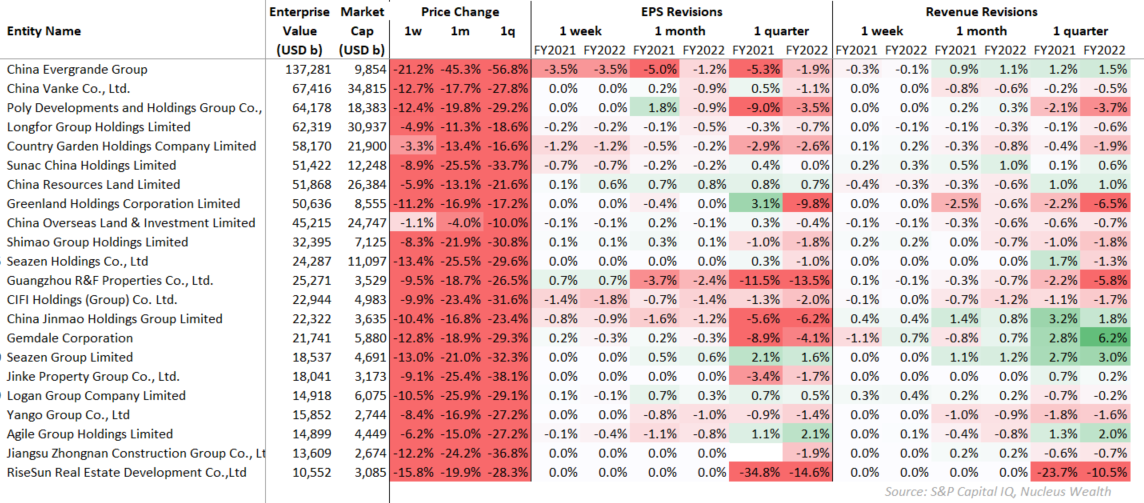

If we are right that the manufacturing boom is a short-lived inventory supercycle rather than a long term structural change, then this support will disappear. Chinese developers are pricing disaster:

The largest developer, Evergrande now has 14x more debt than equity. Evergrande’s bonds are priced for default.

There is a reasonable risk case that current conditions morph into a 2015-style Chinese slowdown which saw commodity prices tumble 50%+ and share prices down 10-15%. See our China Problem post for the full background.

US Growth

US growth faces a different problem. The direct-to-consumer stimulus has largely finished. The next stage of growth is from infrastructure stimulus which is six months away at least. Could there be a “growth gap” between the two programs that causes the US economy to slow?

It is not my base case, but it is clearly a significant risk.

Cavalry to the rescue?

- here is every possibility that at that the Chinese government will stamp the debt accelerator if growth slows too much and restart the cycle. But there will be a lag.

- we think an “end of cycle” event seems to be a low probability at this point – central banks and governments are all-in on preventing the worst outcomes

- however, a pullback in stock markets of 10-15% is a reasonably likely risk case, a warning shot to get central banks and governments to act.

As I have said many times, and will no doubt continue to say:

We are not in a normal market. We are reliant on government and central bank support. So policy error remains the number one risk.

Performance Detail

June was an emphatic up month as all the equity indices marched onward and upward even accelerating toward the end of the month. Our Core portfolios had another strong month.

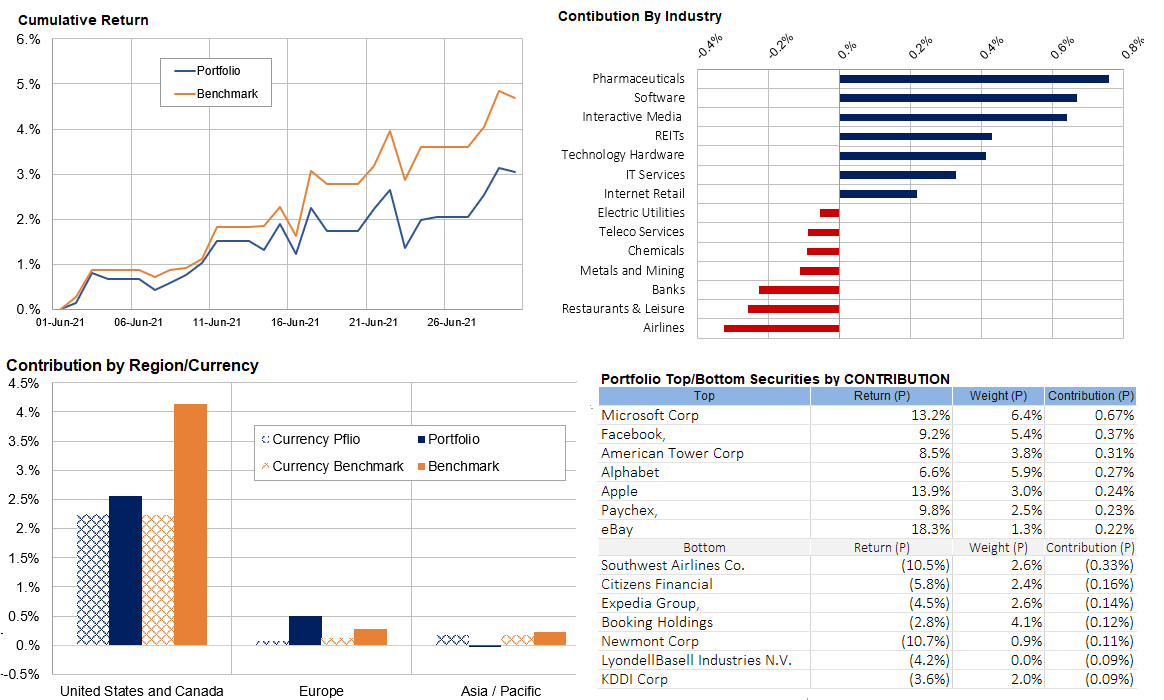

Core International Performance

The market switchback into Technology/Growth and especially the FAANGs over June saw our international portfolio put on 2.8% over June. However, our travel exposures underperformed which meant we didn’t capture all the gains seen in the US market. The European stocks performed well while Asia detracted.

The pivot has worked the other way in July, reversing the June underperformance to date.

Overall the currency effect assisted all the returns especially the weakening of the AUD vs the USD.

In early June we continued our pivot from our Value trade exiting Cement/Chemical stocks and upweighting quality technology plays.

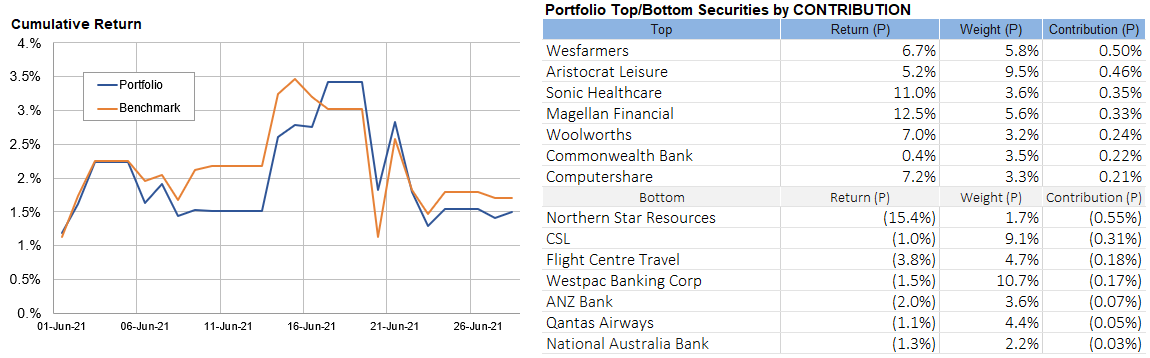

Core Australia Performance

The Core Australian portfolio slightly underperformed the index this month, Travel stocks and Gold the key detractors. Over the month we reduced our Resource exposure and upweighted Technology and Financials.

Want to see what an investment with the MB Fund would look like for you? Create an obligation-free account with our onboarding portal to begin tailoring your portfolio now

Damien Klassen is Head of Investments at Nucleus Wealth.

Follow @DamienKlassen on Twitter or Linked In

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. Damien Klassen is an authorised representative of Nucleus Wealth Management, a Corporate Authorised Representative of Nucleus Advice Pty Ltd – AFSL 515796.