Some more volatility in forex markets overnight as the forgotten US inflation surge tore a hole in the sky. DXY hit new highs and EUR was belted:

Australian dollar was hammered but held above previous lows:

Gold and oil were firm despite DXY:

Advertisement

Not so the rest of the commodities complex:

Junk fell but is not yet alarming:

Yields jackknifed but not enough to break the flattenign trend:

Advertisement

Stocks struggled:

Westpac has the wrap:

Advertisement

Event Wrap

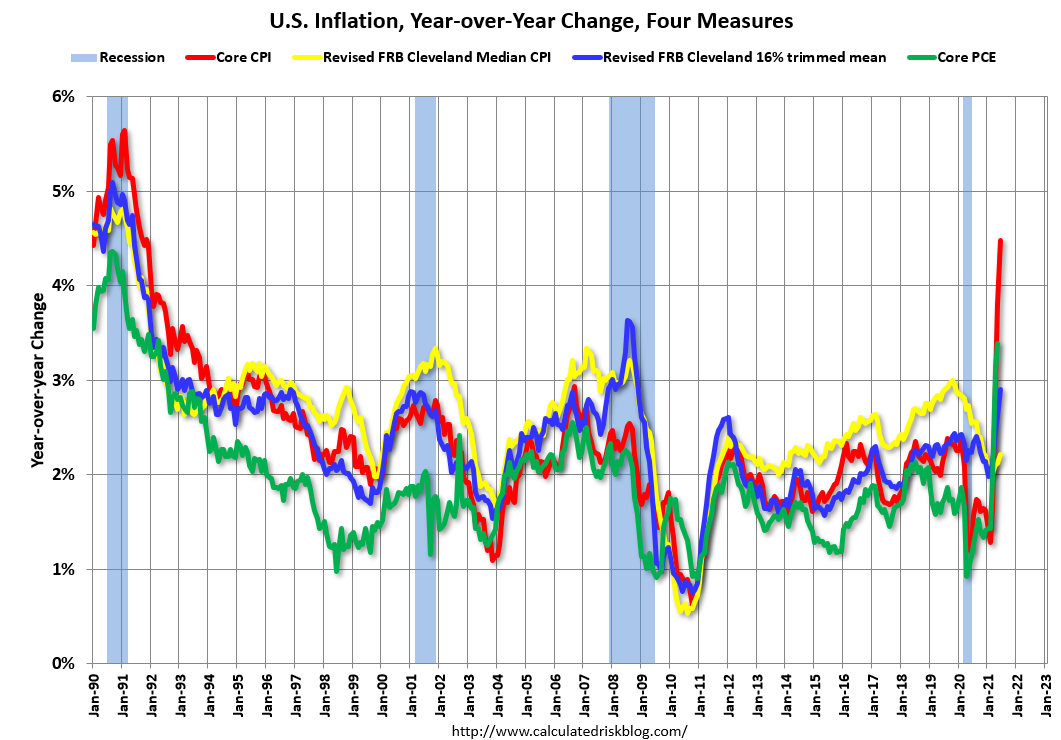

US CPI was stronger than expected, in both the headline and core measures. It rose 0.9% in June (vs 0.5% expected, 0.6% prior), for a 5.4% annual pace – the highest since 2008. The ex-food and energy measure rose 0.9% m/m, 4.5% y/y – the highest since 1991. Many components rose significantly (energy, transportation, vehicles, housing, services, apparel, and food and beverage notable), while medical care was the notable decliner.

NFIB small business optimism survey rose 2.9% to 102.5 in June (99.5 expected, 99.6 prior). Gains were led by “plans to increase inventory” and “expectations for a better economy”. The percentage of owners raising selling prices rose to 47% (40% prior) – the highest since 1981.

Event Outlook

Australia: COVID disruptions are set to feature heavily in the July update of Westpac-MI Consumer Sentiment. While Melbourne has emerged from its June restrictions, Sydney entered an extended lockdown in late June that remains firmly in place, with Brisbane, Perth and Darwin all seeing brief ‘mini-lockdowns’ that have now lifted. Other factors – booming housing and equity markets, a labour market in good shape – will be supportive but COVID developments are likely to dominate.

New Zealand: There will be no new published forecasts at the RBNZ’s monetary policy review. However, the forward guidance in the press release (which previously signalled that current levels of stimulus will remain in place for a ‘considerable’ time) is likely to be altered. The RBNZ is likely to start setting the scene for a normalisation of monetary policy, without committing to a particular timing. We have brought forward our forecast for rate hikes, and now expect the first OCR increase in November 2021 (previously August 2022). May net migration will provide data on the first full month of the trans-Tasman bubble.

UK: The June CPI is set for a 0.2%mth (2.3%yr) print, with strength led by the “reopening” categories.

Euro Area: May industrial production is expected to dip 0.2%, likely a function of supply constraints.

US: The Federal Reserve will release its Beige Book, providing an update on conditions across the Fed districts. The June PPI should advance 0.6% in June, but annual price pressures are likely cresting in annual terms. The FOMC’s Kashkari will speak, and Fed Chair Powell will give his semi-annual testimony to the House Financial Services Committee.

Here’s the US inflation pop:

The Consumer Price Index for All Urban Consumers (CPI-U) increased 0.9 percent in June on a seasonally adjusted basis after rising 0.6 percent in May, the U.S. Bureau of Labor Statistics reported today. This was the largest 1-month change since June 2008 when the index rose 1.0 percent. Over the last 12 months, the all items index increased 5.4 percent before seasonal adjustment; this was the largest 12-month increase since a 5.4-percent increase for the period ending August 2008.

The internals are lot less scary. Much of it is still catch-up prices or one-offs. BofA:

Used cars and trucks“exploded” for another 10.5% mom, while new cars also rose an impressive 2.0% mom. Travel related components also saw outsized strength with lodging away from home spiking 7.0% mom and airline fares rising 2.7% mom. The latter supported a broader transportation services gain of 1.5% mom, which was also boosted by a 5.2% jump in car & truck rentals and a 1.2% rise in auto insurance. Stickier OER stayed hot, rising 0.32% mom, with rent of primary residence somewhat lower at a still solid 0.23% mom. The OER pickup puts it back near the top of the range seen in th last business cycle. Bottom line: transitory drivers continue to boost core CPI by unprecedented numbers, while persistent inflation is also strengthening.

On a contribution basis, new cars added 9bp to core CPI, used cars added 42bp, lodging added 9bp and transportation services added 10bp. Putting it all together, these components contributed 70bp to core CPI this month. As such, the rest of core accounted for 18bp, which in normal times would be a relatively healthy increase in prices. In other words, even without all the transitory strength, other components of inflation were solid—the aforementioned OER pickup likely being the primary driver.

To what extent will we continue to see transitory strength in core CPI? Lodging away from home is now 2% higher than Feb 2020 levels, which could mean much more limited upside going forward. Meanwhile, airline fares still have scope to rise as they remain 9.5% below pre-pandemic levels.

On used cars, the ytd increase for CPI is now at 29%, which is now greater than the ytd increase in Manheim wholesale prices which were up 26% at its high in May and moderated to 24% in June. As such, we believe this may be the end of used car prices trength in CPI, versus our previous belief that it could materialize over the next few months as retail lags wholesale. To the extent that wholesale prices continue to head lower, then the near term risks of a negative payback in used cars grow, which could lead to more depressed core inflation prints. This morning we published a note: Reaching the inflation mountaintop, which explores negative payback scenarios for core goods as well as auto-shortage related components and their potential impact to broader core inflation. We estimate that these scenarios could lead to substantial transitory disinflation over the next year that could bring broader core inflation below target, despite improving persistent inflation.

We don’t believe this report changes much for the Fed. Transitory price pressures remain rampant in the core inflation data and could be nearing their end, with risk of a negative payback over the next year. Persistent inflation, reflected largely by OER, has improved although it is not signaling troublesome inflation.

Advertisement

Nonetheless, I expect ongoing US fiscal stimulus to give DXY a perpetual inflation and yield advantage much deeper into the cycle driving a DXY bull market. Especially so as China lags and commodities crash under pressure from both fundamental and financial pressure, killing off non-US inflation.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.