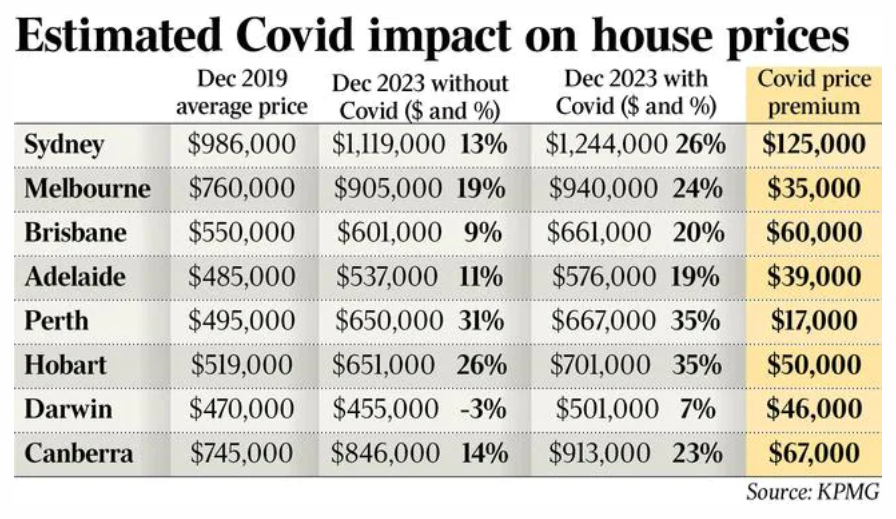

Modelling by KPMG shows that house buyers across Australia are now paying a ‘Covid premium’.

This premium will increase the average price of a house in Sydney by about $125,000 by December 2023, to $1.24 million.

By contrast, the average house would have been around $1.12 million at the end of 2023 if the COVID-19 pandemic had not occurred.

KPMG’s analysis also suggests that the COVID premium for house buyers in Melbourne will be restricted to about $35,000 due to factors such as Melbourne’s extended lockdown in 2020 and the growing number of residents who are moving interstate or to regional areas.

“House prices were ready to jump prior to Covid, particularly in Sydney, where prices were below their long-run trend,” Dr Rynne said.

But the Reserve Bank’s massive easing of monetary policy settings – including slashing the cash rate target from 0.75 per cent leading into the health crisis to 0.1 per cent, and pumping nearly $190bn of virtually free money into the banks – had “turbocharged house prices over and above what they would have been were it not for Covid”.

The sharp fall in borrowing costs – particularly in fixed mortgage rates, which in some cases fell below 2 per cent – “swamped” the negative effect of stagnant population growth as the economic recovery gathered steam, Dr Rynne said.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.