Forex markets are beginning to show some interesting stress as a developing global slowdown converges with early central bank tightening. DXY still looks poised for higher versus EUR:

Australian dollar was universally weak:

Gold did OK as oil was smashed:

Base metals were hit:

Big miners too:

EM stock were pounded:

And something might be beginning to break in EM HY:

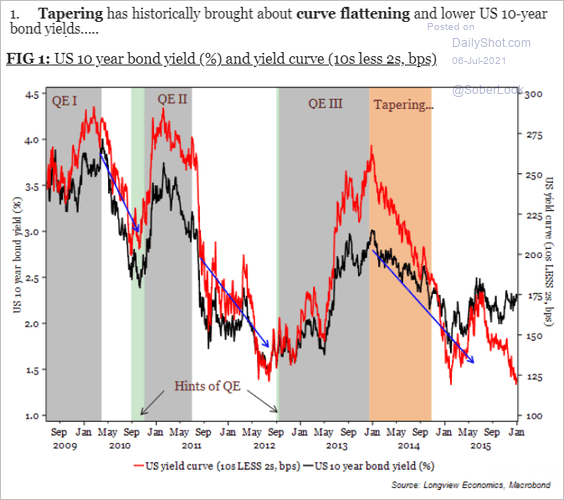

As the US curve was flattened:

Leading to growth outdoing value:

Westpac has the wrap:

Event Wrap

US services ISM survey fell to 60.1 (vs. estimates of 63.5, prior 64.0). Notable declines were seen in new export orders (to 50.7 from 60.0) and employment (to 49.3 from 55.3 in May. While still expansionary, the result was again affected by supply constraints and higher prices. Elevated

Eurozone ZEW surveys disappointed high expectations. Germany expectations fell to a still strong 63.4 (vs. estimate 75.2, prior 79.8), while the current situation rose to +21.9 (est. +5.5, prior -9.1). Eurozone expectations fell to 61.2 (from 81.3) while the current situation rose to +6.0 (from -24.4). Eurozone retail sales in May rose 4.6%m/m and 9.0%y/y (est. 4.3%m/m, 8.2%y/y). German factory orders in May fell 3.7%m/m (est. +0.9%m/m) due to a slump in auto sales.

Event Outlook

China: In recent months, the strength in foreign reserves has been driven by USD weakness; the market is looking for a pullback to $3200bn in June.

US: May JOLTS job openings will point to elevated levels of churn as the labour market heals (market f/c: 9313k). The market will be looking for any guidance on the conditions or nature of tapering in the June FOMC meeting minutes, along with a discussion of the risks to the outlook.

The obvious trigger was the collapse of any OPEC deal. As said yesterday, it made no sense to me that prices were rising. No deal means more oil not less as cheating and possible price war take centre stage. Goldman was late to the party:

- The July OPEC+ meeting never concluded as the UAE and Saudi Arabia/Russiafailed to overcome their differences, with the former asking for a higher baseline from April 2022 and the latter for an extended commitment through 2022.

- While this lack of agreement has introduced uncertainty into the OPEC+production path, our base-case remains for a gradual increase in production through 1Q22 that would ultimately help meet their preferences, with Brent prices at $80/bbl this summer.

- As negotiations continue, we estimate that most outcomes (1) still imply higher prices in coming months as the physical market tightens, (2) with higher OPEC+production than the group discussed needed by the global oil market next year. Price volatility will likely rise, with the release of the August OSP the key next catalyst.

- While the threat of a new OPEC+ price war is no longer negligible, its negativeprice impact would be dampened by a global market starting in a 2.5 mb/d deficitand in need of an extra 5 mb/d in production by year-end to avoid critically low inventories.

Meh. The risk of lower prices is now obvious. That doesn’t mean we get them but the one way bet higher is gone. With Iran also likely about to pump and US shalers ready to go at the first sign of OPEC faltering, yesterday was nasty blow to oil bulls.

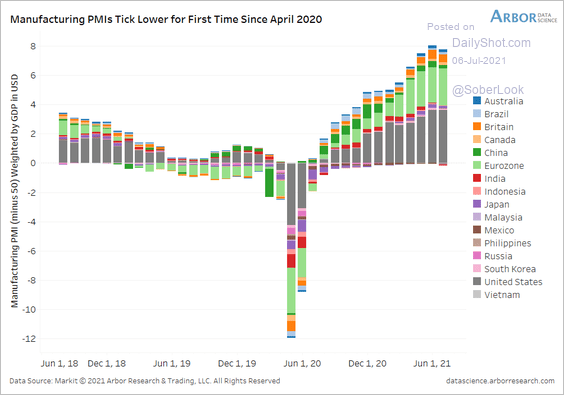

But that’s only the temporal problem. The larger issue is that central banks are on the move at precisely the wrong moment as the global inventory super- cycle tops out:

Leading to dramatic curve flattening:

And, before long, growth scares, falling asset prices and central bank reversal.

None of it bodes well for Australian dollar.