Friday night’s rally on Wall Street caused Asian stocks to rebound yesterday and overall risk sentiment rised in response overnight with European stocks lifting the most, yet Wall Street still put in another new record high. Treasury yields pushed slightly higher but still remain near their yearly lows while currency markets were relatively quiet given the lack of economic releases. Oil prices moderated while gold whipsawed around the $1800USD per ounce level.

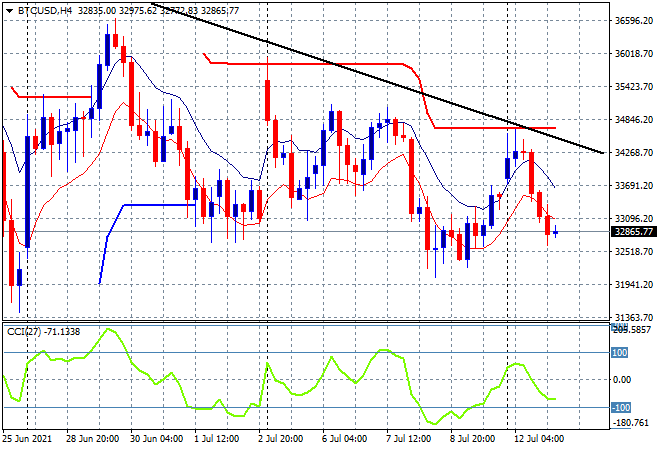

Bitcoin came out of the weekend gap with a bit of gusto but was unable to hold on to any gains, pushed back below the $33K level and almost back to last week’s lows with the daily downtrend line (upper black sloping line) still holding here:

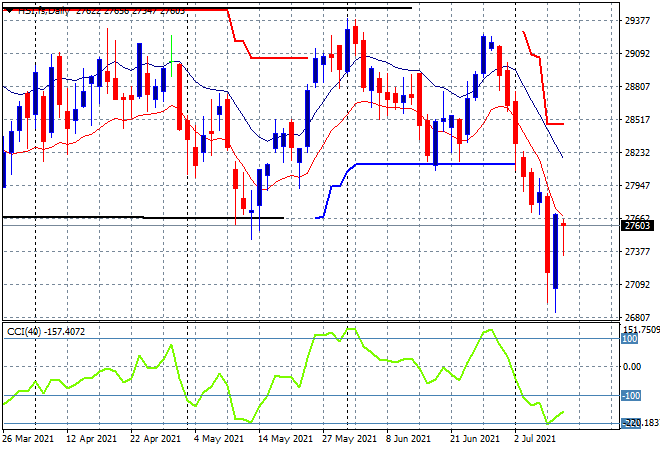

Looking at share markets in Asia from yesterday’s session, where the Shanghai Composite closed 0.7% higher at 3547 points while the Hang Seng Index put on similar gains, up 0.6% to 27515 points. The daily chart shows a possible volatile bottom forming here after breaking down below daily ATR support at the 28100 point level and momentum reverting from very oversold levels, but the picture still remains uncertain until a positive close above the 28000 point level is done:

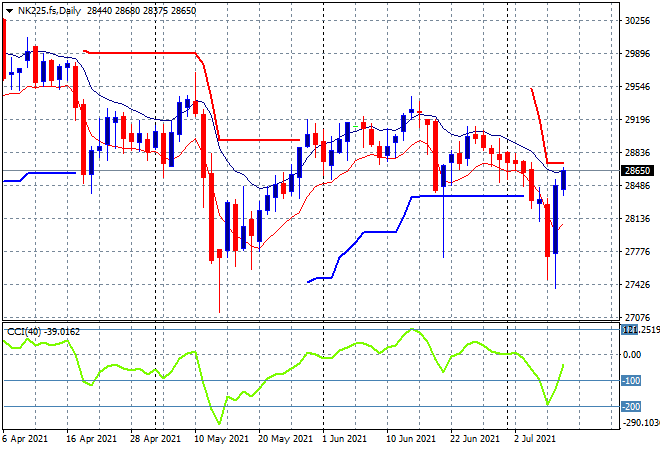

Japanese stocks however surged the strongest with the Nikkei 225 closing over 2% higher to 28569 points. Daily futures are looking good again so we should see a continuation here, albeit with some hesitation because a new trend higher requires at a minimum a new daily high above the high moving average and then clearing substantial resistance at the 29000 point level that has held since May:

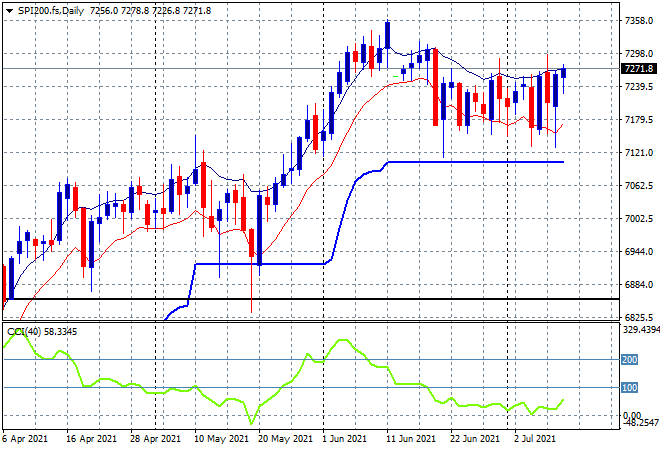

Australian stocks also put on runs but at the same pace as Chinese bourses with the ASX200 closing 0.8% higher as it advances back above the 7300 point level to 7333 points. SPI futures are up slightly this morning so we should see further stabilisation of this sideways trend that has held since early June, with daily momentum still nominally positive and trailing daily ATR support at 7150 points still holding:

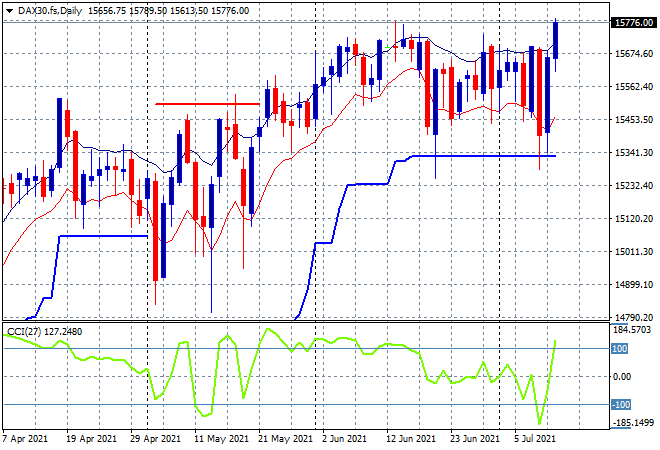

European markets were slightly upbeat, although the FTSE put in a scratch session with the absence of economic news helping smooth volatility. The German DAX lifted 0.6% to close at 15790 points, continuing the bounce off daily ATR support at the 15300 point level. This looks like a potential breakout trade, but I’m sure other traders are looking for a follow through here and keeping stops very loose given the volatility of this sideways march:

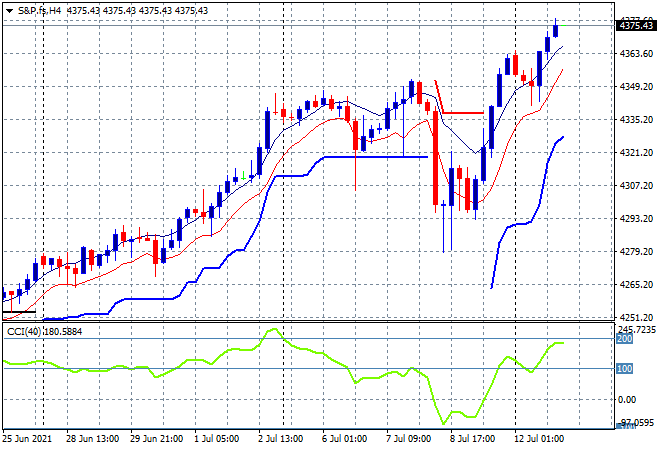

Wall Street had a similar finish, although it ran out of mojo towards the end of the session, with the S&P500 closing 0.3% higher to another new record high at 4384 points. The four hourly chart shows a market still fully engaged and ready to go higher with momentum remaining well into an overbought status and price holding well above trailing ATR support – what could go wrong from here:

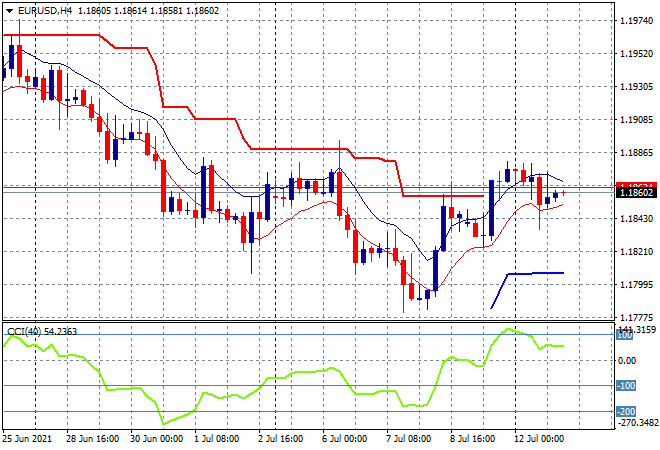

Currency markets were relatively sanguine overnight due to a lack of economic releases so it was bots fighting bots as USD remained a little weak against the majors. Euro tried to extend its Friday night highs but was unable to lift above the 1.1870 level with a possible reweighting slowly evaporating. While the trailing ATR resistance levels have now been broken and momentum is nominally positive on the four hourly and daily charts this is not yet suggesting more upside:

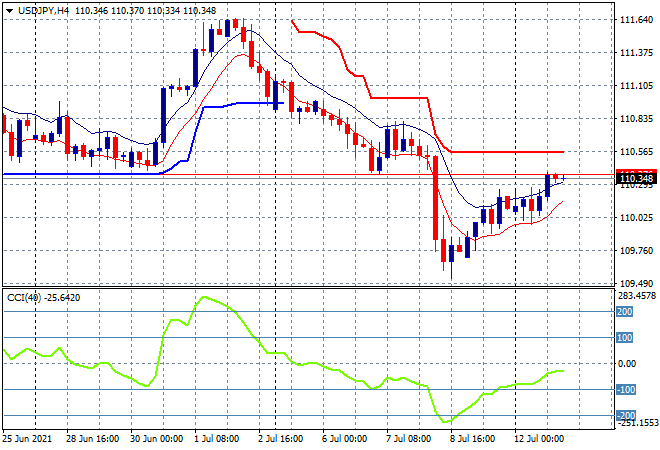

The USDJPY pair is continuing its slight reweighting after last week’s Yen safe haven buying in the wake of the COVID crisis around the Tokyo Olympics with a continued bounceback above the 110 handle overnight. This still suggest a long swing position only so far with momentum still nominally negative and price well below trailing ATR resistance overhead at the 110.50 level but something could be brewing to turn this into a breakout:

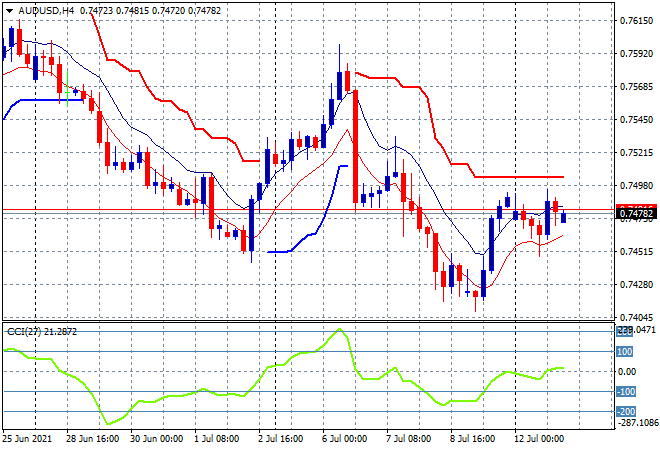

The Australian dollar had a small whipsaw overnight as that swing only buy pattern remaining in play as price is still unable to break back above the 75 handle. Momentum is back to the neutral positive setting but overhead ATR resistance at the 75 level is the key area to watch this week to see if the Pacific Peso can get out of its funk:

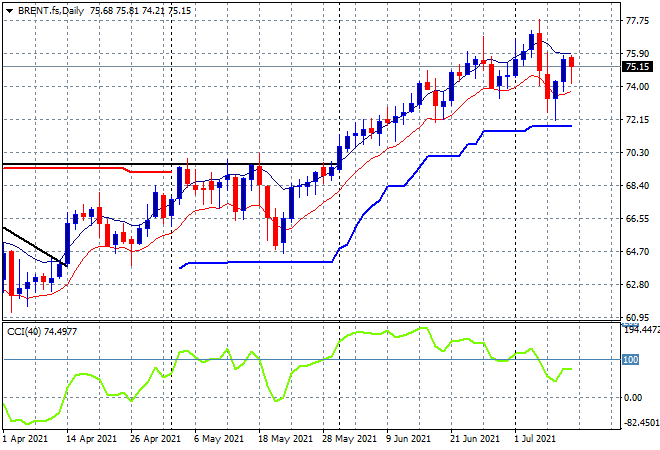

Oil is still a little listless following the OPEC+ meeting with Brent crude retracing slightly to start the week with a whimper after the near 2% lift on Friday night to remain just above the $75USD per barrel level. While price remains strongly supported in this uptrend, the move down to trailing ATR support at $72 may not yet be over, with volatility to rule here still. Watch for a new daily high above the high moving average as a clearer buy signal:

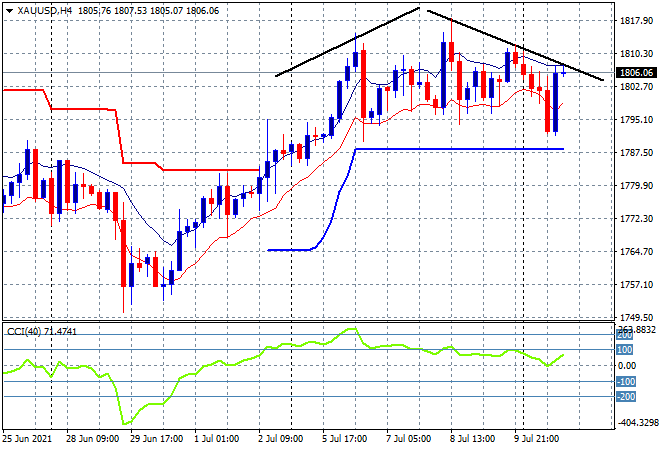

Gold is holding on after a less than steady start to the week, eventually finding more buying support at the $1800USD per ounce level to get back above overnight after a quick trip below. This still doesn’t clear the rounding top pattern here on the four hourly chart and requires a higher close above the high moving average or short term resistance will way against the shiny metal and send it back down to the $1790 ATR support level quickly:

Glossary of Acronyms and Technical Analysis Terms:

ATR: Average True Range – measures the degree of price volatility averaged over a time period

ATR Support/Resistance: a ratcheting mechanism that follows price below/above a trend, that if breached shows above average volatility

CCI: Commodity Channel Index: a momentum reading that calculates current price away from the statistical mean or “typical” price to indicate overbought (far above the mean) or oversold (far below the mean)

Low/High Moving Average: rolling mean of prices in this case, the low and high for the day/hour which creates a band around the actual price movement

FOMC: Federal Open Market Committee, monthly meeting of Federal Reserve regarding monetary policy (setting interest rates)

DOE: US Department of Energy

Uncle Point: or stop loss point, a level at which you’ve clearly been wrong on your position, so cry uncle and get out!