Forex markets returned to the theme of slowing growth overnight with AUD a special casualty. DXY was strong and EUR weak:

Australian dollar was creamed on the crosses. The rally in JPY is not growth positive:

Gold is up as real yields fall away while oil was bashed:

Metals lifted on the notion that bad news is good in China. Wrong in my view. Chinese growth is better than expected:

Miners firmed:

EM stocks held:

Junk too:

The curve was poleaxed:

But stocks fell anyway. Perhaps on earnings jitters:

Westpac has the wrap:

Event Wrap

US industrial production rose 0.4% in June (vs est. +0.6%, prior +0.7%). Manufacturing disappointed, with a 0.1% drop after downward revisions, with vehicle sector weakness noted. Utility output and mining rose, as did capacity utilization to a 16-month high of 75.4% from 75.1%.

The NY (Empire) business survey jumped from 17.4 to 43.0 – an all-time high (vs est. 18.0). Producer sentiment has remained strong since March, as vaccines and fiscal stimulus have fuelled household spending, while businesses need to rebuild inventories. The Philadelphia Fed business survey fell from 30.7 to 21.9 (vs est. 28.0). Most components weakened slightly.

Fed Chair Powell repeated his semi-annual testimony, this time to the Senate. He said that inflation is “well above 2%” and that they are uncomfortable with that. But the jump is seen as due to the shock to the system and the reopening in the economy. The challenge is how to react to the pressures. To the extent the strength is “temporary” it would be inappropriate to react to the rise in prices, but to the extent it persists, the FOMC would have to re-evaluate the risks that it could be of a longer duration, and that it could impact inflation expectations, and that’s what they are monitoring.

FOMC member Evans sees QE tapering by year end as possible if things progress as he expects. He expects the unemployment rate to fall to 4.5% by the end of 2021, and looks for a rate hike by early 2024. He has confidence that the surge in inflation will be “transitory” and that a more normal inflation environment will emerge in 2022. He also said the upside potential for inflation is not quite as strong or sustainable as he would like. Bullard said it is time to end emergency measures. While acknowledging some of the price pressures are temporary, he is worried that some of the strength may persist into 2022. Meanwhile, substantial progress has been made on the labour market, although it is not fully healed yet. He does not want any tapering to be on auto-pilot, rather retaining flexibility on purchases.

UK unemployment rate unexpectedly rose to 4.8% in the three months to May (vs est. 4.7%, prior 4.7%), and employment rose 25k (vs est. 91k). The June claimant count rate fell though. Overall, mixed signals for the BoE.

The Bank of England’s Bailey said they won’t rush any rate decision. He admitted that this week’s inflation data was stronger than expected, but said they will go through the evidence to assess to what is underlying and what is transitory.

Event Outlook

New Zealand: We expect Q2 CPI growth of 0.8%, which would see the annual rate rising to 2.9% (well above the RBNZ’s last published forecast). In terms of specifics of the June report, we expect particular strength in food prices (in part due to the recent increase in the minimum wage), higher construction costs and a further rise in used car prices. The June manufacturing PMI is likely to remain strong on robust domestic demand.

Euro Area: The May trade balance is expected to pull back to EUR 8bn, continuing the decline from the peak at the start of the year.

US: University of Michigan Consumer Sentiment is expected to rise to 86.5 in July – sentiment is beginning to gather momentum after initially lagging the broader economic recovery. Business inventories have been choppy over recent months, but should expand 0.4% in May. The market is looking for another contraction, -0.5%, in June retail sales – goods trade remains elevated, but consumption is shifting toward services spending as the economy reopens. Ahead of the May update, total net TIC flows have oscillated on net flows from Asia. The FOMC’s Williams will partake in an event on culture in the workplace.

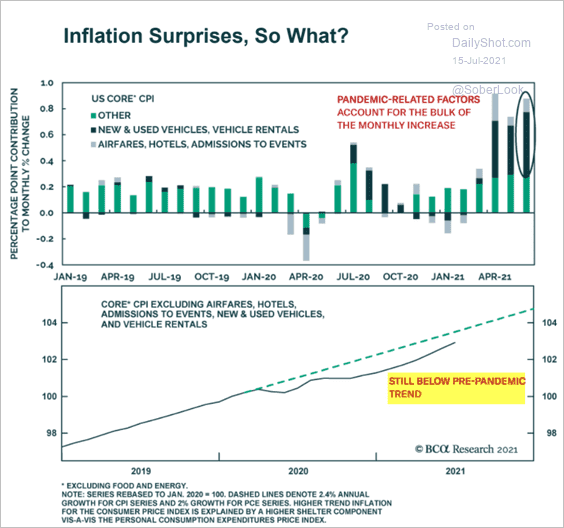

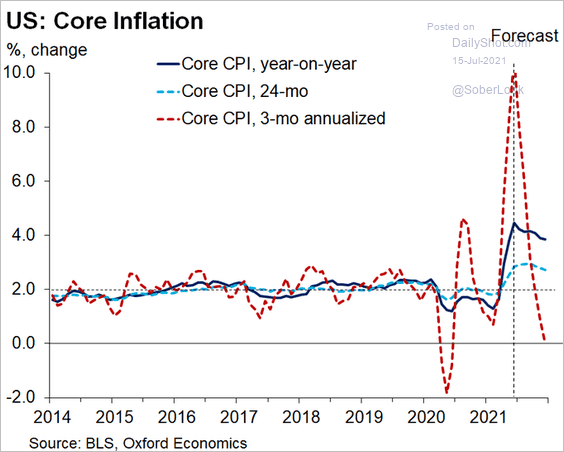

Let’s revisit yesterday’s US inflation number to investigate why the yield curve keeps plunging. It’s all temporary:

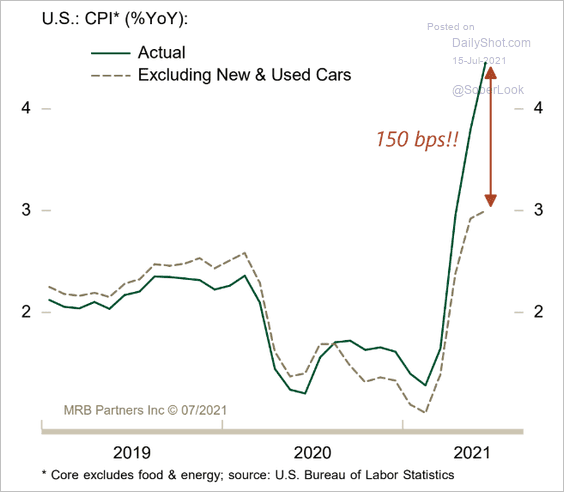

It’s all cars!

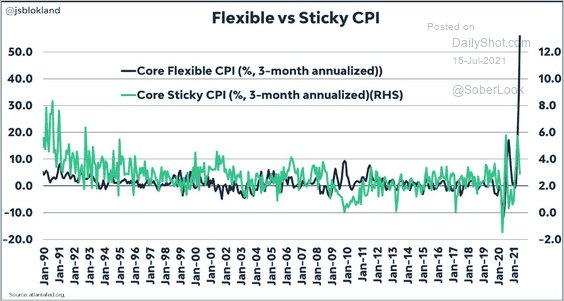

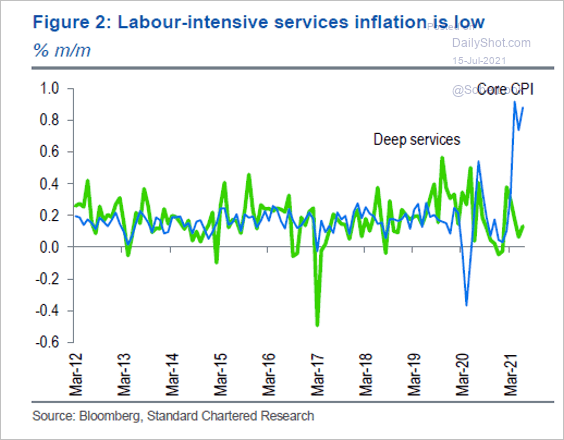

It’s not sticky:

It;s going to collapse:

And there is no wage push inflation cycle in sight:

So, there you have it. While yields keep falling, this regime favours growth over value, staples over cyclicals, bonds over commodities and US over EM forex.

USD over AUD.