CPI in detail: No smoking gun to lift rates

Advertisement

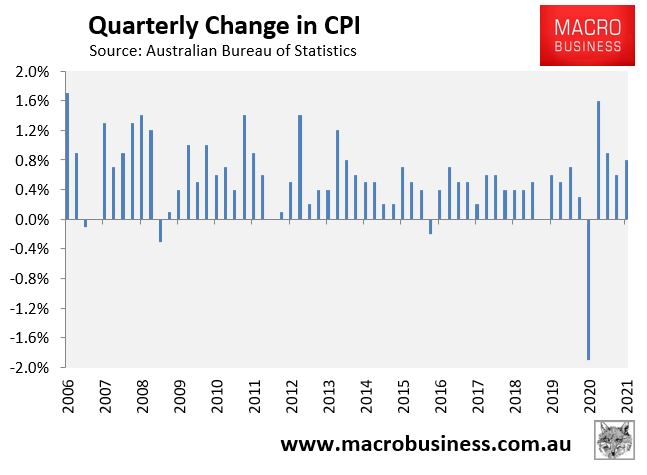

As noted earlier, Australia’s Consumer Price Index (CPI) came in at 0.8% in the June quarter – slightly above market expectations of a 0.7% rise:

Rebounding after last June’s heavy fall.

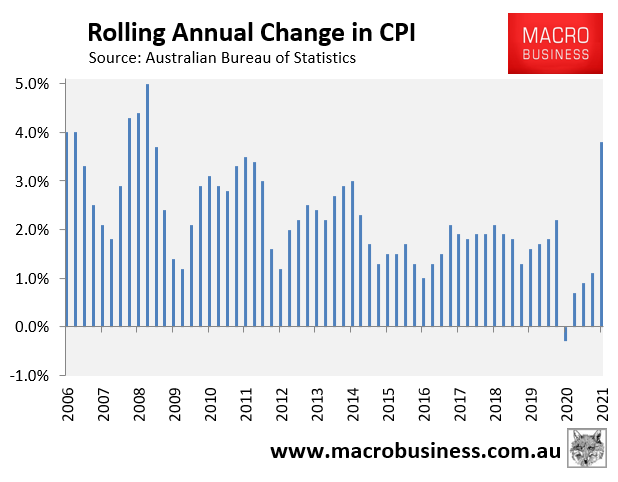

Annual CPI surged 3.8% in Q2. However, this rise was driven by the ‘base effect’, since CPI fell by 3.7% in the corresponding Q2 quarter of 2020 (as shown above).

The full text of this article is available to MacroBusiness subscribers

Cancel at any time through our billing provider, Stripe

About the author

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.