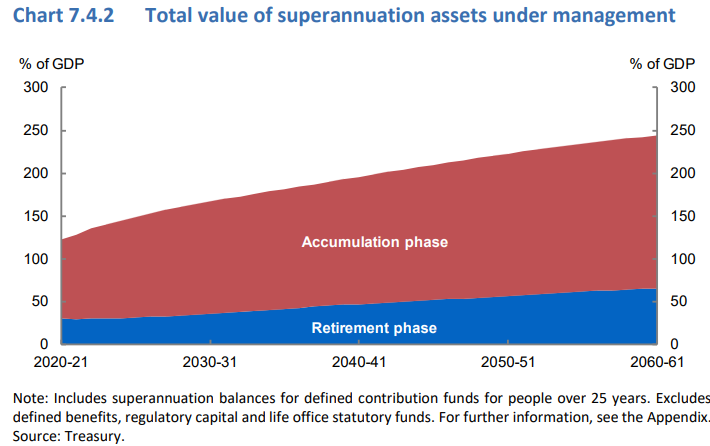

Treasury’s Intergenerational Report showed that superannuation funds under management will soar from around 157% of GDP currently to a projected 244% of GDP by 30 June 2061:

As at 31 March 2021 the superannuation system had assets under management valued around 157 per cent of GDP.80 It is projected this will grow to around 244 per cent of GDP by 30 June 2061. Of this amount, it is estimated that almost three-quarters of funds under management will be held in the accumulation phase.

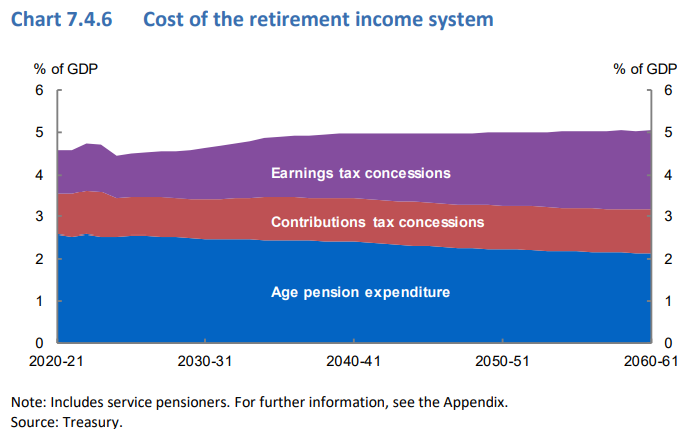

The IGR also showed that the cost of superannuation concessions will over take the cost of providing the aged pension:

The total projected cost of Age Pension expenditure and superannuation tax concessions together is expected to increase from around 4.5 per cent of GDP in 2020-21 to 5.0 per cent of GDP in 2060-61. As a result of the maturing of the superannuation system, government spending on the Age Pension is projected to decline as a proportion of GDP but the cost of superannuation tax concessions is projected to grow. By around 2040, the cost of superannuation tax concessions will exceed the cost of Age Pension expenditure.

Advertisement

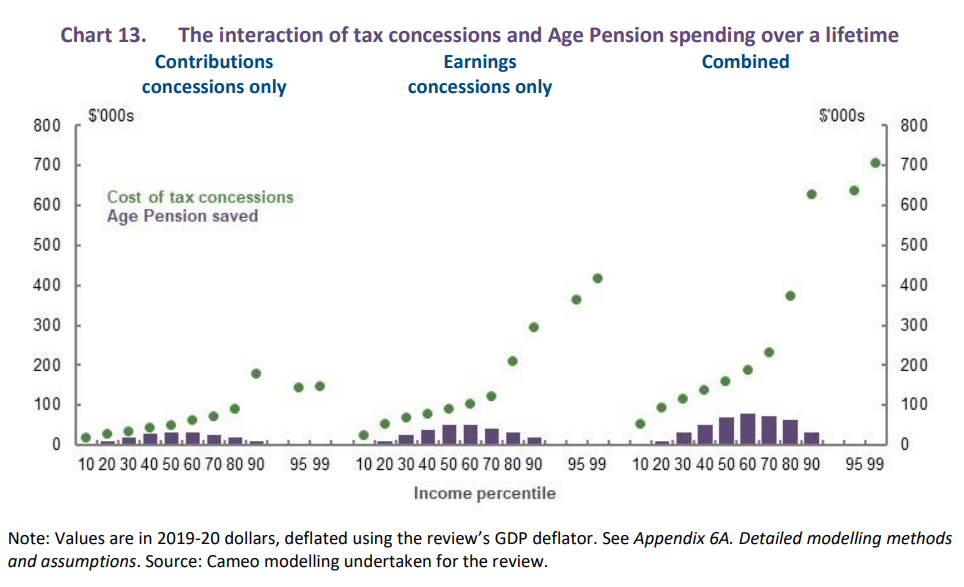

Meanwhile, Treasury’s Retirement Income Review, released last year, estimated that the superannuation system will cost taxpayers more in net terms over the long-run, that is after taking account savings in Aged Pension costs. The Retirement Income Review also showed that superannuation concessions are poorly targeted to high income earners, thereby increasing inequality:

To the extent that superannuation tax concessions are contributing to higher superannuation balances of lower- to middle- income earners, they help to reduce Age Pension expenditure. But the main influence behind the growth in superannuation balances is the SG. Tax concessions are largely concentrated among higher-income earners who are close to and above preservation age. Across the income distribution, the lifetime cost of superannuation tax concessions is projected to outweigh the associated Age Pension saving (Chart 13)…

Therefore, the biggest winners from Australia’s superannuation system are the funds themselves, which will get to glean fatter fees from the strong growth in funds under management.

Advertisement

Lifting the superannuation guarantee to 12% will succeed in feathering funds’ nests even further.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.