By Gareth Aird, head of Australian economics at CBA

Key Points

- At the July Board meeting the RBA will announce a decision on yield curve control and the bond buying program.

- We expect the RBA to maintain the April 24 bond as the target bond for yield curve control (i.e. not shift to the Nov 24 bond).

- We expect the RBA to announce that it will taper its bond buying program when the second $A100bn of bond purchases is completed in early September.

- We have pencilled in an announcement of a further $A50bn of bond buying over six months, but there is considerable uncertainty over this and the RBA may adopt a more flexible approach to tapering.

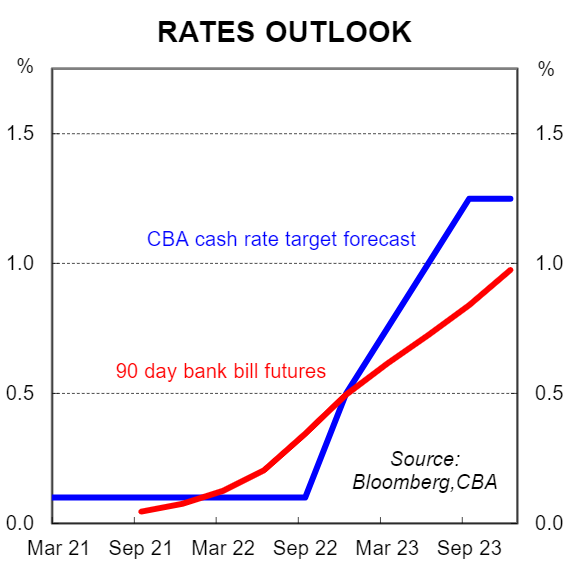

- We expect the RBA to begin normalising monetary policy in late 2022 and see the cash rate target at 0.5% at end‑2022 and then peaking at 1.25% by Q3 2023.

Overview

6 July 2021 has been on the radar of financial market participants since 4 May 2021 when RBA Governor Lowe announced that at the July Board meeting a decision would be made on yield curve control (YCC) and the bond buying program (also known as quantitative easing or QE).

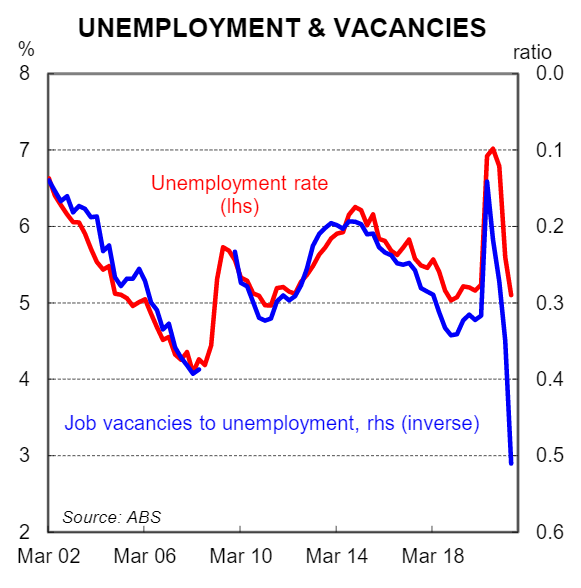

When this announcement was made the Governor would not have envisaged that on the day of the July Board meeting Greater Sydney would be in the midst of a snap two week lockdown. By the same token, the Governor would not have expected the unemployment rate to have dropped to 5.1% in May and for the underutilisation rate to be at its lowest level since early 2013. The Governor is also likely to be shocked at the explosion in job vacancies which have continued to rise as the number of people unemployed has fallen. Indeed the job vacancies to unemployment ratio is consistent with an unemployment rate of around 3.0%! (see chart).

The dichotomy of the strength of the domestic economic data against the backdrop of recent lockdowns across the country creates an unusual dynamic for the July Board meeting. The economic data is evidence that the labour market has tightened quickly which means we are closer to full employment at this juncture than the RBA expected. But the lockdowns are a reminder that we are not out of the pandemic yet.

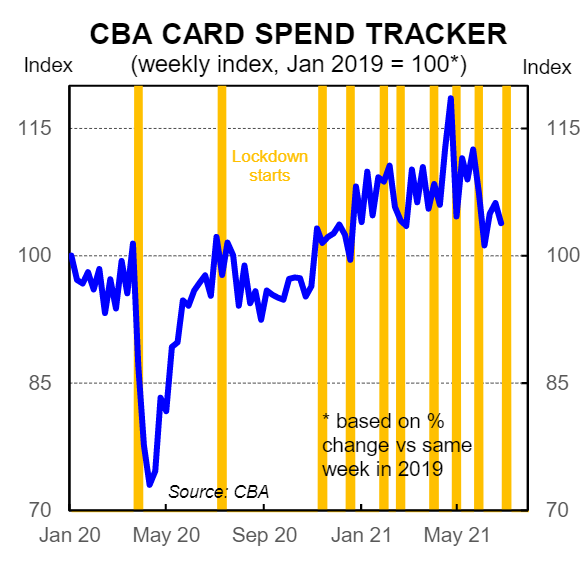

We think the economic data is the more powerful force given the transitory nature of lockdowns and the success Australia has had to date in managing community transmission of COVID‑19. In addition the evidence indicates that spending rebounds quickly post lockdowns.

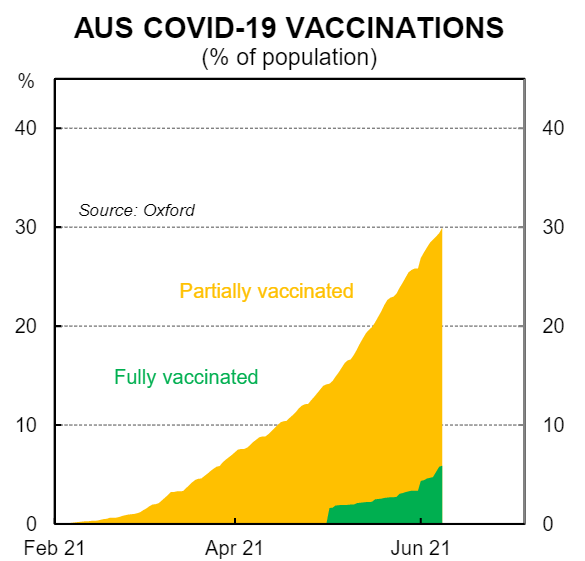

The latest lockdowns are definitely a setback. But the silver lining is that they have accelerated the vaccine rollout. The RBA will be cognisant of both the shift in speed and the sense of urgency now around the vaccine rollout. Put simply, the faster the vaccine is rolled out the sooner the economy will have clear air from COVID‑related distributions.

The yield curve control (YCC) decision looks a done deal

CBA expects the RBA to maintain the April 24 bond as the target bond for YCC (i.e. not shift to the Nov 24 bond) at the current rate of 0.1%. We have held this view ever since the Governor stated in March that the Board would only consider whether to maintain the April 24 bond as the target bond or shift the focus of the yield target to the Nov 24 bond (previously we expected the RBA to abandon YCC around the middle of this year).

We have high conviction on our YCC call because we do not think the RBA can credibly signal that the cash rate will remain on hold until at least November 2024, which is what targeting the Nov 24 bond at 0.1% would imply. Market pricing agrees with us given the yield on the Nov 24 bond is currently 0.42%. We believe the risk of the RBA rolling the yield curve target to the Nov 24 bond is very low.

Tapering is not tightening

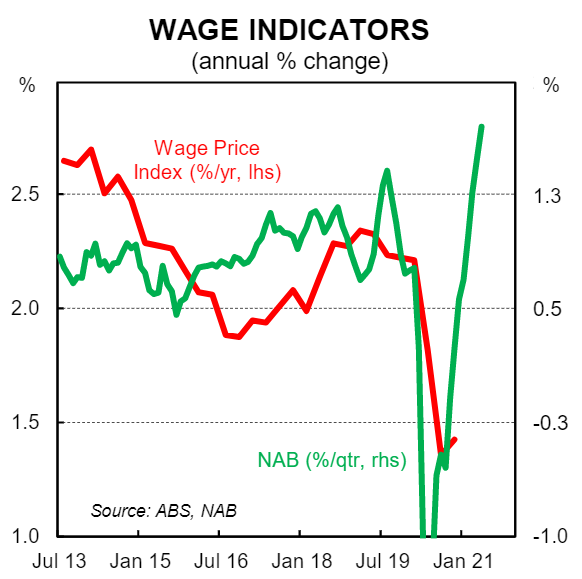

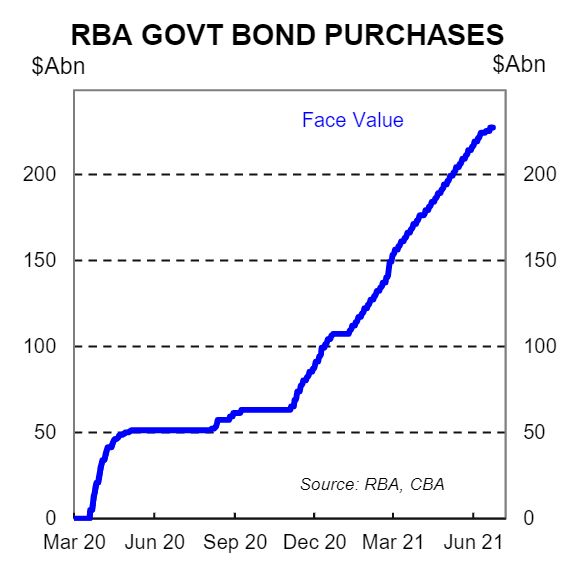

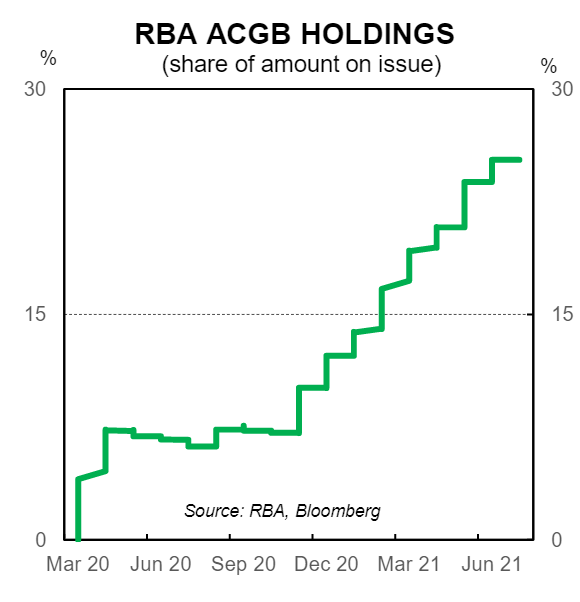

The RBA Governor and the Board want to see inflation return sustainably to the 2‑3% target, which means annual wages growth needs to step up to around 3%. We are still some way from that occurring, which supports a further expansion of the bond buying program. But we are much closer to full employment than we were when the RBA announced its first and second packages of QE in November 2020 and February 2021 (both packages comprised $A100bn of bonds purchased at a rate of ~$A5bn a week for ~6 months). Indeed there is evidence that indicates wages growth has recently lifted given the tightness in the labour market (see below charts).

The question the Board must ask itself is ‑ “from September onwards, what pace should the RBA continue to expand its balance sheet?” ‑ bearing in mind we have progressed towards full employment at a much quicker rate than the Board expected.

Put another way, the RBA is unlikely to continue to be purchasing bonds at the current $A5bn a week rate all the way up until it meets its full employment objective. Indeed when the economy is at full employment the RBA will, in our view, commence normalising monetary policy by lifting the cash rate target. We expect this point to be November 2022.

The RBA Board must therefore have a roadmap in their mind that involves essentially three steps; (i) tapering the rate of bond buying; (ii) the cessation of bond buying; and (iii) normalising the cash rate. The central bank will not drive the monetary policy car with the pedal to the metal and then suddenly slam on the handbrake when the full employment destination is reached. There must be a glide path that involves tapering the rate of bond purchases and we believe we are at that point now.

Here we need to emphasise that tapering the rate of bond purchases, which means expanding the balance sheet through bond buying at a slower pace, does not constitute a tightening in monetary policy – it is just easing at a slower pace. This is a critical point. Former US Fed Chair Ben Bernanke was very forthright about this in 2013 when he stressed to market participants that putting the brakes on the pace of bond buying was not a tightening in monetary policy. It may be the case that RBA Governor Lowe uses his press conference scheduled at 4pm on the day of the Board meeting to make this point if the RBA tapers, as we expect.

What might a taper look like?

The RBA Board will consider three different options for more bond buying at the July Board meeting:

- (i) repeating $A100bn of purchases for another 6 months;

- (ii) scaling back the amount of bonds purchased or spreading the purchases over a longer period; and

- (iii) moving to an approach where the pace of the bond purchases is reviewed more frequently, based on the flow of data and the economic outlook.

Option two constitutes a taper and aligns with our central scenario – that the RBA announces a further $A50bn over six months which implies buying bonds at a pace of around $A2.5bn a month.

Option three, which could best described as a more flexible approach to bond buying, has gained favour with a number of market participants and commentators (note that the bond buying program already has a fair degree of inbuilt flexibility).

Ultimately the added explicit flexibility from option three is more around the flexibility to do ‘less’ and not ‘more’ bond buying. Such an approach could be to announce an intention to buy “up to $Axbn a week in bonds over y months and then reassess” – e.g. “up to $A4bn a week over three months and then reassess”.

Such an approach would allow the RBA to calibrate the bond buying program more frequently based on the economic data. We are very much open‑minded to the RBA taking this approach and on balance it looks to us like a coin toss between options two and three. We have simply gone with option two as our central scenario as it is the approach the RBA has taken to date on QE. In the event that the Board chooses option three we still expect the pace of buying to slow after the current phase of QE ends in September (i.e. they will not continue buying bonds at a pace of $A5bn a week).

Our working assumption is that the RBA maintains the current 80:20 split between Commonwealth and semi government bonds for purchases from September. But as our rates strategists note, there is a risk that the mix of future bond buying is skewed more towards semis.

Look through the semantics

Ultimately we will not be too focussed on the semantics of the bond buying announcement on Tuesday. We are more interested in the modest directional shift we expect the RBA to make. We say “modest” as we still expect the RBA to announce a bond buying program that will be very large in size, particularly relative to the rate of government bond issuance by the AOFM, which has slowed significantly as the economy has improved. And no doubt the RBA will still retain a very dovish tone.

The economy has come a long way since November last year and we believe the RBA will recalibrate its bond buying program at the July Board meeting to reflect that. In doing so the RBA will join a number of other central banks in going down the taper path. The press conference scheduled for 4pm on Tuesday, following the 2.30pm announcement, will be an opportunity for the Governor to fully flesh out the thinking behind the Board’s decision.