By Gareth Aird, head of Australian economics at CBA

Key Points

- The RBA will take a more flexible approach to bond buying (QE) from early September when bond purchases will be at the reduced rate of $A4bn a week until at least mid‑November (as compared with the current pace of $A5bn per week).

- The RBA Board will next review the rate of bond purchases at the November Board meeting.

- We expect the RBA to announce a further taper at the November Board meeting and have pencilled in a rate of bond buying of $A3bn a week from mid‑November 2021 until mid‑February 2022.

- Bond purchases are expected to continue through to May 2022, but at a further reduced rate.

- Total bond purchases from mid‑November 2021 until mid‑May 2022 (i.e QE3) are expected to be a touch under $A100bn.

- Our central scenario remains that the RBA will commence normalising the cash rate in November 2022.

The bond purchase program to be reviewed more frequently

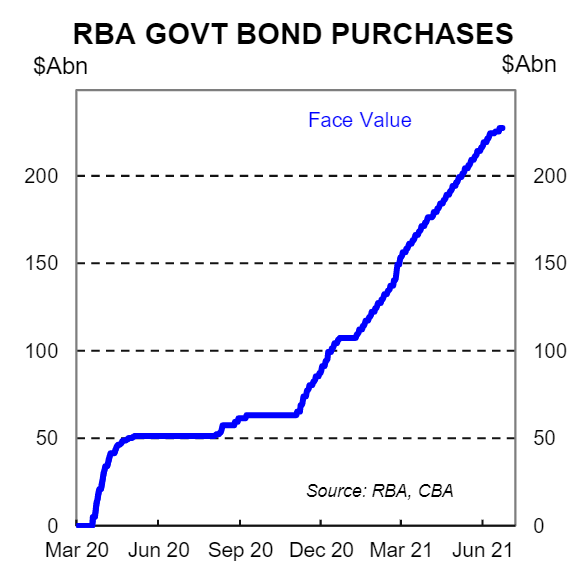

The RBA’s decision from the July Board meeting to extend bond purchases from early September until mid‑November at a reduced rate of $A4bn per week was both a taper as well as a shift to take a more flexible approach to quantitative easing (QE).

CBA expected the RBA to taper bond purchases, but we thought it was a coin‑toss as to whether the taper would involve a more flexible approach to QE. In short, the more flexible approach the RBA has taken simply means committing to purchases for a shorter period of time. Reviewing the bond buying program more frequently will enable the RBA to recalibrate purchases to the flow of economic data and news.

The RBA has committed to next reviewing the bond buying program at the November Board meeting. In other words an announcement will be made on bond purchases on Tuesday 2 November 2021 (Melbourne Cup day).

In his press conference of 6 July RBA Governor Lowe stated, “the reviews of our bond purchases take into account: the effectiveness of the bond purchases to date; the decisions of other central banks; and, most importantly, progress towards our goals for inflation and employment. We will use this same framework in our future reviews.”

It is clear that the RBA considers the bond purchases to date to be effective. Therefore it is the second two points that are worth focusing on when thinking about future RBA decisions around bond buying.

(i) The decision of other central banks

The most important central bank in the world is the US Federal Reserve. By extension, the monetary policy decisions of the US Federal Reserve will have the largest bearing on the monetary policy decisions of the RBA.

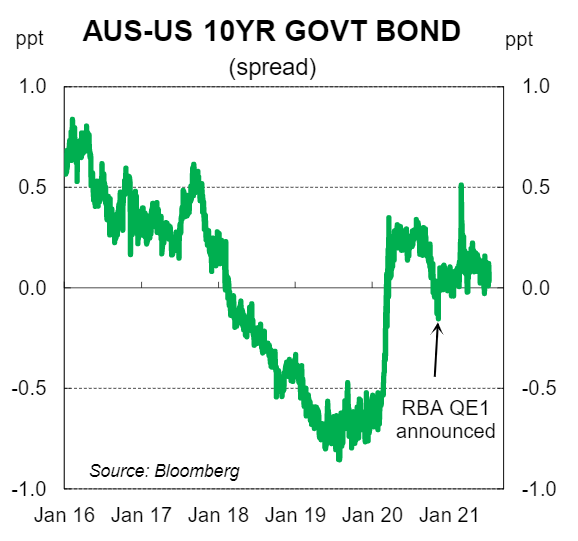

We expect the US FOMC to announce at the September meeting that the Fed will taper its asset purchases from October. This means that when the RBA Board review the bond buying program in November we expect the Fed will by then be buying US Treasuries at a reduced pace. This will provide the RBA scope to further taper without putting upward pressure on the AU/US interest rate differential and by extension the exchange rate.

Of course it is not only the US Fed that matters. We expect a number of other central banks to be taking their foot off the monetary policy accelerator in Q4 21 (notably the Bank of Canada, who have almost finished tapering, and the RBNZ ‑ our colleagues at ASB expect the RBNZ to hike the OCR in November 2021).

(ii) Progress towards the goals of inflation and employment

The November Board meeting is four months away. The recent outbreak of COVID‑19 in Sydney and subsequent lockdown mean there is a considerable degree of uncertainty around the near term economic outlook. Notwithstanding, our working assumption is that the lockdown does not go on for an extended period. Will also expect that economic activity will bounce back quickly once restrictions are eased, as has previously been the case.

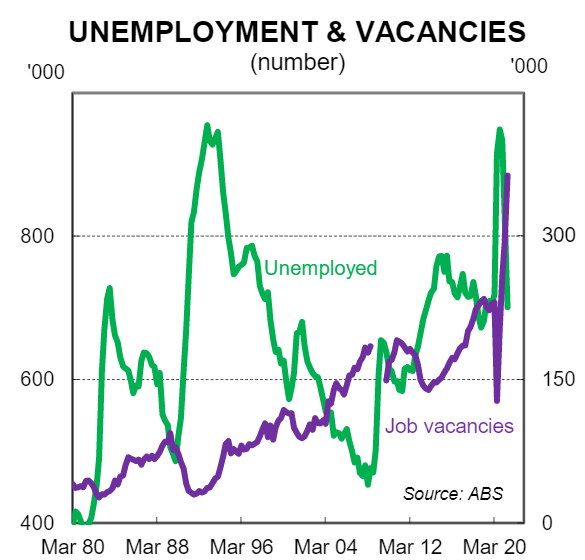

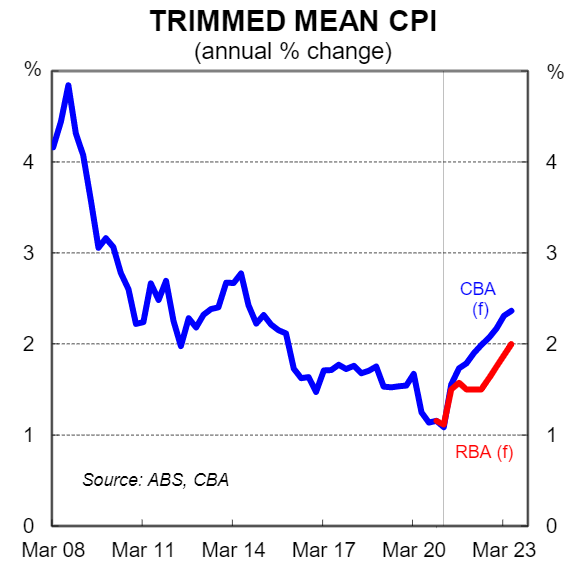

The leading indicators of labour demand are strong and we expect the unemployment rate to have a 4 handle on it at the time of November Board meeting (the September labour force survey will be published on 14 October). We forecast the trimmed mean CPI in Q3 21 to have accelerated to 1.7%/yr.

Put simply, at the time of the November Board meeting both the inflation and employment data is expected to show that progress has been made towards the goals of inflation and employment.

Our profile for the bond buying program

The RBA has committed to buying bonds from early September until mid‑November at a reduced pace of $4bn a week. This equates to $A40bn of QE over that period.

Our base case sees the RBA announce a further tapering of the bond buying program at the November Board meeting. More specifically we expect the RBA to announce they will buy $A3bn of bonds per week from mid‑November to mid‑February 2022, with a three week pause over the Christmas/New Year holiday period. This equates to an additional $A30bn of QE.

We expect the RBA to announce at the November Board meeting that they will further review the bond buying program at the February 2022 Board meeting.

Based on our economic forecasts we have pencilled in additional RBA bond buying from mid‑February to mid‑May at a further reduced based of $2bn per week. This equates to an additional $A26bn of QE.

We expect the RBA to announce at the May 2021 Board meeting that they will cease buying bonds from mid‑May. At that point we expect underlying inflation to be 2.0%/yr.

On our profile the RBA will have bought $A96bn of bonds under QE3.

There are of course risks. If lockdowns are ongoing and the economic expansion stalls over the next few months the RBA is likely not to taper again at the November Board meeting. But working the other way is the possibility that the economy is running hot by the early part of 2022 with a full rollout of the vaccine. Such an outcome could mean that the RBA opts to stop expanding the balance sheet earlier than we anticipate.

We will of course update our profile along the way if the data or news on COVID‑19 differs from our central scenario.

RBA to hike the cash rate in November 2022

Our profile on the cash rate target is unchanged. We expect the RBA to begin normalising monetary policy in late 2022. Picking the exact meeting that the RBA first hikes the cash rate is in many respects false precision. But our central scenario has the RBA delivering a first hike in the cash rate target in November 2022 ,ie. from 0.1% to 0.25%. We see the cash rate target at 0.5% at end‑2022 and then peaking at 1.25% by Q3 2023, the level which we asses to be neutral.

Our profile for the cash rate means that we expect the RBA to exit yield curve control before November 2022 – potentially in H1 2022 at the May Board meeting depending on the flow of economic data.

By mid‑2022 there is likely to be a euphoric mood amongst consumers and businesses as COVID‑related disruptions to day to day life are a thing of the past. We expect the Australian economy to be running at maximum capacity provided the Government has not shifted strategy to tighten fiscal policy. In summary, our forecasts for wages growth and inflation meet the conditions for a rate hike in late‑2022.