Forex markets were largely stable last night with Wall Street closed but under the surface there are some interesting dynamics. DXY was firm and EUR soft:

Australian dollar was basically unchanged:

Oil and gold both jumped:

Base metals lifted with oil:

US and EM junk have diverged a little but it’s not material yet:

EM stocks are stalled still:

Miners did better in London:

Other markets were closed. Westpac has the wrap:

Event Wrap

The Markit Eurozone Services PMI survey was finalised at 58.3, from the flash reading of 58.0, taking the composite index to 59.5 from 59.2. Although Germany’s final readings fell, other national indices rose at the highest growth rates in 15 years. Service sector firms are struggling with surging demand and supply shortages, including labour, and are raising prices at the “steepest pace in 20 years”, with optimism at the highest in 21 years.

UK services PMI was also finalised higher, at 62.4 from 61.7, with a record level of (input and output) price gains.

OPEC+ called off the meeting scheduled for Monday as it again struggled to resolve the differences between Saudi and UAE regarding production into end 2021 and in 2022.

Event Outlook

Australia: The Reserve Bank Board will announce its July policy decision. Following the Board meeting, the Governor will make his usual Statement at 2:30pm, and then speak at 4pm – ‘Remarks by Phillip Lowe – Today’s Monetary Policy Decision’ – which will be followed by media Q&A. The Board has already informed us that decisions will be made around the Yield Curve Targeting (YCT) Program and the Bond Purchase Program (QE). With the economy having recovered much faster than the Bank’s expectations in the November Statement on Monetary Policy, it seems reasonable that the Board will decide not to extend the ‘yield target bond’ to the November 2024 bond. We expect that the Board will decide to take a more flexible approach to its bond buying program than we have seen in the past. We think the Board will be committed to maintaining the current pace of purchases ($5 billion per week) until late in the year (around the December Board meeting). Weekly payroll jobs and wages, for the fortnight ending June 19, will serve as a guide for the June Labour Force Survey.

New Zealand: We expect to see a further improvement in confidence and own-activity expectations in the June NZIER Quarterly Survey of Business Opinion , reflecting recent strong data and the reopening of trans- Tasman travel. Measures of capacity and price pressures will be of particular interest. The March survey found that businesses had had limited success in raising their prices up to that point. Concerns about rising costs and labour shortages have escalated further in the last three months. Futures markets are predicting a 2% fall in prices at the early July GDT auction, continuing the recent trend.

Euro Area: May retail sales are expected rise 4.3%, with further strength ahead as the reopening progresses. The June ZEW survey of expectations should remain upbeat, with the recovery beginning to materialise.

US: The reopening and robust consumer spending should drive another strong print in the June ISM services index (market f/c: 63.5)

The big news of the night was oil with OPEC+ at odds over the output expansion. OPEC+ wants to expand production at 0.4mb/d but UAE wants to have its quota lifted because it has grown capacity.

Why this is being construed as bullish for oil is not obvious. If the agreement gets up we have an extra 5m/bd over the next year which is enough. If it doesn’t then the major risk is that it turns fractious and everybody pumps.

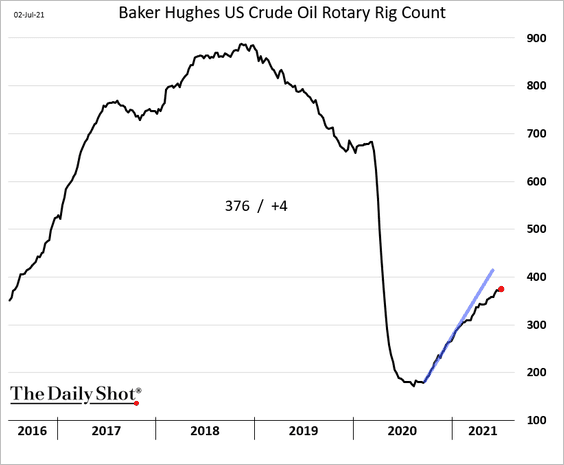

Approaching $80 is also going to be much more than tempting for US shalers. Though they have, for once, been more disciplined so far in this rebound:

That said, each downcycle brings more innovation and greater efficiency of extraction so less rigs are needed.

As for oil and the AUD, they tend to move together:

Some of this is a real relationship since the great expansion of oil-linked LNG capacity. But given that sector is so unprofitable and pays nearly no taxes, delivering no net economic benefit when the price rises, the larger impact is oil’s relationship with the more general macro environment of higher inflation and a commodities bid.

Higher oil is marginal support for the Australian dollar while it lasts.