Things are not looking good in risk-taking land with the COVID-19 delta variant causing a lot of concerns that are spilling over into equity markets which fell sharply overnight. Coupled with the snap OPEC supply surge that has seen oil fall over 7%, commodity markets and commodity currencies are selling off while Treasury yields are down to their February lows just below the 1.2% level in a sign that safe haven buying is accelerating.

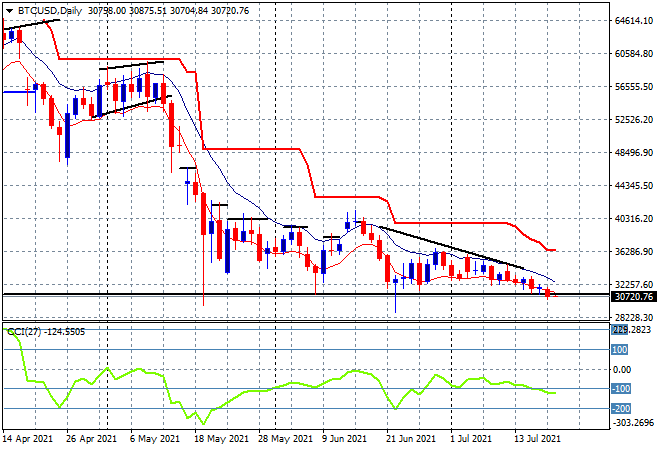

Bitcoin’s deflation continues with the return to the start of year position at $30K as the daily downtrend line (upper black sloping line) still holds on – remember turn this chart upside down and you’d be buying!

Looking at share markets in Asia from yesterday’s session, where the Shanghai Composite was down more than 0.7% mid session but clawed its way back and managed to close with a scratch session at 3539. Meanwhile the Hang Seng Index fell much sharper, down 1.8% to decisively break below the 28000 point level to close at 27489 points. The daily chart was suggesting a possible bottom forming here after breaking down below daily ATR support at the 28100 point level but intrasession selling caused a reversion below the 28000 point level that has now turned into a rout as this dead cat bounce looks to revisit the previous lows below 27000 points:

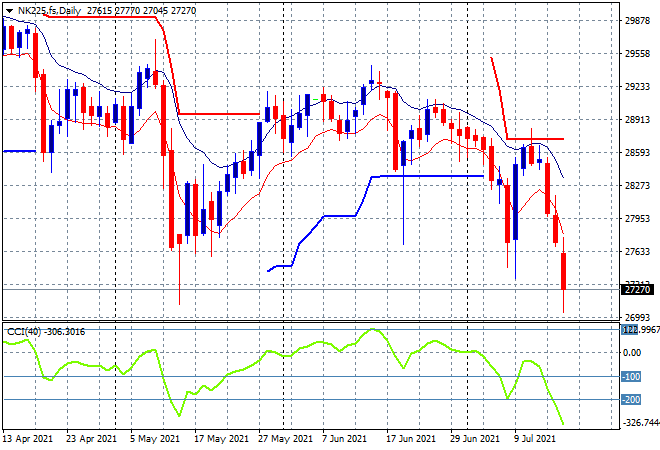

Japanese stocks joined in on the pity party with the Nikkei 225 closing 1.2% lower at 27652 points. Daily futures are suggesting further selloffs in line with overnight share markets as concerns around COVID at the Olympics and the wider US led risk off mood mount even further. Watch for a close below the previous daily lows at the 27000 point level to signal a new downtrend:

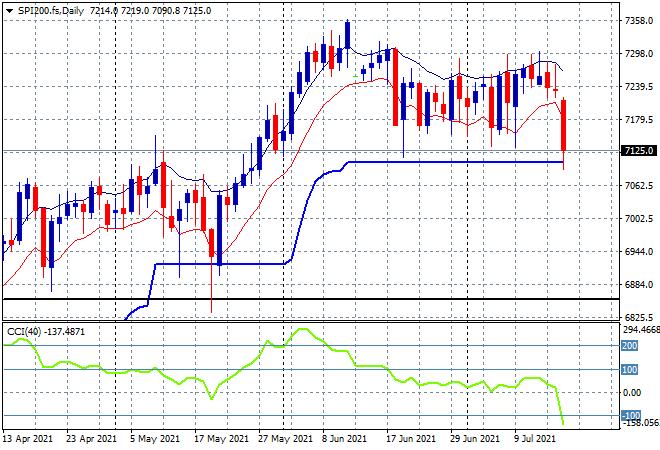

Australian stocks couldn’t escape the risk off mood with the ASX200 off by more than 0.8% to close at 7285 points. SPI futures are down another 1% so we could finally see a break of this sideways mood and a proper breakdown below ATR support at the 7150 point level with daily momentum switching sharply to oversold we could see the 7000 point psychological level breached:

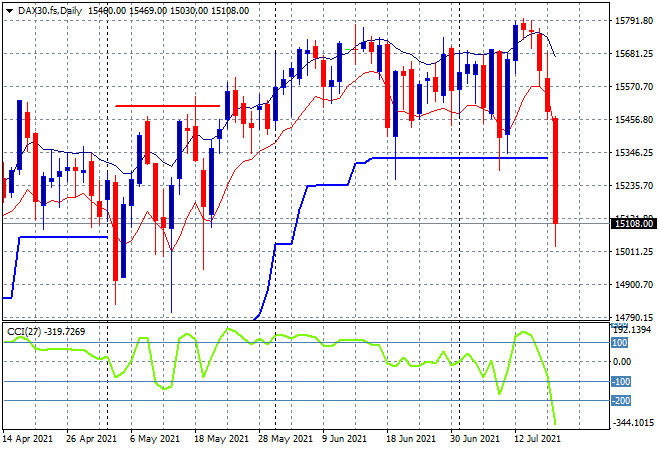

European markets accelerated their own selloff mode with some big falls across the continent, with all bourses down around 2.5% or more. The German DAX fell back 2.6% to 15133 points, crashing through daily ATR support at the 15300 point level with momentum nearly off the charts as a result. This could swing back sharply but it also reminds me of the previous second wave correction:

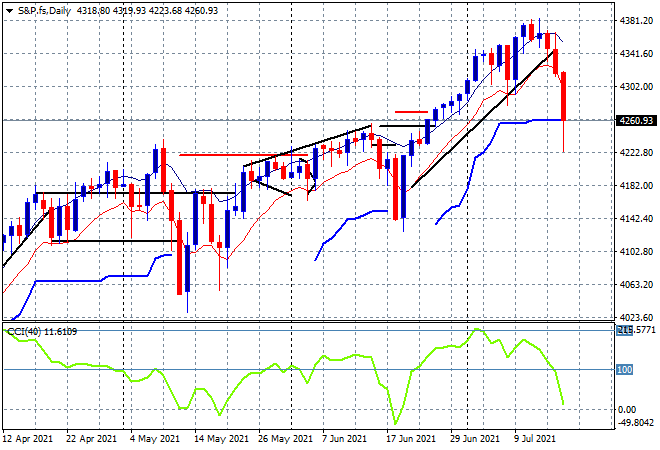

Wall Street also continued the downward trajectory with the headline Dow off by more than 2% while tech stocks were the least affected, the NASDAQ closing only 1% lower and the S&P500 finishing 1.6% lower at 4258 points. The daily chart shows a clean break of the uptrend that held since the last dip mid-June with the key 4300 point level taken out this could widen quickly into a reversion back to the June lows. The market is still up over 30% for the last 12 months, so lot’s of heat to take here:

Currency markets generally moved in the same downward direction as US strength re-engaged although Euro was very resilient unlike commodity currencies in the wake of the collapse in oil prices. The union currency spiked up through the 1.18 handle but then stabilised at the start of week mid point once again. There maybe a short term bottom forming here but price has been unable to get anywhere near the weekly high at just below the 1.19 level for quite sometime now with momentum remaining in the negative zone:

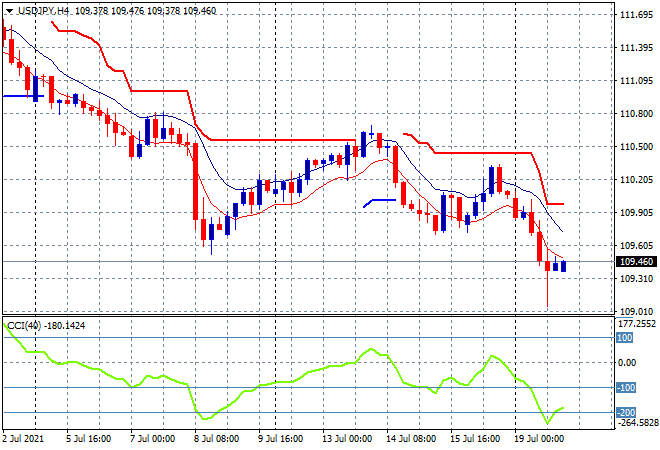

The USDJPY pair was pushed back well below the 110 handle as more Yen safe haven buying on the risk off mood overshadowed USD strength. Overhead trailing ATR resistance is pushing ever lower as momentum cracks into seriously oversold mode with the potential to swiftly break below the 109 level:

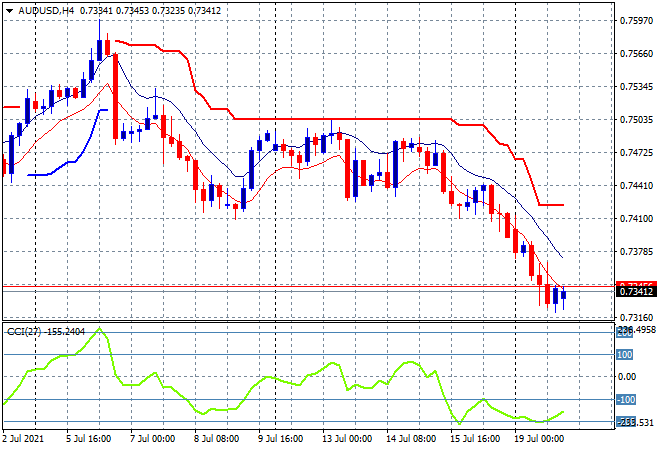

The Australian dollar was pushed lower on commodity prices with a nice fall through the 74 handle and a small deceleration into the 73.40 level as of this morning. You can’t help but be bearish for the Pacific Peso on almost any timescale, but watch for the slim chance of a short term boost from here on overselling – although I think it will be short lived:

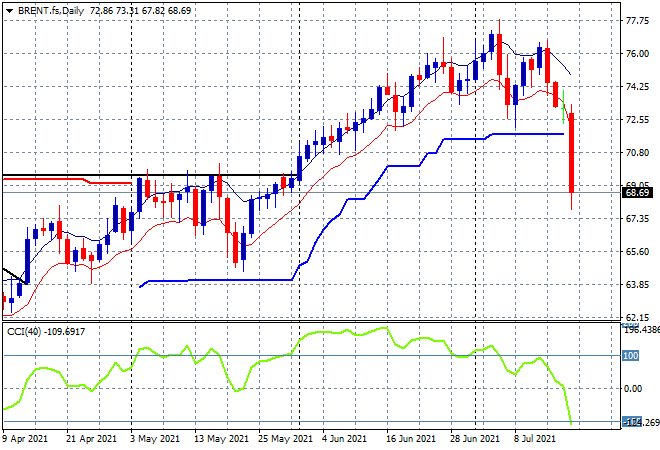

The fallout from the snap OPEC+ meeting on the weekend with increased supply coming online in August has seen both WTI and Brent crude crater to a new monthly lows, with the latter pushed well below the $69USD per barrel level overnight. Price and momentum were already pointing to a return to trailing ATR daily support at the $71 level but this breakdown spells more trouble ahead with the May lows around $63 the possible next target if momentum goes into further oversold readings:

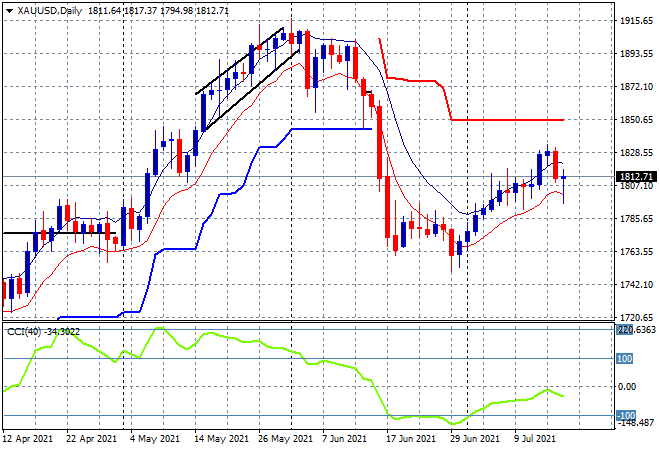

Gold was able to hold fast overnight after a brief dip below its own low moving average and what looked like a break of the uptrend since late June, finishing at the $1812USD per ounce level and staving off a successive new daily low. While daily momentum is not yet positive, its nowhere near oversold levels and this internal buying support may turn into stabilisation as long as the $1800USD per ounce level holds:

Glossary of Acronyms and Technical Analysis Terms:

ATR: Average True Range – measures the degree of price volatility averaged over a time period

ATR Support/Resistance: a ratcheting mechanism that follows price below/above a trend, that if breached shows above average volatility

CCI: Commodity Channel Index: a momentum reading that calculates current price away from the statistical mean or “typical” price to indicate overbought (far above the mean) or oversold (far below the mean)

Low/High Moving Average: rolling mean of prices in this case, the low and high for the day/hour which creates a band around the actual price movement

FOMC: Federal Open Market Committee, monthly meeting of Federal Reserve regarding monetary policy (setting interest rates)

DOE: US Department of Energy

Uncle Point: or stop loss point, a level at which you’ve clearly been wrong on your position, so cry uncle and get out!