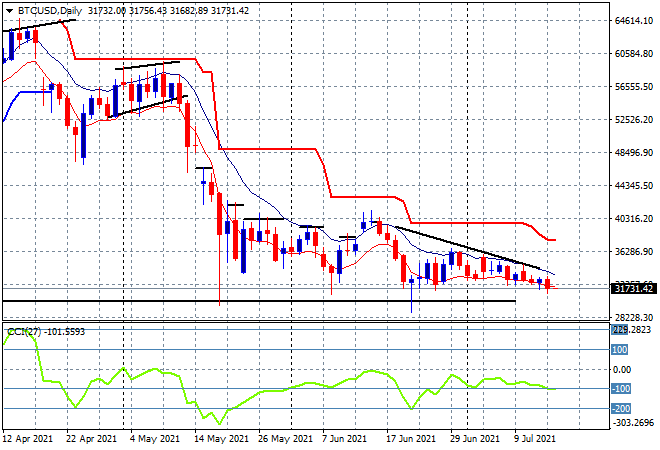

Risk markets continue to swing from hope to fear with the latter ruling again overnight without any obvious catalysts. Both European and US stocks fell back around 1% or so with commodities equally mixed as oil dropped 2% while industrial metals lifted. The USD rebounded after falling back midweek while bond yields also fell back to their weekly lows as Fed Chair Powell re-iterated the Fed’s stance to the Senate overnight. Bitcoin’s deflation continued with a return to the $31K level yesterday that has it on track to get back to the start of year position at $30K or lower as the daily downtrend line (upper black sloping line) still holds:

Looking at share markets in Asia from yesterday’s session, where the Shanghai Composite closed up a solid 1% taking back the previous losses to finish at 3560 points while the Hang Seng Index almost put in a similar result, up 0.7% to almost cross back above the 28000 point level. The daily chart is still suggesting a possible bottom forming here after breaking down below daily ATR support at the 28100 point level and momentum reverting from very oversold levels, but the picture still remains uncertain until a positive close above the 28000 point level is done:

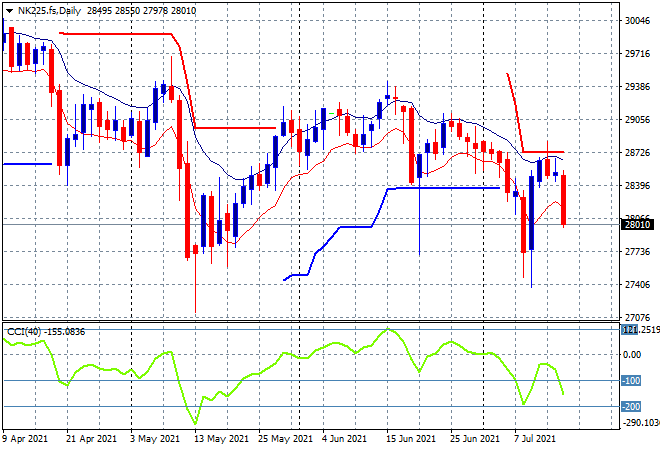

Japanese stocks however went the other way with the Nikkei 225 closing 1% lower at 28279 points, showing how mixed Asian markets are this trading week. Daily futures are now suggesting a further retracement as substantial resistance at the 29000 point level that has held since May just proves too strong against concerns around COVID at the Olympics. Watch for a close below the previous daily lows at the 27000 point level to signal a new downtrend:

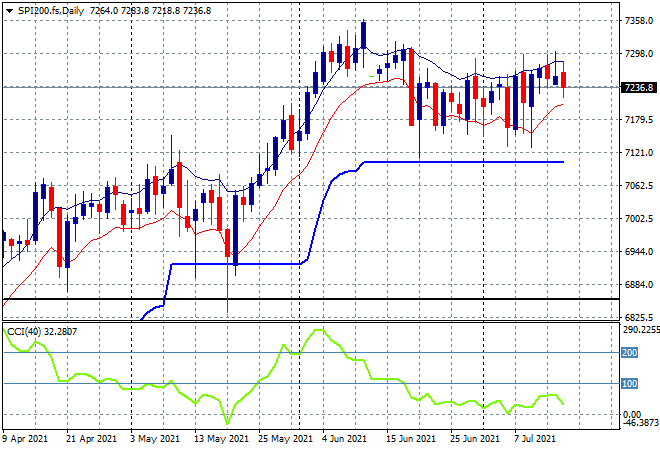

Australian stocks fell the least in response to the local jobs report with the ASX200 closing 0.3% lower at 7335 points. SPI futures are down around 10 points which should make for an unsteady finish to the week as more lockdowns weigh on the economy (this time imagine the Ministry of Silly Walks which the various State/Federal governments are doing a much better job at satire than Monty Python ever did). Daily momentum remains nominally positive and trailing daily ATR support at 7150 points is still holding however:

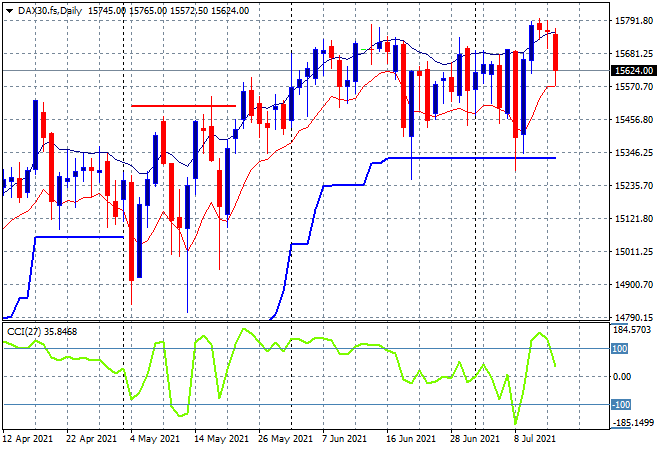

European markets have moved from stalled to selloff mode despite a lower Pound and Euro as sentiment soured yet again. Every major market lose around 1% with the German DAX falling back to 15629 points, remaining above daily ATR support at the 15300 point level but wiping out any chance of a potential breakout trade:

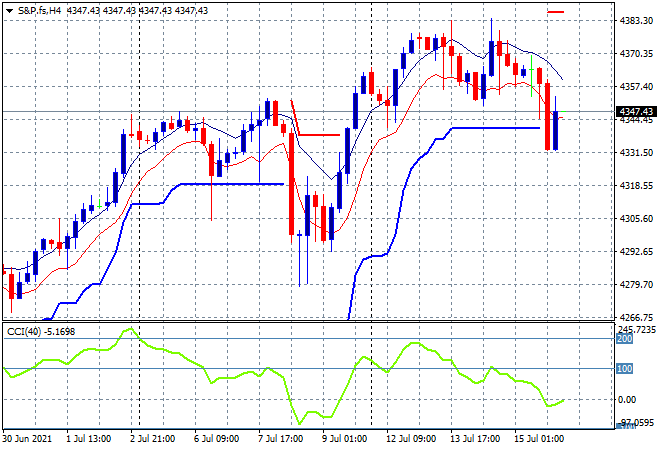

Wall Street joined in on the unanticipated for no reason selloff although the headline Dow eked out a tiny positive result, the NASDAQ lost 0.7% while the S&P500 finished 0.3% lower to close at 4360 points. The four hourly chart has been in stall mode since Tuesday’s session, unable to break above the 4390 level with last night seeing a retracement below trailing ATR support. Price is back to last week’s highs and could retrace further to the previous dip lows at the key 4300 point level:

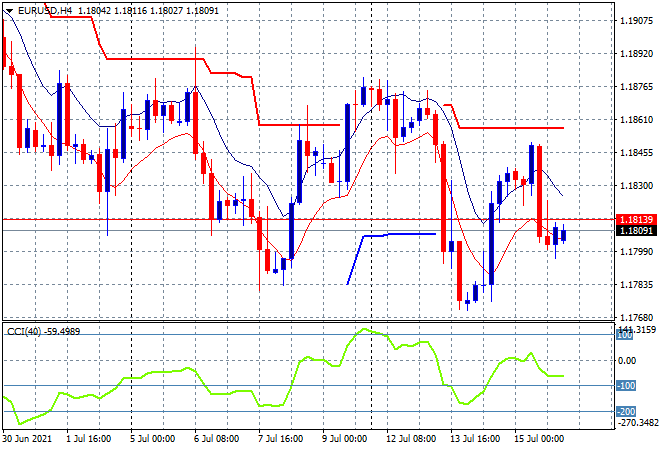

Currency markets were equally mixed not helped by mixed albeit secondary economic prints, namely UK unemployment and US industrial production. Euro was pushed back down to the 1.18 handle, undoing all the work that had been possibly forming a bottom here but as I said yesterday, don’t get too excited until the weekly high is taken out at just below the 1.19 level”

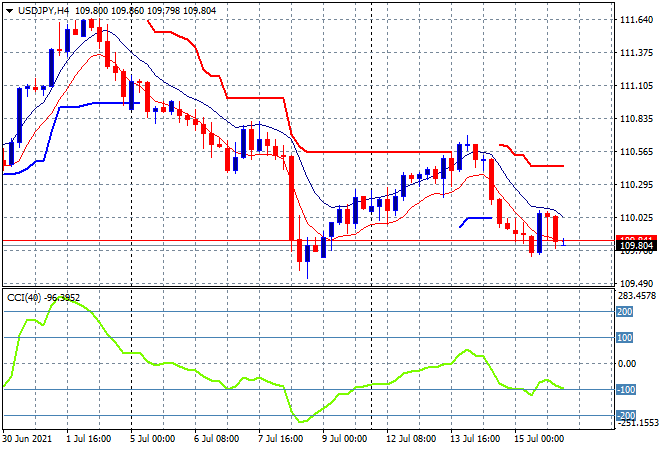

The USDJPY pair was pushed back below the 110 handle overnight on more Yen safe haven buying as the risk off mood accelerates both locally and potentially globally, returning to the intrasession low for the week after rebuffing overhead trailing ATR resistance at the 110.50 level. Momentum is almost in the oversold stage signalling more downside:

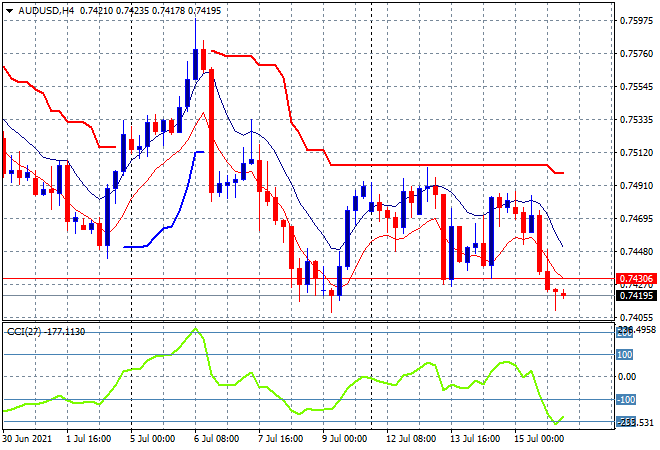

The Australian dollar was pushed lower once more on USD strength with a return to last weeks low just above the 74 handle after failing to make a new high in the previous session and indeed all week. Momentum has switched back to the dominant negative setting on the four hourly chart as overhead ATR resistance at the 75 level becomes a bridge too far for the Pacific Peso:

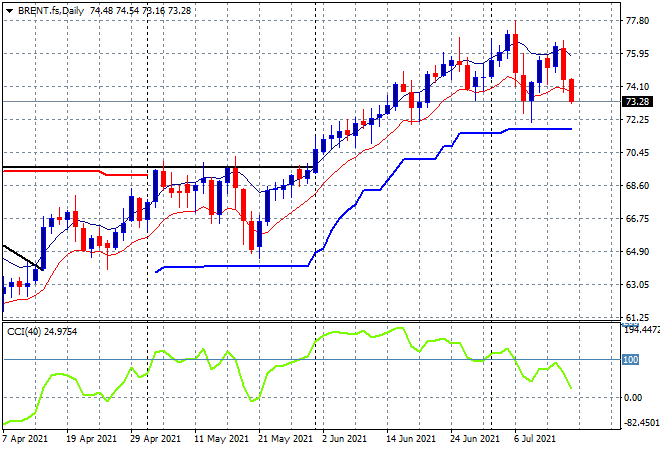

Oil continues to struggle here following last week’s OPEC+ meeting with Brent crude pulling back 2% overnight to a new weekly low just above the $73USD per barrel level after what looked like a breakout earlier in the week. Price and momentum are pointing to a return to trailing ATR daily support at the $71 level unless it can rally tonight to finish back inside the moving average band as a continuation pattern forms:

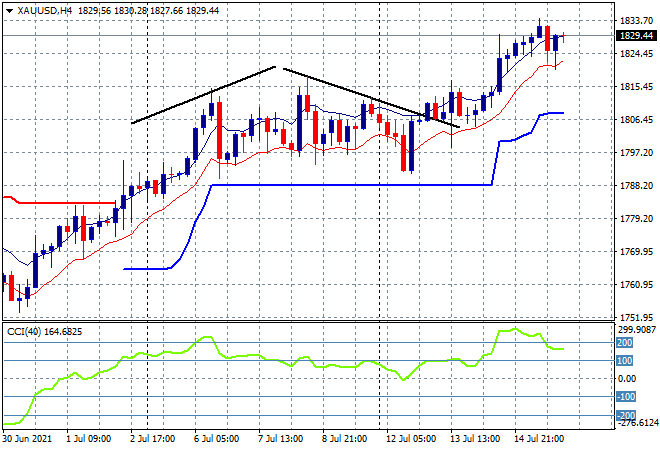

Gold’s breakout continued yesterday but had a mild pause overnight, maintaining a solid position here just below the $1830USD per ounce level. A new weekly high bodes well for the shiny metal going forward, but a look at the four hourly chart shows it must hold above the low moving average and short term support at the $1820 level:

Glossary of Acronyms and Technical Analysis Terms:

ATR: Average True Range – measures the degree of price volatility averaged over a time period

ATR Support/Resistance: a ratcheting mechanism that follows price below/above a trend, that if breached shows above average volatility

CCI: Commodity Channel Index: a momentum reading that calculates current price away from the statistical mean or “typical” price to indicate overbought (far above the mean) or oversold (far below the mean)

Low/High Moving Average: rolling mean of prices in this case, the low and high for the day/hour which creates a band around the actual price movement

FOMC: Federal Open Market Committee, monthly meeting of Federal Reserve regarding monetary policy (setting interest rates)

DOE: US Department of Energy

Uncle Point: or stop loss point, a level at which you’ve clearly been wrong on your position, so cry uncle and get out!