Forex markets enjoyed a relief rally overnight but not AUD which remains very weak. DXY is still grinding higher too, a warning for every reflationist

The Australian dollar dead cat splattered:

‘

‘ Oil is done. Gold too, in my view:

Metals bounced:

Miners a bit:

EM stocks too:

Junk is still fine. Any decent growth scare requires the opposite:

The curve steepened but it was a bear:

Stocks BTFD!

Westpac has the wrap:

Event Wrap

US housing starts in June rose to 1.643m (est. 1.59m, prior 1.546m), underlining the strength of the market despite rising building costs. Although building permits fell to 1.598m (est. 1.696m, prior 1.683m) – still a historically high level.

Eurozone current account data from the ECB showed a fall in the surplus to EUR11.7bn in May (from EUR22.1bn in April), reflecting known trade data.

Event Outlook

Australia: The June update of the Westpac-MI Leading Index is likely to show a further slowing. It will include some positive component updates: commodity prices continuing to surge strongly (+6.8%mth in AUD terms), the ASX200 posting another solid gain, and US industrial production continuing to lift. Sentiment–related components were also surprisingly resilient in July given rising COVID concerns amid the extended lockdown in Sydney. However, two components saw notable weakness in the month: dwelling approvals, down –7.1% as a massive HomeBuilder driven boost continues to unwind; and total hours worked, which fell –1.8% on a sharp lock–down driven contraction in Victoria.

The full impact of Vic’s restrictions will hit June retail sales. The lockdown in Sydney and another round of mini–lockdowns across multiple jurisdictions (Qld, WA, NT and Vic again) won’t hit until July. Our Westpac Card Tracker suggests sales overall held up reasonably well in June. That said, a sharp contraction in hours worked in Vic points to a material impact on activity. On balance we expect retail sales to show a 0.2% decline (vs market median at -0.7%).

Not much in data to explain the sudden bounce. I put it down to technicals.

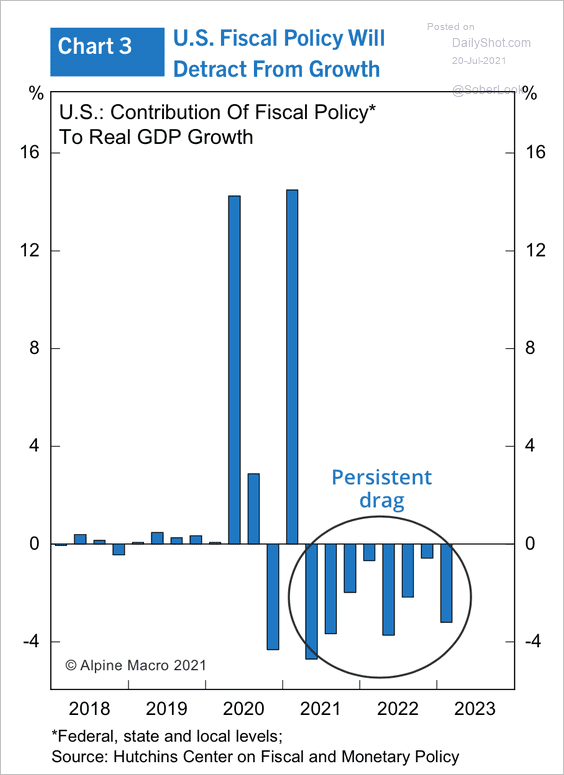

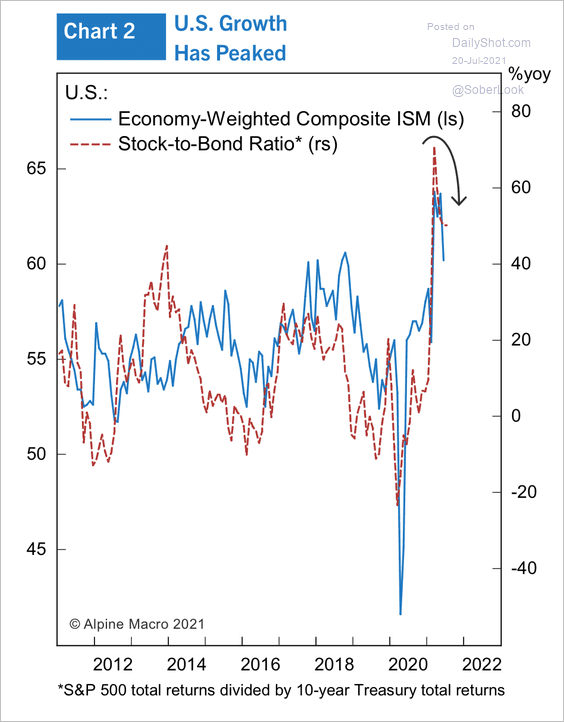

I am still of the view that there is an unusually high-risk case for a growth scare ahead. It is stalking markets as US growth falls off the fiscal cliff:

Materially slowing growth which usually shifts allocations substantially:

Combining with a slowing China and easing inventory cycle to deliver nominal growth and inflation below market expectations.

AUD may get some relief from an improving virus situation in the coming weeks but the broader context remains hostile to a rally.

Hence the failure to bounce with risk.