I recently picked the near top of the CBA bubble to start throwing pins. Since I began I first raised the notion that CBA is a preposterous bubble, it has deflated by 10%, more than its banking peers:

Yet CBA remains stupidly overvalued. It is virtually no different to the other big three. Its yield is materially lower. And it’s assets nothing like worth double other banks.

As well, the global bond curve has rolled over as the great liquidity withdrawal gets underway for both fiscal and monetary authorities:

A flattening yield curve is bad for banks everywhere. CBA’s armies of yield-starved retail can’t keep afloat forever:

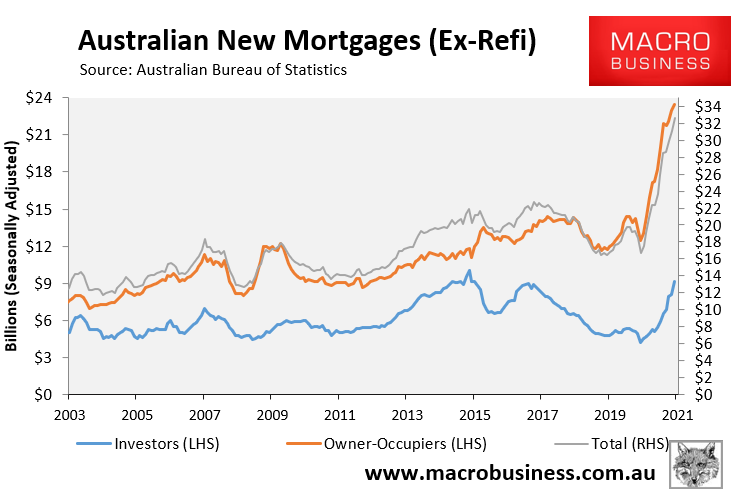

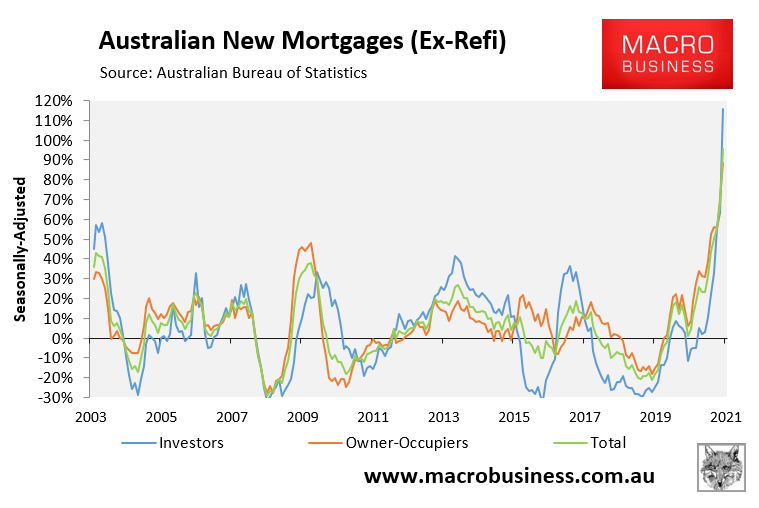

Especially as macroprudential tightening begins soon as investor loans run out of control:

The final giveaway is the stamp of approval from bubble blower, Goldman Sachs:

“If the current Jun-21 quarter approvals’ momentum can be maintained and amortisation remains in line with our forecasts to move higher, we would see about 1% upside to our credit growth forecasts over the course of the next 12 months. Every 1% increase in domestic mortgage credit growth adds about 1% to sector earnings, with BEN (72% of 2H20 total loans), BOQ (66%) and WBC (63%) having the highest exposure of the six listed retail banks.”

Except that the current pace of lending is already surpassing the speed limits that have previously triggered macroprudential and when that happened, banks sank.