Forex was anything but boring last night with China moving to rescue stocks, the Fed delivering outright confusion and markets moving to price more deflation. DXY was hit as the Fed moved more hawkish in its statement then more dovish in its press conference. EUR lifted:

Yet it was still not enough to do anything much for the Australian dollar:

Nor commodities:

Big miners all went a bit silly on RIO’s tiny beat:

EM stocks bounced with the appearance of China’s Plunge Protection Team:

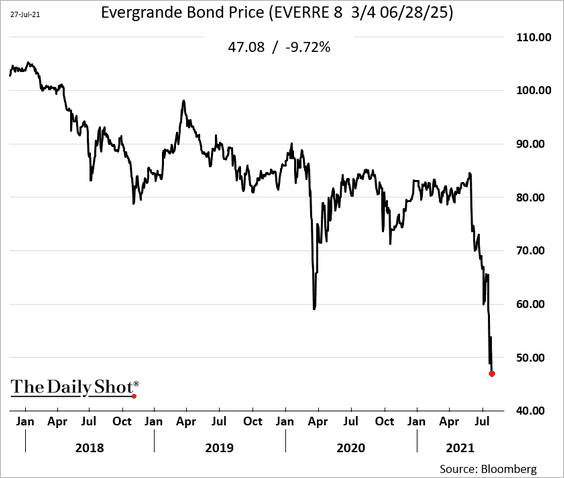

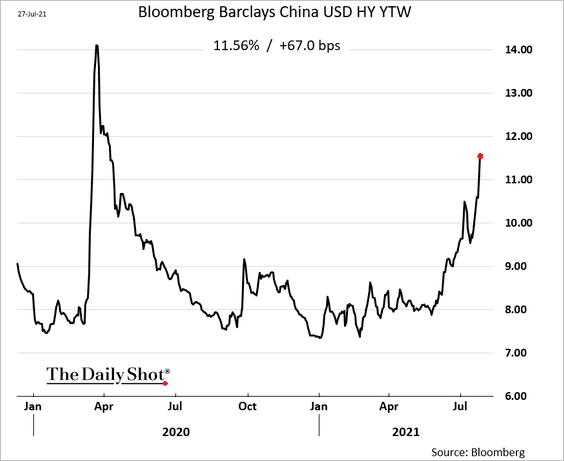

But EM junk is telling a different story. This is all about Chinese tightening and, in particular, Evergrande. Be warned!

The US yield curve was squashed again:

Which lifted growth well over value:

Westpac has the data:

Event Wrap

The FOMC said it “has made progress toward” its goals, and will “will continue to assess progress in coming meetings”, indicating it is moving closer towards tapering bond purchases but is not ready to start yet. The statement noted that the “with progress on vaccinations…indicators of economic activity and employment have continued to strengthen.” On inflation, it reiterated that prices have risen, but are “largely reflecting transitory factors.” Chair Powell, in his press conference, said the labour market “has a ways to go” but also acknowledged that inflation has been hotter than expected and may remain elevated before moderating. Overall, the market was slightly disappointed that there was no strong hint that a tapering decision could be announced at the annual Jackson Hole symposium in August.

Canadian CPI inflation in June slightly softer than expected. Headline CPI fell to 3.1%y/y (est. 3.2%y/y, prior 3.6%y/y), with the core components mixed but close to expectations (common 1.7%y/y, est. 1.9%y/y; median 2.4%y/y, est. 2.3%y/y; trimmed 2.6% as est.).

German GfK consumer confidence was unchanged at -0.3 (est. +1.0). French consumer confidence also missed at 101 (est. 102, prior 103).

UK house price gains showed signs of moderating, with Nationwide’s July survey falling 0.5%m/m (est. +0.3%m/m), pulling the annual pace back to 10.5%y/y (est. 11.9%y/y, prior 13.4%y/y).

Event Outlook

Australia: We are looking for a 1.0% lift in the Q2 import price index on higher energy prices. Meanwhile, the export price index is set to surge 9.0% on sharply higher commodity prices.

New Zealand: We expect to continue seeing an improvement in expectations of own activity in the July ANZBO business confidence survey. This is despite the disruptions we’ve experienced on the Trans–Tasman bubble. Inflation expectations will again be worth watching especially after June’s firm CPI release and given the recent strength in demand.

Euro Area: Ahead of the July update, economic confidence is sitting at a two-decade high (market f/c: 118.4).

US: We are looking for GDP to expand 9.0% annualised in Q2. In the three months to June, the US economy improved materially as the vaccine drive took effect and confidence amongst both households and businesses strengthened. Though consumer spending on goods has topped out, spending on services is on the rise. Housing investment meanwhile has been, and will remain, a significant positive. Investment by the business sector is similarly poised to contribute sustainably. Initial jobless claims are expected to fall to 385k, with last week’s uptick a temporary aberration from an established downtrend. Pending home sales are expected to rise by 0.2% in June, with lower mortgage rates dominating the effect of elevated prices.

Here’s what China did:

China’s securities regulator convened a virtual meeting with executives of major investment banks on Wednesday night, attempting to ease market fears about Beijing’s crackdown on the private education industry.

The hastily arranged call, which included attendees from several major international banks, was led by China Securities Regulatory Commission Vice Chairman Fang Xinghai, people familiar with the matter said, asking not to be named discussing private information. Some bankers left with the message that the education policies were targeted and not intended to hurt companies in other industries, the people said.

This won’t matter because Evergrande is doing this:

In short, the PPT is another of those little attempts to give the falling Chinese aircraft more juice but it is still falling…

In the US, the Fed is setting up for taper:

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. With inflation having run persistently below this longer-run goal, the Committee will aim to achieve inflation moderately above 2 percent for some time so that inflation averages 2 percent over time and longer‑term inflation expectations remain well anchored at 2 percent. The Committee expects to maintain an accommodative stance of monetary policy until these outcomes are achieved. The Committee decided to keep the target range for the federal funds rate at 0 to 1/4 percent and expects it will be appropriate to maintain this target range until labor market conditions have reached levels consistent with the Committee’s assessments of maximum employment and inflation has risen to 2 percent and is on track to moderately exceed 2 percent for some time. Last December, the Committee indicated that it would continue to increase its holdings of Treasury securities by at least $80 billion per month and of agency mortgage‑backed securities by at least $40 billion per month until substantial further progress has been made toward its maximum employment and price stability goals. Since then, the economy has made progress toward these goals, and the Committee will continue to assess progress in coming meetings. These asset purchases help foster smooth market functioning and accommodative financial conditions, thereby supporting the flow of credit to households and businesses.

But poor old Jay Powell is like a cat on a hot tin roof declaring the labour market “has a ways to go”.

Goldman still sees December taper:

We expect labor market progress to accelerate from here, clearing the way for a first hint about tapering in August or September. Fed officials have said that theyintend to signal that tapering is coming “well in advance,” a phrase they alsoused in reference to the start of balance sheet runoff in 2017. That precedent suggests that “well in advance” means two meetings worth of hints before the formal announcement, consistent with our expectation of a first hint in September, a second hint in November, and a formal announcement of taperingin December.

One possible scenario is taper mooted at Jackson Hole in late August then moved forward at subsequent meetings for a December start.

But, by then, unless China has already panicked – and by that, I mean fully reopened the credit throttle to lift its falling economic airplane – a December Fed taper, and the stronger DXY that comes with it, will be about as badly timed as is imaginable because a slowing China and falling CNY will be mid-crash into the entire EM and commodity complex.

In short, our little authorities are furiously working the controls to normalise policy post-COVID but they are on a collision course with the high-flying markets that they created to get through it.

The Australian dollar remains precariously placed.