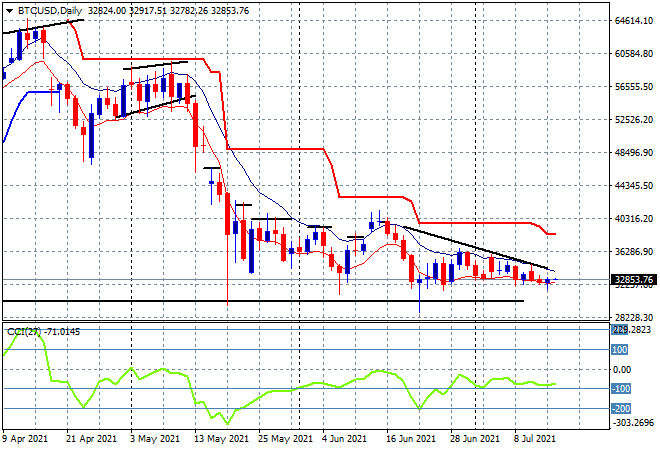

Last night saw markets listening to all the fancy words from Fed Chairman Powell in his semi-annual testimony as inflation concerns – aka taking the punchbowl away concerns – dominated events. Wall Street lifted while USD and bond yields fell back as Powell stated any tightening is still a way off, while European stocks continued to trend sideways. Gold was the standout, managing to lift up towards the $1830USD per ounce level. while Bitcoin’s deflation continued with a return to the $32K level yesterday enacting a small bounce. This rolled over overnight as the daily chart shows it ready to decline back to the start of year position at $30K or lower as the daily downtrend line (upper black sloping line) still holds:

Looking at share markets in Asia from yesterday’s session, where the Shanghai Composite closed 1% lower to finish at 3529 points while the Hang Seng Index also pulled back smartly, down 0.6% to 27787 points. The daily chart shows a possible volatile bottom forming here after breaking down below daily ATR support at the 28100 point level and momentum reverting from very oversold levels, but the picture still remains uncertain until a positive close above the 28000 point level is done:

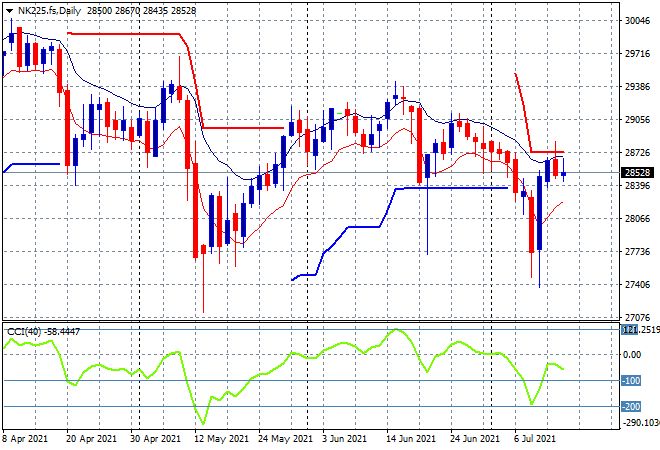

Japanese stocks also looked wobbly with the Nikkei 225 closing 0.3% lower at 28608 points. Daily futures are at best suggesting another sideways trend instead of a breakout developing here as a new trend higher requires at a minimum a new daily high above the high moving average and then clearing substantial resistance at the 29000 point level that has held since May:

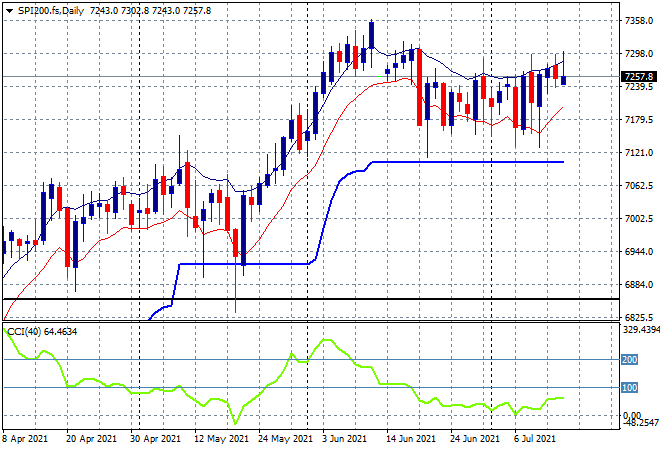

Australian stocks were the only ones to put on any runs as the Westpac consumer sentiment survey was very solid, the ASX200 closing 0.3% higher at 7354 points. SPI futures are down over 10 points despite the moves higher on Wall Street, as the lack of new daily highs continues to weigh heavily here (imagine a Monty Python naked foot on top of the chart). Daily momentum remains nominally positive and trailing daily ATR support at 7150 points is still holding however:

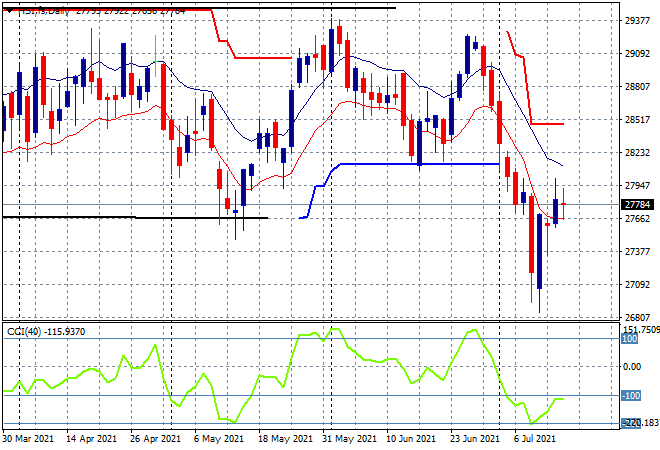

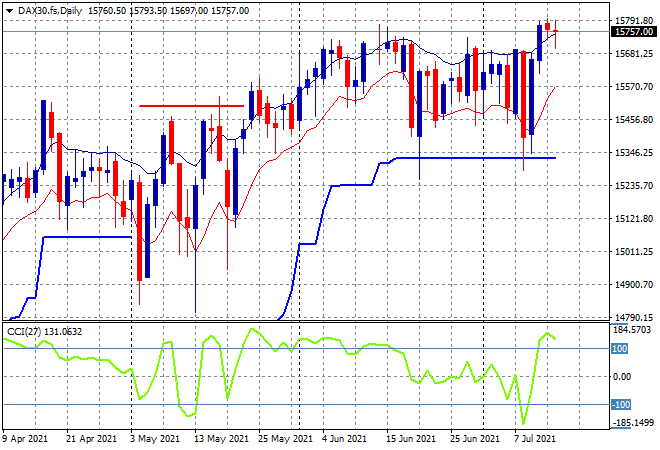

European markets were unable again to gain traction as UK inflation measures lifted more than expected and a higher Euro weighed on sentiment. While the FTSE lost 0.5%, the German DAX finished down a handful of points, remaining above daily ATR support at the 15300 point level but going nowhere. The potential breakout trade still requires more of a follow through here and more correlation with other risk assets like Wall Street:

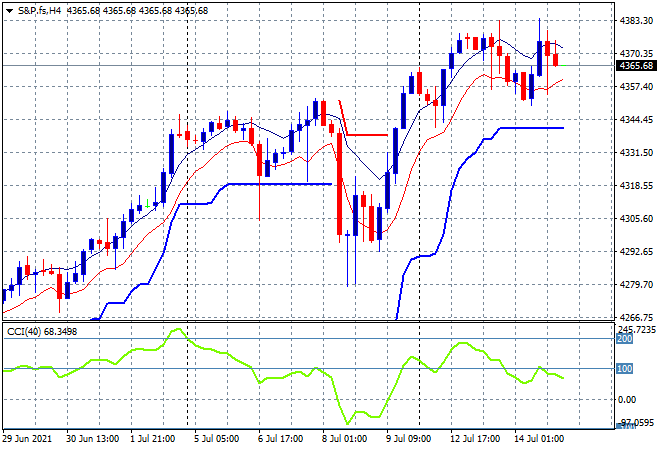

Wall Street this time did appreciate the inflation print comments from Fed Chair Powell, although earnings reports overshadowed, particularly tech stocks with the NASDAQ losing 0.2% while the S&P500 gained 0.2% to close at 4374 points. The four hourly chart shows a market still wanting to go higher with momentum reverting from its overbought status and price still holding above trailing ATR support. There is a possibility of a return to last week’s highs around the 4340 point level if more fallout eventuates from the inflation print, namely Fed hawks getting more vocal:

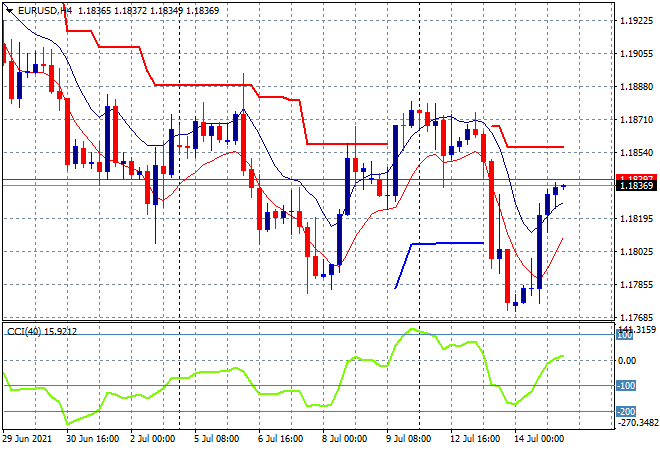

Currency markets responded strongly again to US inflation concerns with USD selling off against most of the majors, although Pound Sterling had a reprieve due to its own inflation troubles, with Euro pushing up through the 1.18 handle taking back most of the post US inflation print falls. Standing back, the four hourly chart is kind of transmitting a possible bottom forming here but there’s still quite a bit of work to do above the 1.1850 level and then 1.19 proper before getting too excited – this could prove transitory too:

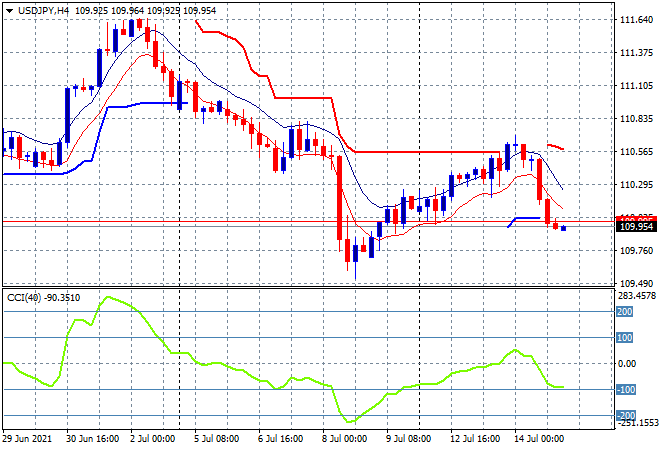

The USDJPY pair was hit hard overnight, retracing well below the 110 handle and making a new intrasession low for the week after rebuffing overhead trailing ATR resistance at the 110.50 level. Momentum is almost in the oversold stage signalling more downside so watch for continued overall weakness around USD and further disruptions due to COVID at the Olympics:

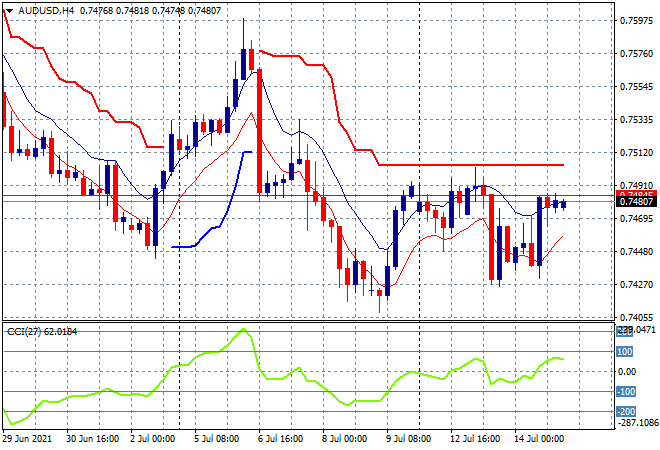

The Australian dollar was initially pushed higher on the Fed inflation comments but sort of got stuck just below steady resistance at the 75 handle, not making a new high where it sits this morning going into the Sydney open. Momentum is back to the positive setting on the four hourly chart but nowhere near overbought as overhead ATR resistance at the 75 level becomes a bridge too far for the Pacific Peso:

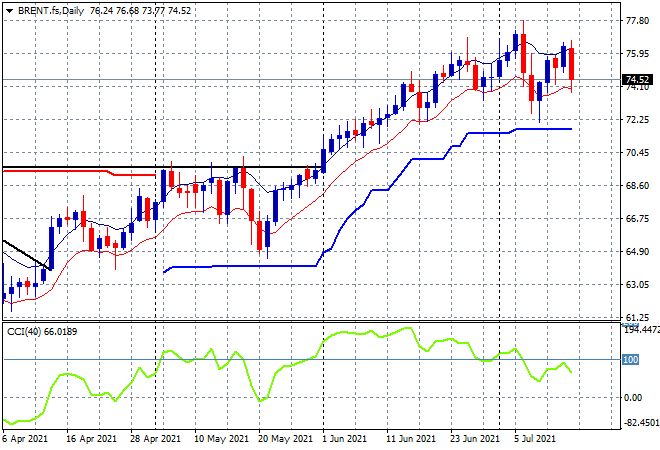

Oil is still struggling to find direction here following last week’s OPEC+ meeting with Brent crude retracing overnight to get back below the $75USD per barrel level after what looked like an eminent breakout. What is required is another move higher to match or surpass the previous highs at the $77USD level but this is not yet eventuating as daily momentum tapers into neutral settings:

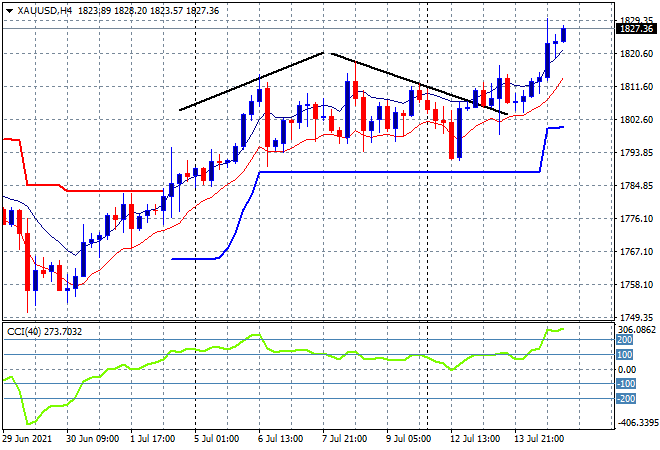

Gold is no longer holding on its breaking out on Powell’s inflation comments with a lovely run up overnight following nearly two weeks of steady buying support above the $1800USD per ounce level, finishing at almost $1830. The clearance of the high moving average and a new weekly high bodes well for the shiny metal going forward:

Glossary of Acronyms and Technical Analysis Terms:

ATR: Average True Range – measures the degree of price volatility averaged over a time period

ATR Support/Resistance: a ratcheting mechanism that follows price below/above a trend, that if breached shows above average volatility

CCI: Commodity Channel Index: a momentum reading that calculates current price away from the statistical mean or “typical” price to indicate overbought (far above the mean) or oversold (far below the mean)

Low/High Moving Average: rolling mean of prices in this case, the low and high for the day/hour which creates a band around the actual price movement

FOMC: Federal Open Market Committee, monthly meeting of Federal Reserve regarding monetary policy (setting interest rates)

DOE: US Department of Energy

Uncle Point: or stop loss point, a level at which you’ve clearly been wrong on your position, so cry uncle and get out!